Economic report analysis for the week ahead will focus heavily on upcoming NFP data, ISM surveys, inflation releases and central bank decisions that could shape financial market direction. Investors enter the new trading week facing elevated uncertainty surrounding economic growth, inflation trends and labour market conditions. The combination of NFP expectations, ISM Manufacturing PMI data and ISM Services PMI releases will likely become the primary drivers for US dollar movement, bond yields and broader market sentiment.

This economic report also highlights major developments across Europe, Canada, Asia and emerging markets. Market participants will monitor Eurozone inflation figures, Canadian employment data and several key central bank meetings for additional signals regarding monetary policy direction into the second half of the year.

Why This Economic Report Matters for Markets

This economic report arrives during a period where global markets remain highly sensitive to macroeconomic releases. Recent inflation data has shown signs of moderation in some regions, while labour market conditions continue to soften gradually. At the same time, geopolitical tensions and supply chain disruptions continue to create inflationary risks.

The upcoming NFP release may provide critical evidence about whether the US labour market is finally slowing in a meaningful way. Investors are also paying close attention to ISM data because manufacturing and service sector activity often provide an early indication of broader economic momentum.

Several factors make this economic report especially important:

- Expectations for Federal Reserve policy remain uncertain

- Inflation pressures remain elevated in services sectors

- Labour market conditions are beginning to weaken

- Global growth concerns continue to rise

- Energy market volatility may impact inflation trends

Markets are currently trying to determine whether central banks will maintain restrictive policy settings or begin shifting toward a more accommodative stance later in the year.

US ISM Manufacturing PMI in Focus

The ISM Manufacturing PMI release on Monday will provide an updated look at activity within the US manufacturing sector. Recent data suggests manufacturing conditions have improved modestly, although underlying details remain mixed.

S&P Global flash manufacturing PMI recently climbed to a multi-year high, supported largely by inventory accumulation and precautionary stock-building rather than strong end-user demand. This distinction is important because inventory-driven growth may not be sustainable over the longer term.

Key themes investors will monitor within the ISM report include:

New Orders

New orders remain one of the most closely watched components of ISM data. Recent gains have largely reflected businesses increasing inventories ahead of potential supply disruptions and tariff concerns.

Prices Paid

Inflation pressures within manufacturing have intensified. Rising transportation costs, shipping disruptions and higher commodity prices continue pushing input costs higher.

Employment Component

Manufacturing employment has shown modest improvement, although broader labour market conditions remain fragile.

Supplier Deliveries

Supply chain conditions have deteriorated again due to geopolitical disruptions and transportation bottlenecks.

A stronger-than-expected ISM Manufacturing PMI could support the US dollar and Treasury yields. Conversely, weaker data may reinforce expectations for slower economic growth.

Eurozone Inflation Data and ECB Outlook

The Eurozone HICP inflation release will represent another major event within this economic report. Inflation remains a central concern for the European Central Bank despite recent moderation in headline figures.

Recent inflation data from Germany, France, Italy and Spain suggests price pressures may stabilize or cool slightly in May. However, services inflation remains relatively sticky, limiting the ECB’s flexibility.

The ECB continues to signal that additional tightening remains possible if inflation risks persist. Markets currently expect another rate increase in coming months, particularly if inflation remains near current levels.

Several drivers continue influencing Eurozone inflation:

- Energy price volatility

- Wage growth pressures

- Supply chain disruptions

- Elevated service sector inflation

- Consumer demand resilience

The Eurozone economy remains fragile, however. Slower growth conditions may eventually force policymakers to reconsider the pace of tightening.

ISM Services PMI Could Shape Market Direction

The ISM Services PMI release on Wednesday may become one of the most influential reports within this economic report because the services sector represents the largest component of the US economy.

Recent business activity data points toward slowing momentum. Services activity has weakened amid softer consumer demand, elevated borrowing costs and growing uncertainty linked to geopolitical developments.

Several areas deserve close monitoring:

Business Activity

Business activity has slowed to near-stagnation levels. Consumer-facing sectors appear especially vulnerable.

Employment Trends

Service sector employment has weakened significantly. Recent data showed one of the sharpest declines in hiring since the pandemic recovery period.

Inflation Pressures

Input costs continue rising, especially within labour-intensive industries. Firms are increasingly passing higher costs to consumers.

Business Confidence

Business optimism has deteriorated due to uncertainty surrounding inflation, interest rates and geopolitical risks.

Weak ISM Services PMI data could strengthen expectations that the Federal Reserve may eventually pivot toward rate cuts. Stronger readings could delay those expectations.

Federal Reserve and Beige Book Expectations

The Federal Reserve Beige Book release will provide qualitative insight into economic conditions across different US regions. Investors will search for signs of weakening demand, labour market softening and inflation moderation.

Recent Federal Reserve commentary has remained cautious. Policymakers continue emphasizing data dependency while acknowledging progress on inflation has been uneven.

