FOMC Analysis: What the Latest FED Minutes Mean for Interest Rates and the U.S. Economy

The FOMC maintained a cautious policy stance during its June 16–17, 2026 meeting, with the latest FED Minutes showing broad agreement among policymakers that Interest Rates should remain restrictive until there is greater confidence that inflation is moving sustainably toward the Federal Reserve’s 2% objective.

The minutes indicate that while economic activity remains resilient and financial markets continue to perform well, policymakers remain concerned about inflation risks, labor market conditions, geopolitical developments, and the possibility that inflation could prove more persistent than previously anticipated.

Rather than signalling an imminent policy shift, the June meeting reinforced the Federal Reserve’s commitment to a data-dependent approach. Committee members acknowledged encouraging progress in several areas but concluded that current economic conditions continue to justify maintaining restrictive monetary policy until additional evidence supports future adjustments.

This analysis examines the key themes from the June 2026 FOMC meeting, the implications for Interest Rates, inflation, financial markets, and what investors should monitor over the coming months.

Key Takeaways

- The FOMC kept the federal funds rate unchanged.

- Policymakers continue to prioritise inflation over near-term rate reductions.

- Inflation has moderated but remains above the Federal Reserve’s long-term target.

- Economic growth continues at a solid pace despite restrictive monetary policy.

- Labour market conditions remain healthy, although gradual signs of cooling are emerging.

- Treasury yields increased during the intermeeting period.

- Equity markets remained resilient, led primarily by technology companies.

- Artificial intelligence investment continues to support business spending and earnings expectations.

- Future monetary policy decisions will remain dependent on incoming economic data.

Understanding the June 2026 FOMC Meeting

The June meeting reflected a Federal Reserve that remains patient rather than reactive. Committee members recognised that monetary policy has successfully slowed inflation from previous highs, but they also agreed that recent inflation data have not yet provided sufficient evidence to justify easing policy.

Throughout the discussion, policymakers repeatedly emphasised that risks remain balanced but uncertain. While economic growth has remained stronger than anticipated, stronger activity also carries the possibility of prolonging inflationary pressures.

The Committee therefore agreed that maintaining the current policy stance remains appropriate until additional data confirm that inflation is moving sustainably toward the Federal Reserve’s objective.

This cautious approach reflects one of the central themes of the latest FED Minutes: avoiding premature policy adjustments that could undermine progress made over the past several years.

Economic Activity Continues to Demonstrate Resilience

One of the more notable observations from the June meeting was the continued strength of the U.S. economy.

Despite elevated Interest Rates, overall economic activity has remained surprisingly resilient. Consumer spending has continued, business investment remains positive, and financial conditions have not tightened enough to materially slow overall growth.

Committee members discussed several factors supporting economic resilience, including:

- Stable household consumption

- Continued business investment

- Strong corporate earnings

- Improved supply chain conditions

- Robust technology investment

- Expanding artificial intelligence infrastructure spending

Although higher borrowing costs have moderated activity in certain interest-sensitive sectors, the broader economy continues to perform better than many forecasts anticipated earlier in the tightening cycle.

This resilience provides policymakers with greater flexibility to maintain restrictive monetary policy while monitoring incoming inflation data.

Inflation Remains the Primary Policy Concern

Inflation remained the dominant topic throughout the June FED Minutes.

While officials acknowledged that inflation has eased considerably from its peak, they agreed that recent data continue to show inflation above the Federal Reserve’s long-term objective.

Several participants expressed concern that underlying price pressures remain persistent in parts of the economy, particularly within service sectors.

Committee members also discussed several factors that could influence inflation over the coming quarters, including:

- Wage growth

- Housing costs

- Consumer demand

- Energy prices

- Global supply conditions

- Geopolitical developments

Although market-based inflation expectations declined following easing tensions surrounding the Middle East, policymakers cautioned that temporary improvements in commodity prices should not be interpreted as permanent reductions in inflation risk.

The Committee continues to expect inflation to gradually moderate, but members stressed that further progress is necessary before considering policy easing.

Interest Rates Are Expected to Remain Restrictive

The latest FOMC discussions reinforce that Interest Rates are likely to remain restrictive for an extended period.

Financial markets broadly anticipated no policy change during the June meeting, and the Committee delivered that outcome.

