Economic Report Overview

Economic Report analysis for the week of 6–10 July focuses on several high-impact events that are expected to influence global financial markets, interest rate expectations and investor sentiment. The calendar is dominated by the release of the FOMC Minutes, the US ISM Services PMI, central bank policy announcements, inflation data from several major economies, and labour market updates from Canada.

While equity markets continue to trade near recent highs, investors remain cautious as policymakers balance persistent inflation pressures against signs of slowing economic momentum. Monetary policy remains the dominant theme across developed markets, with central banks continuing to stress their commitment to price stability despite evidence that growth is moderating in several regions.

This week’s Economic Report highlights the growing divergence between economies. The United States continues to show resilience despite softer employment growth, Europe remains focused on inflation and monetary tightening, China continues to battle uneven domestic demand, while commodity markets await another important decision from OPEC+.

For traders, investors and economists alike, this collection of data releases could significantly influence expectations for interest rates during the second half of the year.

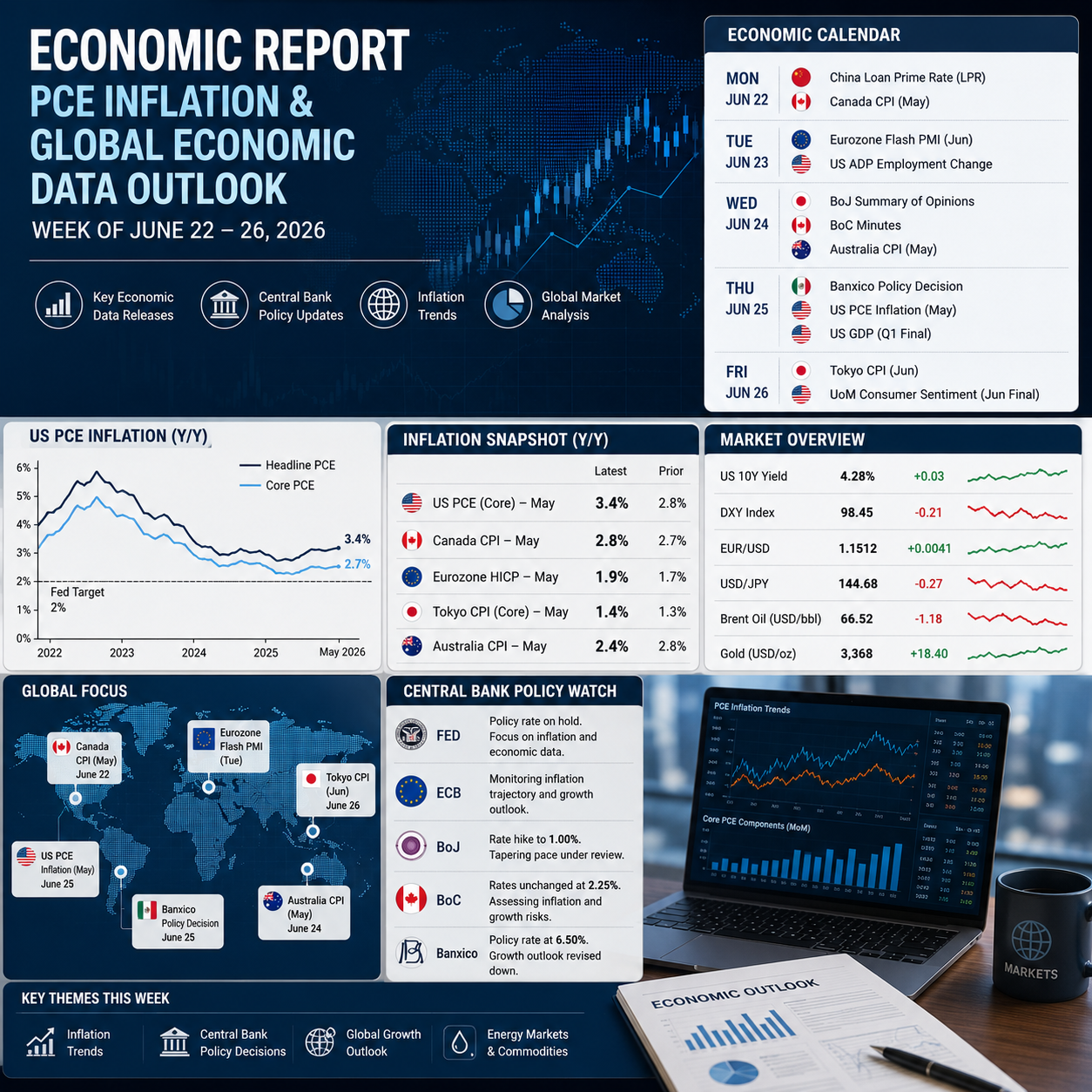

Weekly Economic Calendar

| Day | Major Events |

|---|---|

| Monday | US ISM Services PMI, Eurozone Retail Sales, BoC Business Outlook Survey |