Current market expectations suggest:

- The Fed may remain on hold in the near term

- Rate cuts are unlikely until inflation cools further

- Labour market weakness could become increasingly important

- Economic growth is slowing gradually rather than collapsing

Markets will analyze Beige Book commentary regarding consumer spending, wage growth and business investment trends.

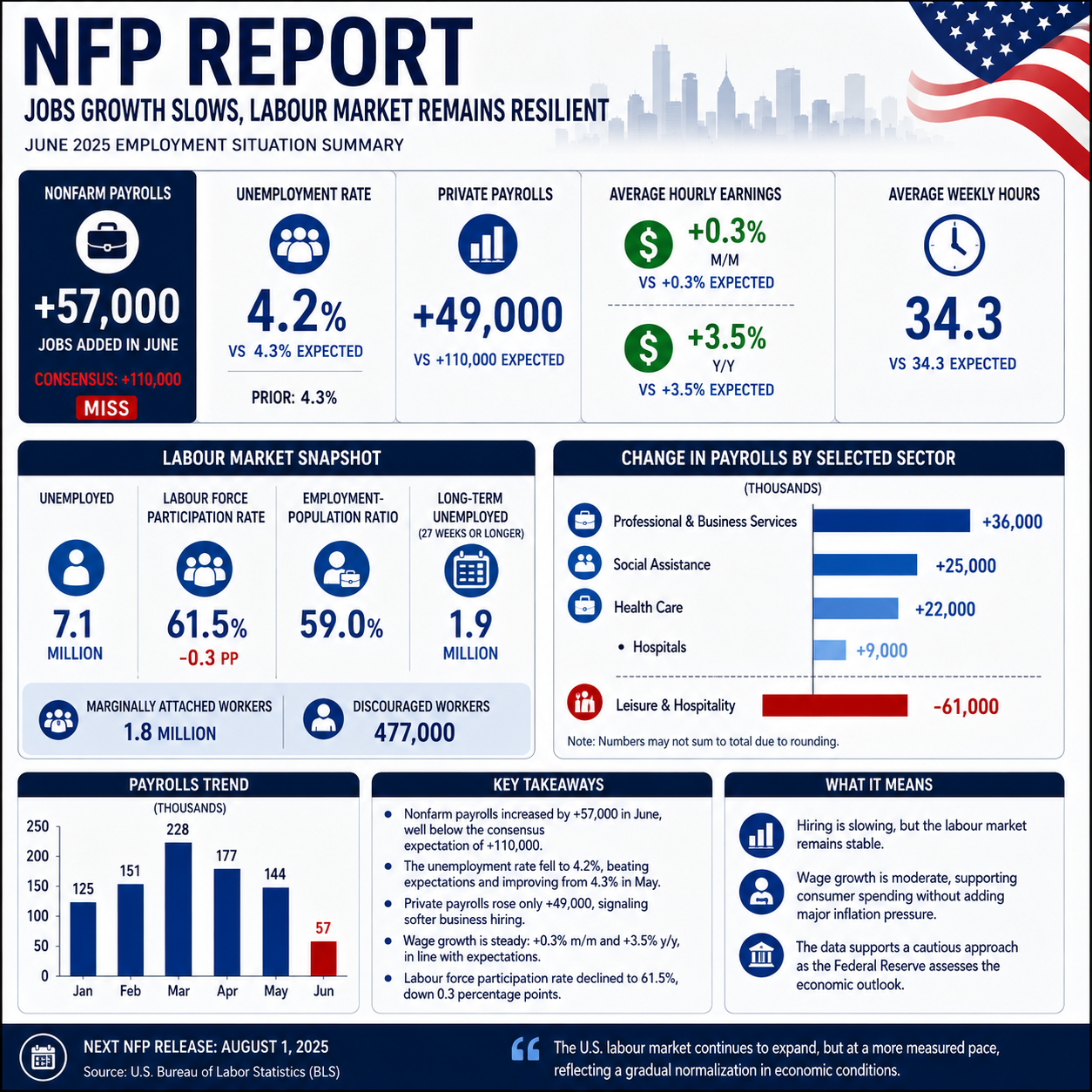

NFP Report Expected to Drive Volatility

The NFP release on Friday represents the centerpiece of this economic report. Nonfarm payrolls remain one of the most market-moving economic indicators globally.

Consensus expectations currently anticipate payroll growth around 95k, down from the prior month. The unemployment rate is expected to remain near 4.3%, while wage growth is projected at 0.3% month-over-month.

Several major institutions expect downside risk to payroll growth due to slowing hiring momentum and weaker labour demand.

Why NFP Matters

NFP data directly impacts Federal Reserve expectations because labour market conditions remain central to monetary policy decisions.

Payroll Growth Trends

Hiring momentum has slowed steadily over recent months. Businesses appear increasingly cautious amid slowing economic growth.

Wage Inflation

Average hourly earnings remain critical because elevated wage growth can contribute to persistent inflation pressures.

Unemployment Rate

Even modest payroll gains may stabilize unemployment due to slowing labour force growth.