More importantly, discussions focused less on the timing of future rate reductions and more on maintaining flexibility should inflation remain elevated.

Survey participants generally expected the federal funds rate to remain unchanged into early 2027, with only modest expectations for future easing.

Market pricing also reflected higher expected policy rates compared with earlier in the year.

This shift illustrates how investors have gradually adjusted expectations toward a higher-for-longer interest rate environment.

For businesses and consumers, this means borrowing costs may remain elevated for longer than previously anticipated, affecting mortgage lending, commercial investment, and corporate financing decisions.

Labour Market Conditions Continue to Support the Economy

Employment conditions remain another source of confidence for policymakers.

The labour market continues to exhibit characteristics of a healthy economy, including relatively low unemployment, ongoing job creation, and steady wage growth.

However, the Committee also recognised early signs that labour market conditions are gradually becoming more balanced.

Among the developments discussed were:

- Moderating job openings

- Improved labour force participation

- Slower hiring in selected industries

- Continued wage growth without significant acceleration

This gradual adjustment is viewed positively because it suggests that labour market conditions are cooling without triggering widespread unemployment.

Such an outcome would improve the likelihood of achieving lower inflation while avoiding a severe economic slowdown.

Financial Markets Responded Positively Despite Policy Uncertainty

The June FED Minutes highlighted several notable developments across financial markets during the intermeeting period.

Equity markets continued to perform well despite elevated Interest Rates.

The S&P 500 advanced nearly six percent, with technology companies leading gains.

Higher earnings expectations, particularly among firms investing heavily in artificial intelligence infrastructure, contributed significantly to market performance.

Meanwhile:

- Treasury yields moved higher.

- The U.S. dollar strengthened.

- Expected policy rates increased modestly.

- Oil prices declined following reduced geopolitical tensions.

- Market-based inflation expectations eased.

Although these developments improved financial conditions in some areas, policymakers continue to monitor whether easier financial conditions could ultimately slow progress toward reducing inflation.

Artificial Intelligence Continues to Influence Economic Growth

One of the more interesting observations within the June minutes was the continued discussion surrounding artificial intelligence investment.

Committee members noted that ongoing investment in AI infrastructure has become an increasingly important driver of corporate spending.

Technology companies continue to allocate significant capital toward expanding computing capacity, data infrastructure, and software development.

These investments have supported stronger earnings expectations and contributed to the resilience observed across equity markets.

While AI is not currently a direct monetary policy consideration, its influence on productivity, business investment, and long-term economic growth is becoming increasingly important.

Policymakers will likely continue monitoring whether productivity improvements associated with AI contribute to stronger long-term economic growth while helping moderate inflationary pressures.

Treasury Yields Reflect Expectations for Higher Interest Rates

The June FOMC meeting minutes highlighted notable movements across U.S. Treasury markets during the intermeeting period. Rising Treasury yields reflected stronger economic data, improving investor confidence, and a reassessment of expectations regarding the future path of Interest Rates.

Longer-term Treasury yields increased as market participants concluded that policy easing may occur more gradually than anticipated earlier in the year. Investors adjusted their expectations to reflect the Federal Reserve’s continued commitment to returning inflation to its long-term objective before considering significant monetary policy accommodation.

Higher Treasury yields have important implications across financial markets because they influence borrowing costs for households, corporations, and governments. Mortgage rates, commercial lending, corporate bond issuance, and municipal financing all respond to movements in Treasury yields.

Committee members observed that financial markets have remained orderly despite the increase in yields. Demand for Treasury securities remains strong, reflecting continued confidence in U.S. financial markets even as borrowing costs remain elevated.

The minutes also noted that investors have become increasingly comfortable with the possibility that restrictive monetary policy could remain in place for an extended period. Rather than expecting rapid rate reductions, market participants now appear to anticipate a more gradual normalization process.

This adjustment has reduced some of the volatility that characterised earlier periods of monetary policy uncertainty.

Financial Conditions Have Eased Despite Restrictive Policy

One of the more interesting observations from the June FED Minutes is that overall financial conditions have become somewhat more accommodative despite unchanged Interest Rates.

Normally, restrictive monetary policy leads to tighter financial conditions through higher borrowing costs, lower equity valuations, wider credit spreads, and reduced liquidity. However, recent market developments have partially offset those restrictive effects.