| Tuesday | German Industrial Production, US Trade Balance, Canadian Trade Balance |

| Wednesday | FOMC Minutes, RBNZ Interest Rate Decision, Swedish Inflation |

| Thursday | ECB Minutes, Chinese Inflation, US Jobless Claims |

| Friday | Canadian Employment Report, Japanese PPI, IEA Oil Market Report |

Several of these releases have the potential to reshape expectations surrounding monetary policy and global growth.

Why This Economic Report Matters

Markets enter the new week following several important developments.

The latest US employment figures showed that hiring slowed noticeably during June. Although payroll growth remained positive, the pace of expansion was considerably weaker than expected, suggesting that higher borrowing costs are gradually cooling labour demand.

Meanwhile, inflation continues to remain above target across most advanced economies. While energy prices have eased following geopolitical developments in the Middle East, services inflation remains stubbornly elevated in several countries.

Consequently, policymakers continue to face a difficult balancing act.

Raise rates too aggressively and economic growth risks slowing further.

Pause too early and inflation could become entrenched.

This tension is likely to dominate market pricing throughout the week.

OPEC+ Meeting Could Influence Inflation Expectations

The week’s first major event actually arrives before markets fully reopen.

OPEC+ ministers are expected to approve another increase in crude oil production during Sunday’s meeting.

Current expectations point towards an additional production increase of approximately 188,000 barrels per day, matching increases approved during previous meetings.

Several factors explain why additional supply appears increasingly likely.

Oil prices have retreated sharply following the easing of geopolitical tensions in the Middle East after the United States and Iran agreed to a memorandum aimed at reducing regional conflict.

At the same time, shipping through the Strait of Hormuz has gradually normalised, reducing concerns surrounding energy supply disruptions.

Additional pressure has come from weaker Chinese import demand and increasing production from countries outside the traditional OPEC alliance.

For policymakers, lower energy prices could provide welcome relief by reducing inflationary pressures during the second half of the year.

However, politics inside OPEC+ remain complicated.

Reports suggest Iraq continues pushing for higher production quotas while questioning existing output restrictions. Such disagreements could eventually create divisions inside the organisation, although analysts currently expect members to continue supporting a gradual rollback of production cuts introduced during 2023.

Should additional supply reach markets as expected, crude prices may remain contained, reducing one important source of inflation pressure for central banks.

US ISM Services PMI: A Critical Gauge of Economic Momentum

Among Monday’s releases, the US ISM Services PMI will receive considerable market attention.

As the largest component of the US economy, the services sector provides one of the clearest real-time indicators of underlying economic activity.

Recent survey data suggests conditions remain expansionary, although growth continues at a relatively modest pace.

The latest S&P Global flash survey showed business activity rising to its strongest level in four months.

At first glance, this appears encouraging.

However, looking beneath the headline reveals a more mixed picture.

Business activity improved modestly, but many companies continued reporting cautious customer spending.

Higher borrowing costs remain a significant challenge.

Businesses also continue highlighting elevated operating expenses, particularly labour costs and service-related inflation.

New orders improved only modestly, while export demand remained relatively weak.

This combination reflects an economy that continues growing but lacks broad-based acceleration.

Perhaps more concerning for policymakers is the continued strength of inflation within the services sector.

Input costs increased at their fastest pace in six months.

Selling prices accelerated further, reaching their highest rate in almost a year.

This reinforces the Federal Reserve’s concern that underlying inflation remains persistent despite lower energy prices.

Another notable feature of recent surveys has been employment.

Service-sector businesses reported modest reductions in staffing levels as firms attempted to offset rising costs through greater efficiency.

Although layoffs remain limited, hiring intentions have become increasingly cautious.