Market Reaction Scenarios

A stronger NFP report could:

- Support Treasury yields

- Strengthen the US dollar

- Reduce rate cut expectations

- Pressure equities temporarily

A weaker NFP report could:

- Increase expectations for policy easing

- Weaken the US dollar

- Support growth-sensitive assets

- Increase recession concerns

The NFP release may ultimately determine near-term market direction.

Canadian Jobs Report and BoC Implications

Canada’s employment report will also attract attention within this economic report. Recent labour market data has weakened, with employment unexpectedly contracting in the previous release.

Several trends remain concerning:

- Full-time employment has declined

- Youth unemployment remains elevated

- Labour market turnover remains weak

- Participation rates continue fluctuating

The Bank of Canada remains cautious regarding inflation and labour market developments. Policymakers continue balancing slower growth against persistent inflation risks.

Markets currently expect limited policy flexibility from the BoC until inflation shows clearer moderation.

Global Central Bank Developments

Several additional central bank meetings and policy updates may influence market sentiment this week.

RBI Policy Decision

India’s central bank is expected to maintain rates while monitoring inflation and growth conditions.

Swedish CPIF Inflation

Sweden’s inflation data may influence expectations regarding future Riksbank policy adjustments.

Swiss CPI

Swiss inflation remains relatively contained, allowing the Swiss National Bank to maintain a cautious approach.

ECB Outlook

ECB minutes reinforced expectations that policymakers remain concerned about inflation persistence.

SARB Policy

South Africa’s central bank recently raised rates while emphasizing inflation risks and cautious policymaking.

Geopolitical Risks Remain Important

Geopolitical developments continue influencing this economic report and broader market conditions.

Recent tensions involving the United States and Iran initially triggered concerns regarding energy markets and shipping disruptions. However, reports suggesting potential diplomatic progress helped improve market sentiment later in the week.

Markets remain highly sensitive to:

- Energy supply disruptions

- Shipping route risks

- Commodity price volatility

- Global trade tensions

- Regional military developments

Any escalation could quickly impact inflation expectations and financial market stability.

Australia, Japan and Asia-Pacific Outlook

Australia’s recent inflation data highlighted ongoing divergence between headline and core inflation trends. While headline inflation moderated, underlying price pressures remain elevated.

Japan’s economic data also delivered mixed signals:

- Labour markets remain resilient

- Inflation has softened recently

- Consumer spending remains uneven

- Bank of Japan tightening expectations persist

Asian central banks continue navigating the difficult balance between inflation control and economic growth support.

Market Themes to Watch This Week

This economic report identifies several major themes likely to dominate market sentiment:

Inflation Persistence

Services inflation remains elevated across many economies.

Labour Market Weakness

Employment conditions continue softening gradually.

Central Bank Caution

Policymakers remain hesitant to signal aggressive easing.

Geopolitical Uncertainty

Global conflicts continue creating volatility risks.

Growth Concerns

Economic momentum continues slowing in several regions.

Potential Market Impact Across Asset Classes

US Dollar

Strong NFP and ISM data could support further dollar strength.

Treasury Yields

Bond yields may react sharply to labour market and inflation data.

Equities

Equity markets may remain volatile as investors reassess monetary policy expectations.

Commodities

Energy and commodity prices remain highly sensitive to geopolitical developments.

Emerging Markets

Emerging market currencies may face volatility amid shifting Fed expectations.

Conclusion

This economic report highlights a highly important week for global financial markets. NFP, ISM Manufacturing PMI and ISM Services PMI releases will likely dominate investor attention as markets search for clearer evidence regarding the direction of economic growth, inflation and labour market conditions.

Central banks remain cautious as inflation pressures persist despite signs of slowing economic momentum. Investors will continue balancing expectations for future rate cuts against concerns surrounding sticky inflation and geopolitical uncertainty.

The NFP release may ultimately become the defining event of the week, particularly if labour market data deviates meaningfully from expectations. Combined with ISM data and global inflation releases, these reports could significantly shape market pricing and policy expectations heading into the next quarter.

FAQs

What is an economic report?

An economic report provides analysis and data regarding economic conditions, inflation, employment and financial markets.

Why is NFP important?

NFP measures US job creation and significantly influences Federal Reserve policy expectations and market sentiment.

What does ISM mean?

ISM stands for Institute for Supply Management, which publishes manufacturing and services PMI data.

How does NFP impact markets?

Strong NFP data can strengthen the US dollar and Treasury yields, while weak data may increase expectations for rate cuts.

Why are ISM reports important?

ISM reports provide early insight into economic activity, business conditions and inflation pressures.

What is HICP inflation?

HICP stands for Harmonized Index of Consumer Prices, which measures inflation across the Eurozone.

What are markets watching most this week?

Markets are primarily focused on NFP, ISM Manufacturing PMI and ISM Services PMI releases.

Why do central bank decisions matter?

Central bank policy influences borrowing costs, inflation expectations and overall financial market conditions.