Several factors contributed to easier financial conditions:

- Strong equity market performance

- Narrower corporate credit spreads

- Stable corporate financing conditions

- Improved investor confidence

- Continued capital investment

- Robust corporate earnings

From the Federal Reserve’s perspective, easier financial conditions can complicate efforts to reduce inflation. If financial markets become too optimistic, increased spending and investment could stimulate economic activity sufficiently to delay progress toward price stability.

For this reason, policymakers continue monitoring not only official economic data but also broader financial conditions when assessing the appropriate path for monetary policy.

Business Investment Continues to Support Economic Growth

Business investment remained an important area of discussion throughout the June meeting.

Despite elevated financing costs, many firms continue expanding operations and investing in productivity-enhancing technologies.

Several sectors were highlighted as demonstrating ongoing strength, including:

- Technology

- Manufacturing

- Energy

- Infrastructure

- Artificial intelligence

- Cloud computing

Businesses appear increasingly willing to undertake long-term investment projects despite higher financing costs because many view current investments as essential to maintaining future competitiveness.

The rapid expansion of artificial intelligence infrastructure remains particularly noteworthy.

Large technology firms continue investing billions of dollars in advanced computing facilities, semiconductor manufacturing, data centres, and software development. These investments have contributed significantly to stronger capital expenditure across the economy.

Committee members recognised that sustained business investment may improve long-term productivity growth while supporting employment and economic expansion.

Consumer Spending Remains Resilient

Household spending continues to represent one of the strongest pillars supporting U.S. economic growth.

Although higher Interest Rates have increased borrowing costs for mortgages, vehicle financing, and consumer credit, overall spending has remained relatively stable.

Several factors continue supporting household demand:

- Low unemployment

- Positive wage growth

- Rising household wealth

- Strong equity markets

- Stable consumer confidence

- Continued income growth

The Federal Reserve acknowledged that consumer spending has moderated somewhat compared with previous years but remains sufficiently strong to support continued economic expansion.

Committee members noted that resilient household demand has contributed to the economy’s ability to absorb higher interest rates without experiencing a significant downturn.

Housing Activity Continues to Face Pressure

Housing remains one of the sectors most directly affected by elevated Interest Rates.

Higher mortgage rates continue limiting affordability for many prospective homebuyers, resulting in slower transaction volumes across several regions.

The June FED Minutes indicated that housing activity remains subdued relative to historical averages.

Higher financing costs continue affecting:

- Residential construction

- Existing home sales

- Mortgage refinancing

- Housing affordability

- New home demand

Nevertheless, housing prices have generally remained supported by limited inventory and continued demographic demand.

The Federal Reserve continues monitoring housing closely because shelter costs remain an important component of overall inflation measures.

Any sustained moderation in housing inflation would provide additional evidence that broader price pressures continue easing.

Inflation Expectations Remain Well Anchored

One of the most encouraging themes within the June meeting involved inflation expectations.

Committee members noted that both market-based and survey-based measures of longer-term inflation expectations remain broadly consistent with the Federal Reserve’s long-term inflation objective.

Maintaining well-anchored inflation expectations is essential because expectations influence wage negotiations, business pricing decisions, and long-term investment planning.

If households and businesses expect inflation to remain elevated indefinitely, those expectations can become self-reinforcing.

Current evidence suggests that longer-term expectations remain relatively stable despite recent inflation volatility.

This provides policymakers with additional confidence that restrictive monetary policy continues producing its intended effects.

However, officials also acknowledged that short-term inflation expectations remain sensitive to developments involving:

- Energy prices

- Food prices

- Supply chain disruptions

- Geopolitical events

- Trade policies

These factors continue introducing uncertainty into the inflation outlook.

Global Developments Continue to Influence Monetary Policy

Although domestic economic conditions remain the Federal Reserve’s primary focus, international developments also received considerable attention during the June meeting.

Global economic activity continues affecting inflation, financial markets, and international capital flows.

Committee members discussed several external risks that could influence future policy decisions.

These include:

- Geopolitical tensions

- Commodity price volatility

- Global trade developments

- Exchange rate movements

- International supply chain disruptions

- Economic growth among major trading partners

While geopolitical tensions eased somewhat during the intermeeting period, policymakers acknowledged that global risks remain elevated.