The ISM survey will therefore provide valuable confirmation regarding whether these trends are continuing.

What Investors Should Watch

Markets will focus on four specific components.

- Business Activity

- New Orders

- Employment

- Prices Paid

If prices remain elevated while activity improves, investors may conclude that inflation remains sufficiently persistent to justify additional Federal Reserve tightening.

Conversely, weaker activity combined with softer price pressures would reinforce expectations that policy rates may be approaching their peak.

Given the Federal Reserve’s continued emphasis on inflation, the pricing component may ultimately prove more influential than the headline index itself.

FOMC Minutes: Markets Search for Policy Clues

The FOMC Minutes represent the week’s most closely watched event.

While the Federal Reserve left interest rates unchanged during its previous meeting, policymakers delivered what many analysts interpreted as a significantly more hawkish message.

Perhaps the most important development was the complete removal of forward guidance.

Rather than signalling likely future policy moves, officials instead emphasised that every meeting would remain data dependent.

This reflects a broader shift towards flexibility.

Federal Reserve Chair Kevin Warsh has repeatedly argued that excessive forward guidance limits policymakers’ ability to respond quickly to changing economic conditions.

Instead, policymakers appear determined to retain maximum flexibility while maintaining credibility in their commitment to restoring price stability.

Inflation forecasts were revised higher across much of the forecast horizon.

Economic growth projections were trimmed modestly.

Unemployment expectations improved slightly.

Taken together, these revisions suggest policymakers remain relatively confident about economic resilience despite acknowledging slower growth.

The updated dot plot also surprised markets.

Several members now expect interest rates to remain higher for longer than previously anticipated.

Some policymakers even projected additional rate increases during coming years rather than eventual reductions.

This represented one of the clearest hawkish shifts observed in recent Federal Reserve communications.

What the Minutes May Reveal

While the policy decision itself is already known, the meeting minutes provide valuable insight into internal discussions.

Investors will analyse the document for evidence regarding:

- How concerned officials remain about services inflation.

- Whether labour market weakness received significant attention.

- The degree of disagreement among committee members.

- Discussion surrounding balance sheet reduction.

- Confidence in inflation returning towards target.

Any indication that policymakers are becoming more comfortable with inflation progress could reduce expectations for future tightening.

However, if officials expressed widespread concern that inflation risks remain elevated, markets may interpret the minutes as reinforcing the case for maintaining restrictive policy for longer.

RBNZ Policy Decision: Will the Reserve Bank of New Zealand Tighten Again?

Another key event in this week’s Economic Report is the Reserve Bank of New Zealand’s (RBNZ) monetary policy announcement. Although the RBNZ oversees a comparatively small economy, its policy decisions are closely monitored because they often provide an early indication of how developed-market central banks are balancing inflation against slowing growth.

Market pricing currently favours a 25-basis-point increase, with investors assigning a high probability that the Official Cash Rate will rise from 2.25% to 2.50%. Such a move would reinforce the central bank’s determination to keep inflation under control despite evidence that domestic demand has moderated over recent quarters.

The debate, however, remains finely balanced.

Unlike several other central banks that have continued tightening, New Zealand has maintained a more cautious approach over recent meetings despite inflation remaining above its preferred target range. Consumer prices have proven more persistent than anticipated, yet policymakers have preferred to gather additional evidence before committing to further tightening.

The previous policy meeting illustrated this uncertainty perfectly. Committee members were evenly divided on whether interest rates should remain unchanged, with the Governor casting the deciding vote to maintain current policy while simultaneously delivering a hawkish message about future meetings.

That communication shifted market expectations considerably.

Investors interpreted the Governor’s comments as signalling that additional tightening remained the most likely outcome if inflation failed to moderate convincingly.

Since then, several developments have complicated the outlook.

Energy prices have declined noticeably following reduced geopolitical tensions, easing one important inflationary risk. At the same time, domestic inflation has remained stubbornly elevated, leaving policymakers with conflicting signals.

Consequently, the accompanying statement may ultimately prove more important than the rate decision itself.

Should policymakers emphasise that inflation risks continue to outweigh slowing growth, markets may continue pricing additional tightening later this year. Conversely, a more balanced assessment could encourage expectations that the policy cycle is approaching its peak.

For currency markets, guidance surrounding future meetings will likely generate greater volatility than the actual policy decision.

