NFP Points to a Labour Market That Continues to Cool in an Orderly Manner

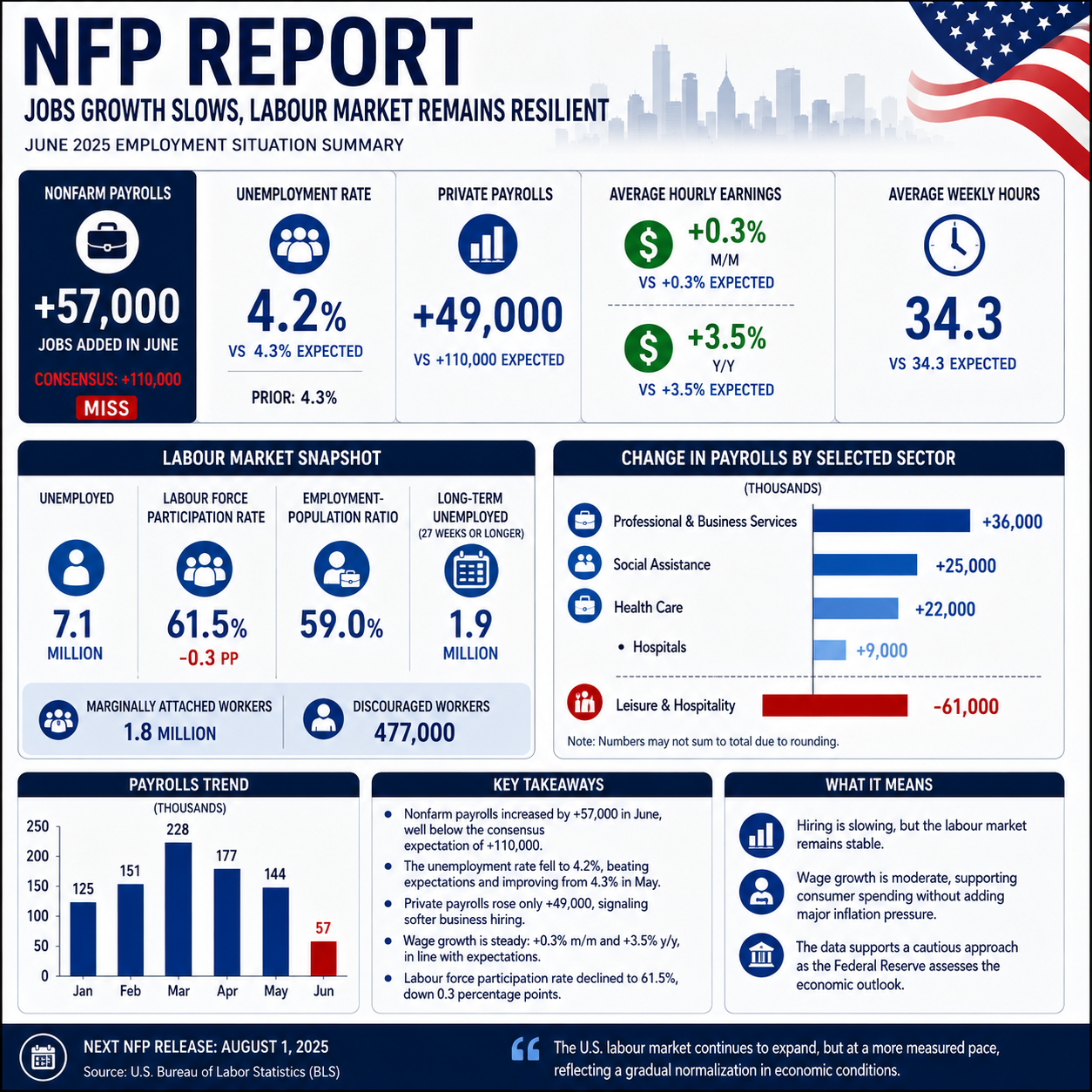

NFP increased by 57,000 jobs, according to the latest Bureau of Labor Statistics Employment Situation report, marking another month of positive employment growth while reinforcing evidence that the U.S. labour market continues to transition toward a more sustainable pace. Although hiring remained positive, payroll growth was noticeably slower than the average monthly gains recorded over the previous year, reflecting a labour market that is gradually cooling rather than weakening.

At the same time, the unemployment rate held at 4.2%, while the number of unemployed Americans changed little at 7.1 million. The combination of slower payroll growth and stable unemployment suggests businesses remain cautious in expanding headcount but are not broadly reducing staff.