Unexpected international developments could quickly affect inflation through energy prices, transportation costs, or disruptions to global supply chains.

Maintaining flexibility therefore remains an important element of current monetary policy.

Risk Assessment Remains Balanced but Uncertain

A recurring theme throughout the FOMC discussions was uncertainty.

Rather than identifying a single dominant economic risk, policymakers recognised that multiple competing risks continue influencing the outlook.

Among the upside risks discussed were:

- Persistent inflation

- Stronger-than-expected consumer spending

- Continued wage growth

- Easier financial conditions

- Rising asset prices

Potential downside risks included:

- Slowing global growth

- Weakening labour markets

- Reduced business investment

- Financial market volatility

- Geopolitical disruptions

This balanced assessment explains why the Committee continues emphasising a data-dependent approach rather than providing explicit forward guidance regarding future Interest Rates.

Incoming economic information will determine whether policy remains unchanged or requires future adjustment.

What the FOMC Minutes Mean for Investors

For investors, the June FED Minutes reinforce several important themes.

First, expectations for rapid interest rate reductions have become less likely.

Second, economic resilience continues supporting corporate earnings despite elevated borrowing costs.

Third, inflation remains the central variable influencing future monetary policy.

Investors should therefore continue monitoring:

- Consumer Price Index reports

- Personal Consumption Expenditures inflation

- Employment reports

- Wage growth

- Retail sales

- GDP growth

- Manufacturing activity

- Consumer confidence

Each of these indicators will influence future Federal Reserve decisions.

Rather than focusing solely on individual inflation reports, investors should evaluate the broader trend across multiple economic indicators.

The Federal Reserve has repeatedly emphasised that future decisions will depend upon cumulative evidence rather than isolated monthly data releases.

Implications for Financial Markets

The June meeting carries different implications across major asset classes.

Equities

Corporate earnings remain the primary driver of equity performance. Strong economic growth and continued investment in technology continue supporting valuations despite elevated interest rates.

Bonds

Bond investors should continue preparing for higher yields over the near term while monitoring inflation trends that could eventually support future policy easing.

U.S. Dollar

Higher relative interest rates continue supporting the U.S. dollar compared with many international currencies.

Gold

Gold prices remain influenced by inflation expectations, Treasury yields, and geopolitical developments. Persistent inflation concerns could continue supporting demand for defensive assets.

Corporate Credit

Credit markets remain healthy, with relatively narrow spreads reflecting investor confidence in corporate balance sheets and continued economic expansion.

Looking Ahead to the Next FOMC Meeting

As policymakers prepare for upcoming meetings, attention will remain focused on several critical economic indicators.

These include:

- Inflation data

- Employment reports

- Consumer spending

- Business investment

- Productivity growth

- Financial conditions

- Treasury market developments

- Global economic activity

The Federal Reserve has made it clear that future policy adjustments will depend on sustained evidence that inflation continues moving toward the 2% objective.

Until that evidence becomes more compelling, the Committee appears comfortable maintaining current Interest Rates while continuing to evaluate incoming economic data.

What to Watch Before the Next FOMC Meeting

While the June meeting did not produce any major surprises, it reinforced the Federal Reserve’s commitment to making policy decisions based on incoming economic data rather than market expectations or fixed timelines. As a result, investors, businesses, and policymakers will closely monitor several key indicators before the next FOMC meeting.

The most important reports include:

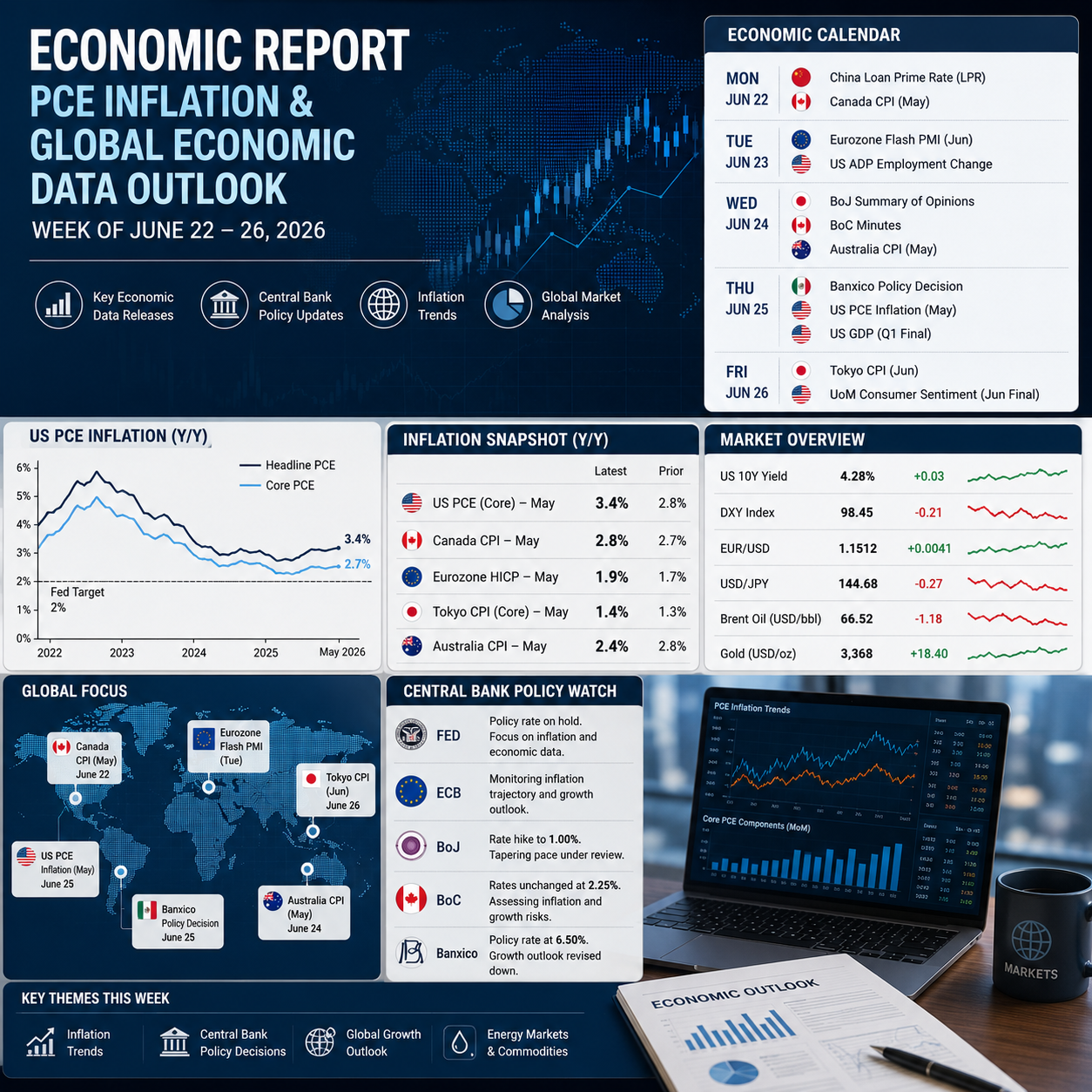

- Consumer Price Index (CPI)