ECB Minutes: Searching for Clarity on the European Central Bank’s Next Move

Attention then shifts to Europe, where the publication of the ECB Minutes should provide greater insight into the Governing Council’s thinking following its latest interest rate increase.

The European Central Bank delivered another widely anticipated rate hike during its June meeting while maintaining a cautious but clearly inflation-focused tone.

President Christine Lagarde acknowledged encouraging progress in certain inflation measures but stopped well short of suggesting that policy tightening had concluded.

That balanced approach reflected the difficult environment currently facing European policymakers.

Headline inflation has eased from previous peaks, largely due to lower energy prices, yet underlying services inflation remains considerably stronger than officials would prefer.

Meanwhile, economic growth across the euro area continues to weaken.

Manufacturing activity remains subdued in several member states, business confidence has softened, and consumer spending remains restrained by elevated borrowing costs.

The ECB Minutes will therefore be analysed for evidence regarding how policymakers weighed these competing risks.

Investors will pay particular attention to several themes.

Inflation Persistence

Committee members are expected to have discussed whether recent improvements in headline inflation represent a lasting trend or merely temporary relief resulting from lower energy costs.

If officials expressed concern that services inflation remains excessively strong, markets may interpret the minutes as supporting further tightening later this year.

September versus Immediate Action

Another important issue concerns policy timing.

Although another immediate increase appears unlikely following recent energy price declines, investors remain divided over whether September could bring additional tightening.

The minutes may reveal whether policymakers already viewed September as the preferred opportunity for further action.

Growth Risks

Europe’s economic outlook has deteriorated modestly since the previous meeting.

If committee members expressed increasing concern about slowing economic activity, markets may conclude that the tightening cycle is nearing completion.

Overall, investors should remember that meeting minutes describe discussions held several weeks earlier.

Since then, geopolitical developments, lower oil prices and new economic data have altered the outlook.

Consequently, while the ECB Minutes remain valuable, markets will likely treat them as historical context rather than definitive guidance.

Chinese Inflation: Assessing the World’s Second-Largest Economy

China’s latest inflation figures will provide another important piece of the global economic puzzle.

Unlike many developed economies that continue battling persistent inflation, China has experienced comparatively subdued consumer price pressures throughout much of the past year.

Recent data highlighted this contrast.

Consumer inflation remained relatively contained while producer prices continued strengthening, reflecting improving industrial demand and higher commodity prices.

Several structural forces explain this divergence.

Domestic consumer spending continues recovering gradually rather than rapidly.

Property market weakness has constrained household confidence.

Meanwhile, industrial investment linked to advanced manufacturing, renewable energy and artificial intelligence has supported demand for raw materials and intermediate goods.

Government initiatives encouraging technological development have also increased demand across computing-related industries.

As a result, producer prices have risen more quickly than consumer prices.

This distinction matters because producer inflation often feeds into consumer prices over time.

If Thursday’s data shows another acceleration in factory gate prices, analysts may begin reassessing inflation expectations across global supply chains.

Conversely, subdued consumer inflation would reinforce the view that Chinese domestic demand remains relatively fragile.

Such an outcome could influence commodity markets, particularly industrial metals and energy prices.

Investors should therefore monitor both components carefully rather than focusing solely on the headline CPI figure.

Swedish Inflation: A Test for the Riksbank

Sweden’s June inflation report represents another important event within this week’s Economic Report, particularly after recent volatility in European inflation trends.

Economists generally expect inflation to moderate further following lower global energy prices.

Forecasts suggest that headline inflation will ease modestly while core inflation remains subdued.

Although this would represent encouraging progress, policymakers are unlikely to declare victory prematurely.

The Riksbank has repeatedly stressed that inflation expectations must remain firmly anchored before policy can become less restrictive.

Another consideration involves the Swedish krona.

Currency weakness has periodically increased imported inflation, offsetting some of the benefits generated by lower energy costs.

Accordingly, policymakers will continue monitoring exchange rate developments alongside domestic inflation.

Should inflation surprise on the upside once again, expectations for future tightening could quickly re-emerge.

Norwegian Inflation: Another Decision Point for Norges Bank

Norway’s inflation figures also deserve attention.

Unlike several European economies experiencing slowing inflation, Norway continues facing relatively resilient domestic price pressures.