For policymakers, investors and economists, the latest Employment Report adds to a growing body of evidence that labour demand continues to normalize after several years of exceptionally strong hiring. Higher borrowing costs, moderating economic activity and improving labour supply appear to be reducing pressure on employers without triggering a significant deterioration in employment conditions.

The report also highlights a widening divergence across industries. Hiring continued in professional and business services, healthcare and social assistance, while leisure and hospitality recorded a notable decline. Rather than pointing to broad-based weakness, sector performance indicates businesses are responding differently to changing demand conditions depending on industry-specific fundamentals.

Payroll Growth Moderates but Remains Positive

The headline increase of 57,000 Nonfarm Payrolls represents continued expansion in employment, although the pace of hiring has slowed considerably from the stronger gains that characterised much of the economic recovery.

Monthly payroll growth rarely follows a straight line. Instead, hiring typically fluctuates as businesses respond to changes in demand, productivity, financing conditions and seasonal factors. June’s payroll increase therefore reflects a labour market that continues creating new positions but at a pace more consistent with an economy operating closer to full employment.

Importantly, there is little evidence within the report of widespread job losses across the private sector. Instead, employers appear increasingly selective about recruitment, adding workers where demand remains strong while exercising greater discipline in industries facing slower growth.

This pattern is consistent with a labour market that is becoming more balanced following several years of extraordinary hiring activity.

Unemployment Holds at 4.2%

One of the most significant aspects of the report is that the unemployment rate remained unchanged at 4.2%.

Despite slower payroll growth, unemployment did not move materially higher, suggesting businesses continue retaining workers even as hiring moderates.

The total number of unemployed people also remained broadly stable at 7.1 million, reinforcing the view that labour market conditions have softened only gradually rather than deteriorating sharply.

Across major demographic groups, unemployment rates showed little change during the month:

| Group | Unemployment Rate |

|---|---|

| Adult men | 3.9% |

| Adult women | 3.7% |

| Teenagers | 14.6% |

| White workers | 3.6% |

While differences remain between demographic groups, the broader picture continues to reflect relatively stable employment conditions throughout the labour market.

Labour Force Participation Declines

Although unemployment remained steady, one area warranting closer attention was labour force participation.

The labour force participation rate declined to 61.5%, representing a 0.3 percentage point decrease during the month.

Similarly, the employment-population ratio fell to 59.0%, indicating a smaller proportion of the working-age population remained employed.

Participation rates often provide valuable context beyond the headline unemployment rate. A decline can reflect retirements, demographic changes, workers leaving the labour force temporarily or individuals choosing not to actively seek employment.

While one month’s decline does not establish a trend, continued weakness in participation would likely become a more closely monitored indicator over coming months.

Professional and Business Services Led Private-Sector Hiring

Professional and business services once again provided one of the strongest contributions to overall Jobs growth.

Employment in the sector increased by 36,000, extending a trend that has persisted throughout much of the past year.

Demand remained particularly strong for occupations supporting business operations, consulting, administrative services and specialised professional expertise.

Despite slower overall payroll growth, businesses continue investing in productivity-enhancing roles rather than implementing widespread hiring freezes.

This resilience suggests many employers remain focused on long-term operational efficiency even as economic growth moderates.

Social Assistance Continued Expanding

Social assistance employment increased by 25,000, continuing one of the strongest hiring trends within the broader services sector.

Much of the growth reflected continued demand for individual and family services, community support programmes and childcare services.

The sector has consistently generated payroll gains as demographic changes and workforce participation continue supporting demand for essential community-based services.

Unlike more cyclical industries, social assistance employment tends to remain comparatively stable through changing economic conditions, providing an important source of ongoing employment growth.

Healthcare Hiring Remained Positive

Healthcare continued adding workers, with employment increasing by 22,000 during the month.

Although hiring remained solid, it represented a moderation compared with the sector’s stronger average monthly gains over the previous year.

Hospitals accounted for approximately 9,000 additional jobs, while broader healthcare services continued expanding as providers responded to sustained demand driven by population ageing and increased healthcare utilisation.

Healthcare remains one of the most resilient components of the labour market because demand is supported by long-term demographic trends rather than short-term economic cycles.

Even as broader hiring slows, healthcare continues generating consistent employment opportunities across clinical, technical and administrative occupations.

Leisure and Hospitality Recorded the Largest Decline

The weakest area of the Employment Report was leisure and hospitality.

The sector lost 61,000 jobs, making it the largest negative contributor to overall payroll growth during the month.