- Personal Consumption Expenditures (PCE) Inflation

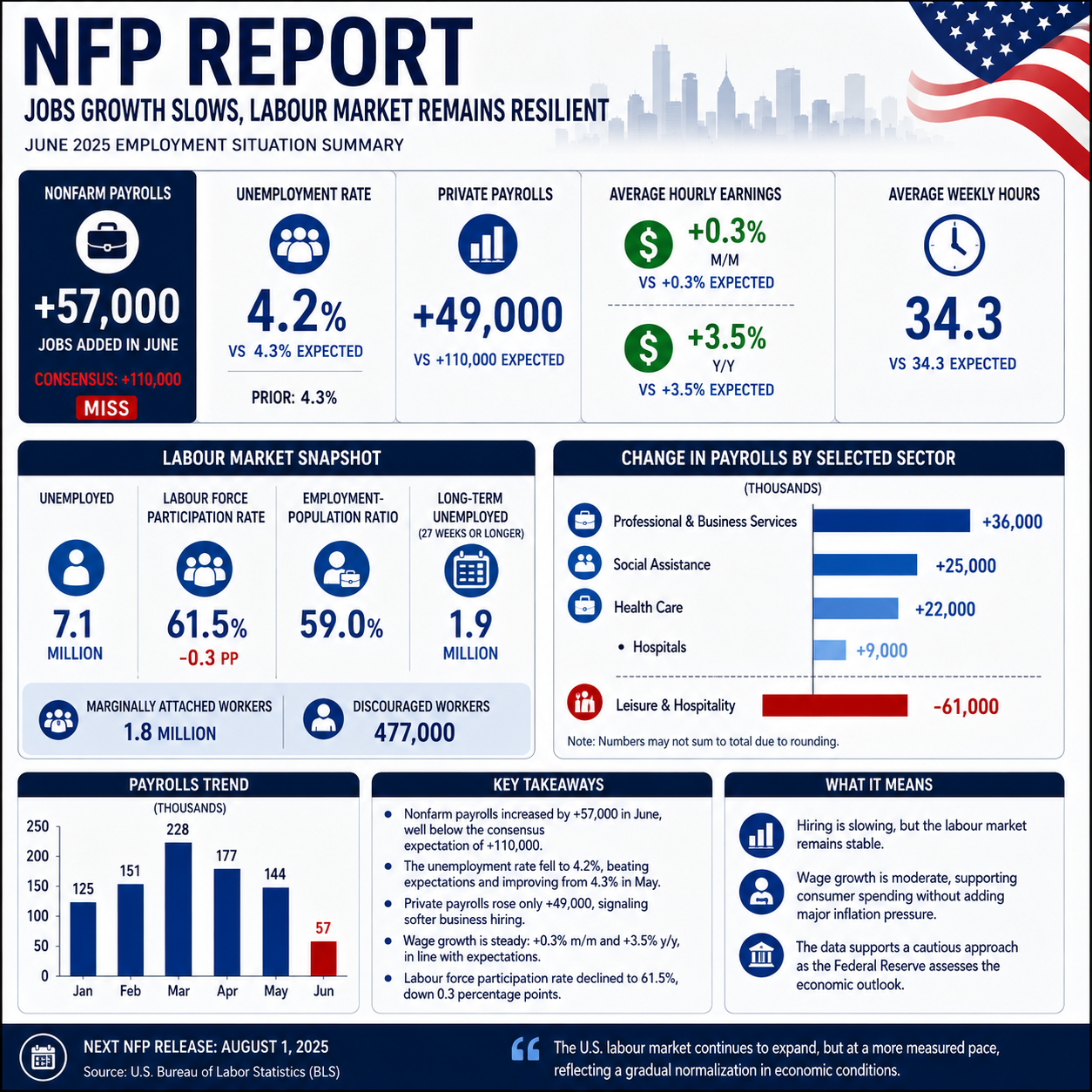

- Non-Farm Payrolls

- Unemployment Rate

- Average Hourly Earnings

- Retail Sales

- Gross Domestic Product (GDP)

- ISM Manufacturing and Services PMIs

- Housing Starts and Existing Home Sales

- Consumer Confidence

Each report provides another piece of the broader economic picture. Rather than reacting to one month’s data, the Federal Reserve has consistently indicated that it will evaluate trends over time before making any adjustments to Interest Rates.

Key Risks Identified in the FED Minutes

The June FED Minutes outlined several risks that could influence the economic outlook over the coming quarters.

Inflation Remains Above Target

Although inflation has declined significantly from previous highs, policymakers agreed that price growth remains above the Federal Reserve’s long-term objective. Any renewed increase in inflation could delay future policy easing.

Labour Market Strength

Employment remains resilient, supporting consumer spending and economic growth. However, if wage growth accelerates too quickly, inflationary pressures could persist longer than expected.

Financial Market Optimism

Strong equity markets and improving financial conditions may partially offset the effects of restrictive monetary policy by encouraging additional spending and investment.

Global Uncertainty

Geopolitical developments, trade policy, commodity prices, and global supply chains continue to present risks that could quickly influence inflation and economic growth.

Economic Growth

The U.S. economy continues to outperform many forecasts. While stronger growth is positive overall, it may also make inflation more difficult to reduce if demand remains elevated.

What This Means for Businesses

Businesses should continue planning for an environment where borrowing costs remain higher than the levels experienced before the tightening cycle began.