Recent data has consistently exceeded expectations.

Although lower oil prices have eased certain inflation risks, currency movements continue creating upward pressure on imported goods.

Consequently, Norges Bank remains one of the few developed-market central banks where another interest rate increase remains a realistic possibility during coming months.

Markets currently remain divided regarding timing.

Some economists anticipate another increase during August.

Others believe policymakers will prefer waiting until September.

Friday’s inflation report may ultimately determine which scenario becomes more likely.

Canadian Employment Report: Labour Market Under the Microscope

Friday concludes this week’s Economic Report with one of North America’s most important releases—the Canadian employment report.

Employment growth has become increasingly volatile throughout recent months.

After several consecutive declines earlier in the year, hiring rebounded strongly during the previous report.

This recovery reduced immediate concerns regarding recession risks but did not fundamentally alter the broader economic picture.

The Bank of Canada continues describing the economy as operating below full capacity while emphasising persistent inflation pressures.

This creates a familiar challenge.

Weak labour markets generally argue for easier monetary policy.

Elevated inflation argues for continued restraint.

Markets currently expect another interest rate increase before year-end.

Friday’s employment figures could significantly influence those expectations.

Several indicators deserve close attention.

- Total employment growth

- Full-time employment

- Unemployment rate

- Labour force participation

- Wage growth

Of these, wage growth may prove especially influential.

Persistent wage inflation could reinforce concerns that underlying inflationary pressures remain inconsistent with the Bank of Canada’s long-term objective.

Conversely, weaker employment combined with moderating wage growth could encourage investors to reassess expectations for additional tightening.

The Canadian dollar may therefore experience elevated volatility following the release.

How These Events Could Shape Financial Markets

This week’s calendar presents investors with an unusually concentrated series of high-impact releases capable of influencing multiple asset classes simultaneously.

For equity markets, stronger-than-expected economic data could initially support corporate earnings expectations. However, if stronger data also increases expectations for further interest rate hikes, stock markets may struggle as higher discount rates weigh on valuations.

For bond markets, inflation data and the FOMC Minutes remain the primary catalysts. Persistent inflation could push government bond yields higher, while softer economic indicators may encourage renewed demand for fixed-income assets.

In foreign exchange markets, central bank communication will remain the dominant driver. Currency pairs involving the US dollar, euro, New Zealand dollar and Canadian dollar are likely to experience heightened volatility as investors reassess interest rate expectations.

Meanwhile, commodity markets will focus on the OPEC+ decision alongside Chinese inflation data. Together, these releases could influence expectations for future demand and global energy prices.

Week in Review: The Economic Developments Shaping Market Expectations

While this week’s Economic Report is centred on several forward-looking events, investors continue to digest a series of important economic releases from the previous week that have already begun influencing expectations for central bank policy.

The dominant themes remain familiar. Inflation continues to moderate gradually in some regions while remaining stubbornly elevated in others. Labour markets are beginning to cool, although not uniformly, and central banks continue to prioritise price stability despite growing evidence that higher borrowing costs are weighing on economic activity.

Taken together, last week’s data reinforced the view that policymakers are unlikely to pivot towards easier monetary policy in the immediate future. Instead, financial markets continue to anticipate that interest rates will remain elevated for longer as central banks seek greater confidence that inflation is moving sustainably towards target.

RBA Minutes Reinforce Australia’s Inflation Fight

The release of the Reserve Bank of Australia’s meeting minutes reaffirmed the Board’s commitment to maintaining restrictive monetary policy until inflation is clearly under control.

Although policymakers ultimately left interest rates unchanged, the discussion revealed little appetite for declaring victory over inflation.

Board members acknowledged that previous rate increases were continuing to work through the economy, but also noted that demand remained stronger than supply across several sectors.

Importantly, the minutes highlighted that inflation is still expected to take considerable time to return to target, reinforcing the view that further tightening remains possible if economic conditions require it.

Officials also discussed geopolitical developments and their potential influence on commodity prices, supply chains and inflation expectations.

Most economists continue expecting the RBA to remain on hold in the near term, although the possibility of another increase later this year cannot be completely dismissed should inflation remain persistent.

Japan’s Tankan Survey Highlights Improving Business Confidence

Japan provided one of the week’s more encouraging economic surprises.

The latest Tankan Business Survey exceeded expectations across most major indicators, demonstrating continued resilience among both manufacturers and service-sector firms.