Restaurants, accommodation providers and entertainment businesses remain particularly sensitive to changes in discretionary consumer spending.

While the sector experienced rapid hiring during the economic reopening period, employment growth has become increasingly uneven as consumer spending patterns normalize and businesses focus more heavily on cost management.

Although one month’s decline does not necessarily indicate a lasting trend, it represents one of the more significant areas of weakness within the latest report.

Long-Term Unemployment Remains Elevated

The report also showed 1.9 million individuals remained unemployed for 27 weeks or longer.

Long-term unemployed workers represented a meaningful share of total unemployment and continue facing greater challenges returning to employment compared with individuals experiencing shorter periods without work.

Persistent long-term unemployment often reflects skills mismatches, geographic mobility constraints or changing industry demand.

Monitoring this measure remains important because prolonged unemployment can reduce future workforce participation and productivity.

Marginally Attached Workers Show Limited Change

Outside the official labour force, approximately 1.8 million people remained marginally attached to the labour market.

These individuals wanted employment and had searched for work within the previous year but were not actively seeking employment during the four weeks preceding the survey.

Within that group, 477,000 were classified as discouraged workers, indicating they believed suitable employment opportunities were unavailable.

Although these figures changed little over the month, they continue providing valuable context regarding underlying labour market conditions beyond the headline unemployment rate.

Average Hourly Earnings Continue to Support Income Growth

Wage growth remained broadly stable in the latest Employment Situation report, providing further evidence that labour market conditions continue to normalize without deteriorating.

Average hourly earnings for all private nonfarm employees increased by 8 cents to $36.30, while average hourly earnings rose 3.7% over the past 12 months.

The pace of annual wage growth continues to exceed inflation in many areas of the economy, allowing real household incomes to improve while avoiding the rapid acceleration in earnings that concerned policymakers during earlier stages of the inflation cycle.

For employers, moderating wage growth offers greater certainty around labour costs. Businesses remain willing to increase compensation to attract and retain skilled employees, but the pace of increases has become more consistent with longer-term productivity gains rather than labour shortages.

From a monetary policy perspective, wage growth of 3.7% is unlikely, on its own, to materially alter the Federal Reserve’s assessment of inflation. Instead, it reinforces the narrative that labour market conditions are gradually moving toward equilibrium.

Average Weekly Hours Were Little Changed

The report also showed little movement in average hours worked.

The average workweek for all private nonfarm employees remained at 34.2 hours, indicating employers have not materially adjusted working schedules despite slower hiring.

Manufacturing employees continued to average 40.1 hours per week, while overtime remained broadly unchanged.

Average hours worked are often viewed as an early indicator of changes in labour demand. Employers frequently reduce overtime or shorten workweeks before implementing broader workforce reductions. The stability seen in this month’s report therefore suggests businesses continue experiencing sufficient demand to maintain existing staffing levels.

Taken together with stable unemployment and positive payroll growth, the data indicate employers remain cautious but are not responding to a significant deterioration in business conditions.

Household Survey Presents a More Mixed Picture

While establishment payroll data continued to show employment growth, the household survey reflected a more subdued labour market.

Household employment declined during the month, contributing to the fall in the labour force participation rate and employment-population ratio. Divergences between the establishment and household surveys are not uncommon because they measure employment differently and are based on separate statistical samples.

The establishment survey counts payroll jobs reported by employers, while the household survey measures individuals who are employed, unemployed or outside the labour force.

Professional economists typically evaluate both surveys together rather than drawing conclusions from either in isolation.

Although the household survey softened during the month, it did not suggest the type of widespread labour market deterioration normally associated with an economic recession.

Payroll Revisions Remain an Important Part of the Employment Picture

Headline payroll numbers often receive the greatest attention immediately following release, but revisions to prior months can materially change the broader assessment of labour market conditions.

The Bureau of Labor Statistics routinely revises payroll estimates as additional employer data becomes available. These revisions help improve the accuracy of employment estimates but also remind investors that initial payroll figures should not be viewed in isolation.

Professional market participants therefore assess three key components simultaneously:

- Current month’s payroll gain.

- Revisions to previous months.

- Trends over a three- to six-month period.

The latest report continues to support the view that hiring has slowed gradually rather than abruptly, even after incorporating revised employment estimates.

Sector Performance Highlights a Rotating Labour Market

Rather than indicating broad-based weakness, the latest Employment Report illustrates a labour market undergoing sector rotation.

Healthcare, professional and business services, social assistance and government continue generating employment gains because underlying demand remains relatively resilient.