Companies considering expansion projects, acquisitions, or capital investments should continue evaluating financing strategies carefully. Although economic conditions remain favourable in many industries, elevated financing costs require greater discipline in capital allocation.

Businesses should also continue monitoring labour costs, supply chain developments, and consumer demand as these factors will influence profitability over the coming quarters.

What This Means for Consumers

For consumers, the June FOMC meeting suggests that interest-sensitive borrowing costs may remain elevated for some time.

Mortgage rates, auto loans, credit cards, and other consumer lending products continue reflecting the current monetary policy environment.

However, the strong labour market continues supporting household incomes, while moderating inflation is gradually improving purchasing power.

Consumers should continue expecting monetary policy decisions to remain dependent on economic conditions rather than predetermined timelines.

Overall Assessment of the June FOMC Meeting

The June 2026 meeting reinforced a message that has become increasingly consistent throughout the Federal Reserve’s recent communications.

The economy continues demonstrating resilience.

Inflation continues moving in the right direction but remains above target.

Employment remains healthy.

Financial markets continue functioning effectively.

Taken together, these conditions provide policymakers with the flexibility to maintain current Interest Rates while waiting for additional evidence that inflation is returning sustainably toward 2%.

The FED Minutes do not suggest an immediate shift in policy. Instead, they highlight a disciplined and measured approach that prioritises long-term price stability while recognising the strength of the broader economy.

For investors, businesses, and consumers, the primary takeaway is that monetary policy remains firmly data dependent. Future adjustments will be determined by inflation, employment, and broader economic conditions rather than market expectations alone.

Frequently Asked Questions

1. What is the FOMC?

The Federal Open Market Committee (FOMC) is the Federal Reserve’s monetary policy committee responsible for setting the target range for the federal funds rate and guiding U.S. monetary policy.

2. What are the FED Minutes?

The FED Minutes are the official summary of discussions held during each FOMC meeting. They provide additional insight into policymakers’ views, economic assessments, and the factors influencing monetary policy decisions.

3. Why are Interest Rates important?

Interest Rates influence borrowing costs for consumers and businesses, affecting mortgages, credit cards, business loans, investment decisions, and overall economic activity.

4. Did the June 2026 FOMC meeting change Interest Rates?

No. The Committee voted to maintain the existing target range while continuing to evaluate incoming economic data before making future policy adjustments.

5. Why is inflation still the Federal Reserve’s primary concern?

Although inflation has moderated, it remains above the Federal Reserve’s 2% target. Policymakers want greater confidence that inflation is moving sustainably lower before easing monetary policy.

6. What does “higher for longer” mean?

It refers to maintaining restrictive Interest Rates for an extended period to ensure inflation returns to target without requiring additional policy tightening later.

7. How do the FED Minutes affect financial markets?

Investors analyse the Minutes for clues about future monetary policy. Changes in expectations regarding Interest Rates can influence stocks, bonds, currencies, and commodity prices.

8. Could Interest Rates increase again?

The Federal Reserve has not ruled out additional tightening if inflation unexpectedly accelerates. Future decisions remain dependent on economic data.

9. What indicators will the FOMC monitor before its next meeting?

Officials will focus on inflation reports, employment data, consumer spending, GDP growth, financial conditions, and broader economic developments.

10. What is the main takeaway from the June FED Minutes?

The Committee believes the economy remains resilient but continues to require restrictive monetary policy until inflation demonstrates sustained progress toward the Federal Reserve’s long-term objective.

Conclusion

The June 2026 FOMC meeting provided a comprehensive assessment of an economy that continues to perform better than many expected despite restrictive monetary policy.

The FED Minutes demonstrate that policymakers remain encouraged by progress on inflation but are not yet prepared to declare victory. Maintaining current Interest Rates allows the Federal Reserve to preserve flexibility while continuing to evaluate incoming economic data.

Economic growth remains steady, labour market conditions remain favourable, and financial markets continue operating efficiently. At the same time, inflation has not yet returned to the Federal Reserve’s long-term objective, making patience the defining characteristic of current monetary policy.

Looking ahead, future policy decisions will continue to depend on the balance between inflation, employment, and economic growth. Investors, businesses, and consumers should expect the Federal Reserve to remain focused on achieving lasting price stability while supporting sustainable long-term economic expansion.