Large manufacturers reported the strongest confidence levels in several years, while business investment intentions remained robust.

Perhaps most encouraging was the continued improvement in corporate capital expenditure plans.

Strong investment typically reflects confidence in future demand and supports broader economic growth through increased productivity and employment.

The survey also suggested that Japanese businesses have become more resilient to external geopolitical shocks than many analysts initially feared.

Although some uncertainty remains surrounding global trade conditions, the results support the Bank of Japan’s gradual approach towards monetary policy normalisation.

Unlike many developed economies, Japan continues to transition carefully away from decades of exceptionally accommodative policy.

Strong business confidence provides policymakers with greater flexibility should inflation remain above recent historical norms.

Eurozone Inflation Continues to Moderate

Another important development came from the latest Eurozone inflation figures.

Headline inflation slowed more than economists had anticipated, reflecting continued easing in energy costs and improving supply chain conditions.

Core inflation also moderated, providing further evidence that underlying price pressures may finally be beginning to soften.

For the European Central Bank, this represents encouraging progress.

However, policymakers remain cautious.

Inflation continues to exceed the ECB’s medium-term objective, while wage growth across several member states remains elevated.

Services inflation, in particular, continues to prove more resilient than goods inflation.

Consequently, although recent inflation reports reduce pressure for immediate additional tightening, they do not eliminate the possibility of further policy action later this year.

Investors therefore continue viewing September as the next realistic opportunity for any additional adjustment in monetary policy should inflation fail to improve sufficiently.

US ISM Manufacturing PMI Reflects Slower but Continued Expansion

The manufacturing sector delivered another mixed message.

Although the headline ISM Manufacturing PMI declined modestly from the previous month, it remained comfortably above the expansion threshold.

This indicates that manufacturing activity continues growing, albeit at a slower pace than earlier in the year.

Several underlying components deserve attention.

New orders softened modestly, suggesting that demand growth is beginning to moderate.

Production also eased slightly, reflecting both slower order growth and improved supply chain conditions.

Importantly, supplier delivery times shortened, indicating that previous logistical bottlenecks continue to ease.

Perhaps the most encouraging development came from inflation indicators.

The Prices Paid Index declined significantly from previous highs, suggesting manufacturers are experiencing less cost pressure than earlier in the year.

Employment also improved modestly, although hiring remains relatively subdued.

Overall, the manufacturing sector continues demonstrating resilience despite higher borrowing costs and ongoing global uncertainty.

Swiss Inflation Remains Exceptionally Well Contained

Switzerland continues to stand apart from many developed economies.

The latest inflation report showed consumer prices remaining remarkably stable despite ongoing global inflationary pressures.

Monthly inflation was effectively unchanged, while annual inflation remained comfortably within the Swiss National Bank’s target range.

Lower energy prices contributed significantly to this outcome.

Transportation and household energy costs both declined, offsetting modest price increases elsewhere in the economy.

For the Swiss National Bank, these figures reinforce the appropriateness of maintaining current policy settings.

Unlike several other central banks, Switzerland currently faces little urgency to tighten monetary policy further.

Instead, policymakers can continue monitoring international developments while maintaining price stability.