By contrast, leisure and hospitality, along with several consumer-sensitive industries, have experienced slower hiring as spending patterns normalize.

This divergence reflects changing economic conditions rather than systemic labour market weakness.

Businesses appear increasingly focused on productivity, profitability and operational efficiency rather than rapid workforce expansion.

Such behaviour is typical during the later stages of an economic cycle when demand remains positive but becomes more moderate.

Implications for the Federal Reserve

The latest NFP report is unlikely to materially alter the Federal Reserve’s broader policy framework, but it reinforces expectations that labour market conditions continue cooling in an orderly manner.

Several aspects of the report are likely to receive close attention from policymakers:

- Payroll growth remained positive.

- Unemployment held steady at 4.2%.

- Wage growth continued moderating.

- Participation declined modestly.

- Average hours worked remained stable.

Collectively, these indicators point to a labour market that is no longer exceptionally tight but continues to support economic expansion.

The Federal Reserve has consistently indicated that labour market rebalancing can occur through slower hiring rather than widespread layoffs. The latest Employment Report broadly aligns with that objective.

Future policy decisions will continue to depend on inflation, consumer spending, productivity and broader financial conditions rather than any single employment release.

Market Perspective

Financial markets often respond immediately to payroll data because employment influences expectations for interest rates, corporate earnings and economic growth.

A report showing slower—but still positive—payroll growth generally supports a more balanced market outlook.

For equity investors, continued employment growth supports household income and consumer spending, two critical drivers of corporate revenue.

Bond markets may interpret moderating payroll growth and stable wage gains as reducing the likelihood of renewed inflationary pressure.

Currency markets likewise assess employment data alongside inflation and central bank expectations when pricing future monetary policy.

Rather than providing a decisive signal in either direction, the latest Employment Report reinforces the view that the U.S. economy continues expanding while gradually returning to more sustainable labour market conditions.

Outlook

Looking ahead, labour market performance will remain closely tied to broader economic activity.

Employment growth is expected to continue moderating as businesses adjust hiring plans to reflect slower, but still positive, economic expansion.

Several sectors appear well positioned to continue supporting payroll growth, including healthcare, government, professional services and social assistance.

Meanwhile, industries more exposed to discretionary consumer spending and higher borrowing costs may continue experiencing greater month-to-month volatility.

Investors should continue monitoring several key indicators in future Employment Reports:

- Nonfarm Payroll growth.

- Unemployment rate.

- Labour force participation.

- Average hourly earnings.

- Average weekly hours.

- Revisions to previous payroll data.

- Sector-level employment trends.

Together, these measures provide a more complete picture of labour market conditions than the headline payroll figure alone.

Conclusion

The latest NFP report presents a picture of a labour market that continues to slow without signalling significant deterioration.

Payrolls increased by 57,000, unemployment remained at 4.2%, and wage growth continued at a moderate annual pace of 3.7%. While hiring has slowed compared with previous years, the data continue to indicate that employers are adding workers rather than reducing headcount on a broad scale.

Sector performance was mixed. Professional and business services, healthcare and social assistance remained key contributors to employment growth, while leisure and hospitality experienced a notable decline. Labour force participation eased, but average hours worked remained stable, suggesting employers continue maintaining existing workforces despite a more measured hiring environment.

For policymakers, the report supports the view that labour market conditions are gradually rebalancing. For investors, it reinforces expectations of continued economic expansion at a slower, more sustainable pace.

Although future reports will determine whether this trend persists, the latest Employment Situation release suggests the U.S. labour market remains resilient, with growth continuing despite tighter financial conditions and a more cautious hiring environment.

Frequently Asked Questions

How many Jobs did the latest NFP report add?

The latest Employment Situation report showed 57,000 new Nonfarm Payroll jobs.

What was the unemployment rate?

The unemployment rate remained unchanged at 4.2%.

How many people were unemployed?

Approximately 7.1 million people were unemployed during the survey period.

Which sectors added the most Jobs?

Professional and business services (+36,000), social assistance (+25,000) and healthcare (+22,000) recorded the strongest employment gains.

Which sector lost the most Jobs?

Leisure and hospitality recorded the largest decline, shedding 61,000 jobs.

How much did wages increase?

Average hourly earnings increased by 8 cents to $36.30, while annual wage growth measured 3.7%.

What was the labour force participation rate?

The labour force participation rate declined to 61.5%.

What does this report suggest about the economy?

The data indicate the labour market continues to cool gradually while remaining fundamentally resilient, supporting expectations of continued, but more moderate, economic growth.