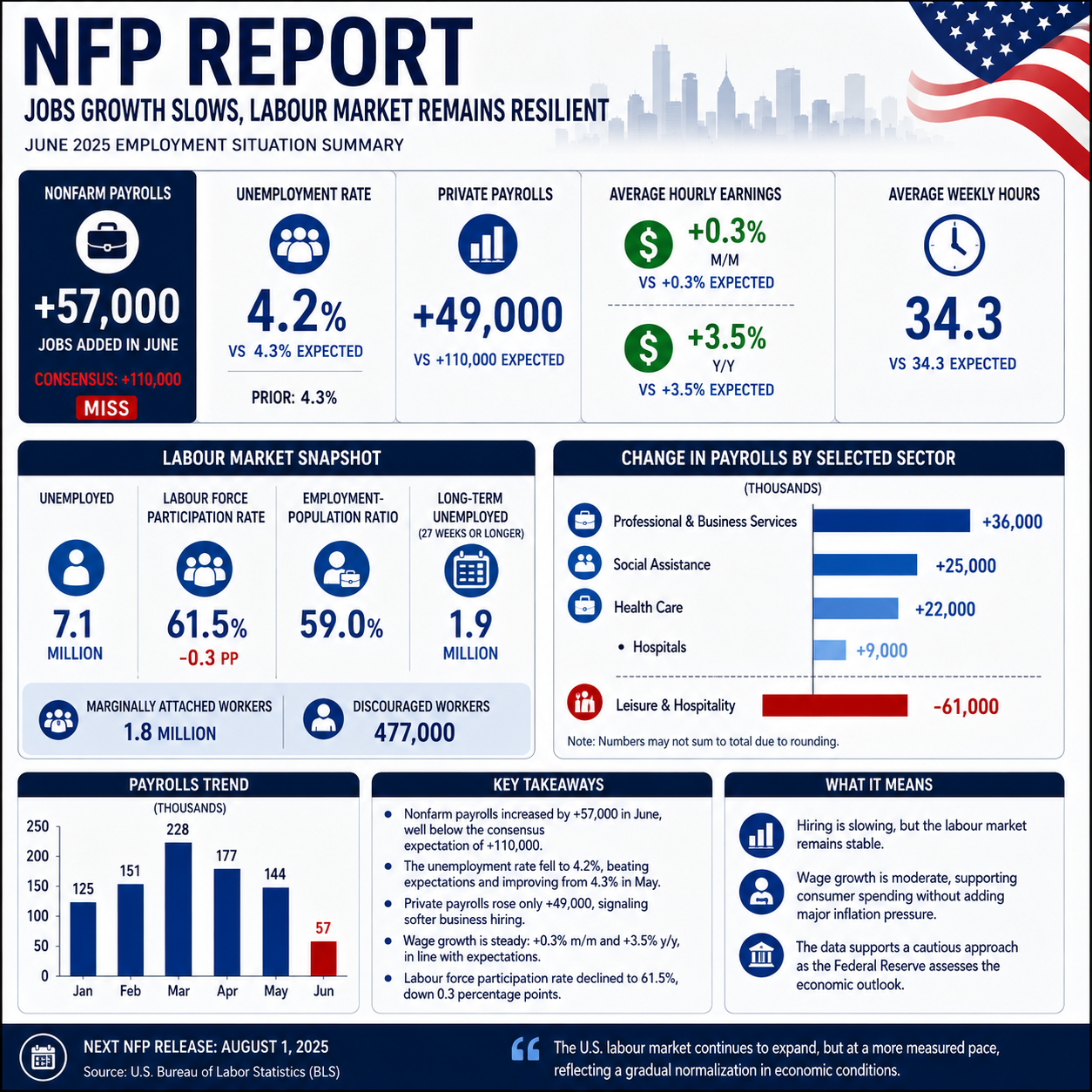

US Employment Report Signals a Gradual Cooling in the Labour Market

Perhaps the most closely scrutinised release from last week was the US Non-Farm Payrolls report.

Employment growth slowed considerably compared with previous months, falling well below consensus expectations.

While payrolls continued expanding, the pace of hiring suggested that higher interest rates are gradually reducing labour demand.

However, the report was far from uniformly weak.

The unemployment rate actually declined slightly.

Wage growth remained broadly consistent with expectations.

Professional services, healthcare and social assistance continued creating jobs.

The primary weakness was concentrated within leisure and hospitality, where employment reversed unusually strong gains recorded during the previous month.

Many economists believe this reflected temporary seasonal distortions rather than a fundamental deterioration in labour market conditions.

Nevertheless, the report reinforces the view that employment growth is gradually slowing.

That moderation is precisely what the Federal Reserve has been attempting to achieve through tighter monetary policy.

Importantly, one softer employment report is unlikely to alter policy significantly.

However, should similar reports emerge over coming months, policymakers may eventually begin placing greater emphasis on slowing labour market conditions alongside inflation.

Federal Reserve Outlook: Inflation Still Drives Policy

The Federal Reserve remains at the centre of global financial markets.

Despite softer employment data, policymakers continue emphasising inflation as their primary concern.

Recent communications have consistently reinforced three important messages.

First, inflation remains above target.

Second, the economy continues demonstrating resilience.

Third, future policy decisions will remain entirely dependent on incoming economic data.

This flexible approach allows officials to respond quickly as conditions evolve while avoiding commitments that may later prove inappropriate.

Markets currently expect interest rates to remain elevated for an extended period.

Although expectations for additional immediate tightening have moderated slightly following weaker employment data, investors continue anticipating restrictive policy throughout much of the year.

Accordingly, every major inflation release, employment report and business survey assumes greater importance.

This week’s FOMC Minutes and US ISM Services PMI therefore represent critical pieces of that broader policy puzzle.

Investment Implications

This week’s Economic Report presents investors with several potential scenarios.

Equities

Equity investors will seek confirmation that economic growth remains sufficiently strong to support corporate earnings without triggering significantly higher interest rates.

Technology, financials and consumer discretionary sectors may experience above-average volatility following the week’s major data releases.

Fixed Income

Bond markets remain particularly sensitive to inflation surprises.

Should inflation indicators continue moderating, government bond yields may stabilise or decline modestly.

Conversely, stronger inflation data could renew upward pressure on yields.

Foreign Exchange

Currency markets are likely to respond primarily to changes in interest rate expectations.

The US dollar, euro, Canadian dollar and New Zealand dollar may all experience increased volatility following central bank communications.

Commodities

Oil markets remain focused on OPEC+ production decisions.

Industrial metals will likely respond to Chinese inflation and broader growth expectations.

Gold may continue reacting primarily to movements in real interest rates and Federal Reserve expectations.

Key Risks Investors Should Monitor

Although the scheduled economic calendar is substantial, investors should remain alert to additional developments that could quickly reshape market sentiment.

Among the most significant risks are:

- Unexpected inflation surprises in major economies.

- More pronounced deterioration in labour market conditions.

- Renewed geopolitical tensions affecting global energy markets.

- Significant revisions to previously released economic data.

- Changes in central bank communication between scheduled meetings.

- Unexpected weakness in global consumer demand.

- Further slowing in Chinese economic activity.

- Currency volatility driven by diverging monetary policy expectations.

Monitoring these risks alongside scheduled data releases provides a more comprehensive framework for assessing market conditions.

Conclusion

This week’s Economic Report arrives at a pivotal moment for global financial markets.

Although inflation has eased from the extreme levels experienced over recent years, it remains above target across many major economies. Central banks therefore continue navigating the difficult balance between restoring price stability and preserving economic growth.

The FOMC Minutes will offer valuable insight into the Federal Reserve’s internal policy discussions, while the US ISM Services PMI will provide an important update on the health of the largest segment of the US economy. Together with policy decisions from the Reserve Bank of New Zealand, the release of the ECB Minutes, Chinese inflation figures and Canada’s employment report, these events will shape expectations for interest rates and broader market direction during the weeks ahead.

Investors should focus not only on headline numbers but also on the underlying trends driving policy decisions. Inflation persistence, labour market resilience, business activity and consumer demand remain the key variables influencing central bank thinking.

While individual data releases may generate short-term market volatility, the broader narrative remains unchanged. Policymakers continue signalling that inflation control remains their highest priority, suggesting that monetary policy is likely to stay restrictive until there is clear and sustained evidence that price pressures are returning to target.

For investors, traders and market participants, maintaining a disciplined, data-driven approach remains essential. This week’s economic releases will provide important clues about the trajectory of the global economy and the outlook for monetary policy through the remainder of the year.

Frequently Asked Questions

What is the most important event in this week’s Economic Report?

The release of the FOMC Minutes is expected to be the week’s most influential event, providing insight into the Federal Reserve’s latest policy discussions and future interest rate outlook.

Why is the US ISM Services PMI important?

The US ISM Services PMI measures business activity in the US services sector, which represents the largest part of the American economy. It is widely used as an indicator of economic growth and inflationary pressures.

How could the OPEC+ meeting affect financial markets?

Changes in oil production can influence crude oil prices, inflation expectations and energy-related sectors, making OPEC+ decisions important for global investors.

What should investors watch in the ECB Minutes?

Markets will look for clues about policymakers’ views on inflation, economic growth and the timing of any future interest rate adjustments.

Why does the Canadian employment report matter?

Canada’s labour market data provides insight into economic strength and may influence future Bank of Canada policy decisions, affecting both bond and currency markets.

What is the main theme of this week’s Economic Report?

The dominant theme is how central banks continue balancing persistent inflation with gradually slowing economic growth while determining the appropriate path for future monetary policy.