Economic Report Overview

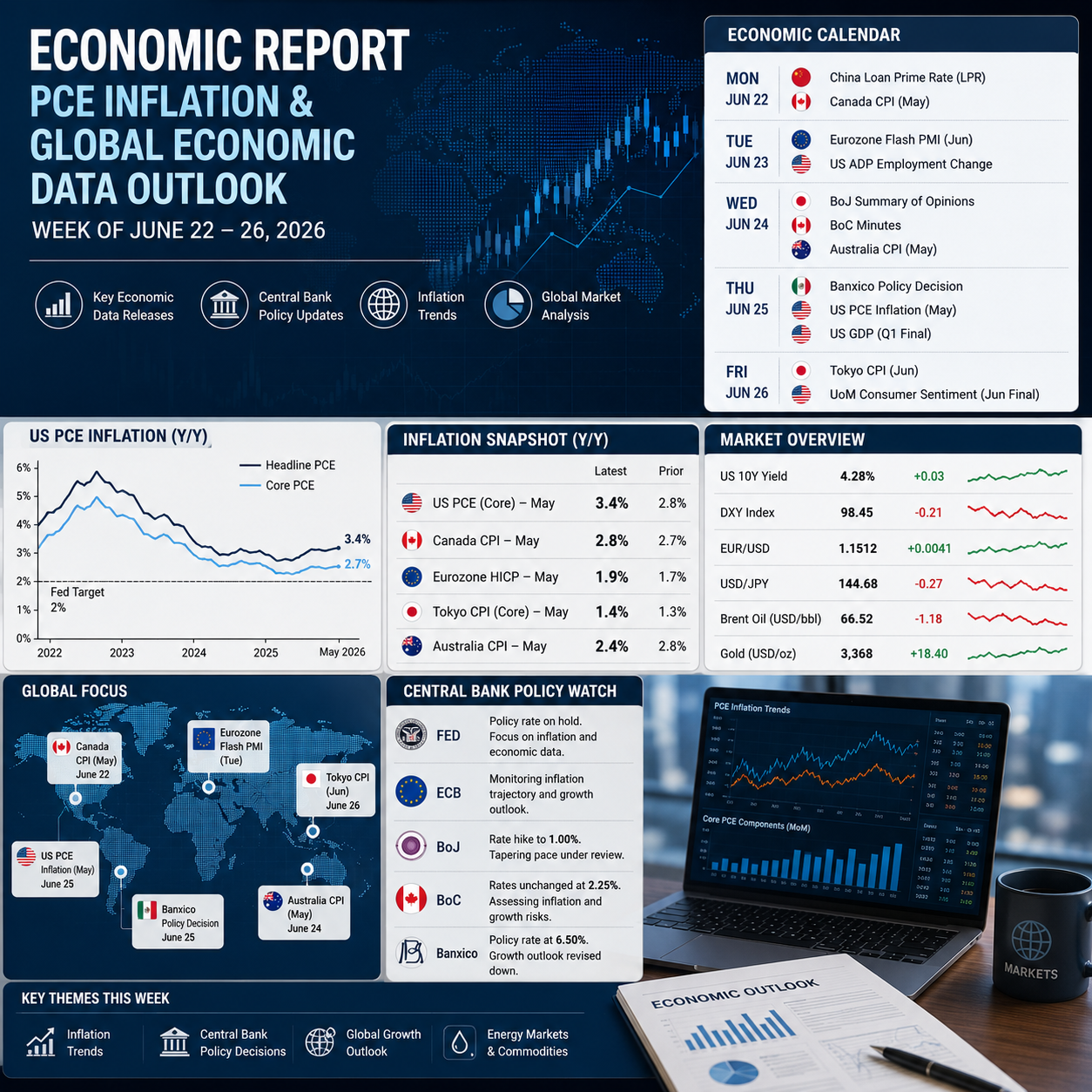

Economic Report analysis for the week of June 22-26 focuses on a broad range of inflation indicators, economic activity surveys, labour market releases and central bank communications across the major economies. While several important data points are scheduled throughout the week, the US PCE inflation report remains one of the most relevant releases for assessing the Federal Reserve’s inflation outlook and policy direction.

In addition to US PCE inflation, market participants will review Canadian CPI, Eurozone Flash PMIs, Tokyo CPI, Australian inflation data and the latest Banxico policy decision. These releases collectively provide insight into price pressures, consumer demand, business activity and monetary policy trends across developed and emerging markets.

Recent central bank meetings have highlighted a continued emphasis on inflation management. The Federal Reserve, Bank of Japan, Reserve Bank of Australia and several European central banks have maintained a cautious approach as policymakers evaluate incoming data and assess whether inflation is moving sustainably toward target levels.

This Economic Report examines the week ahead, reviews current expectations and discusses the potential implications for monetary policy and financial markets.

Key Economic Events for June 22-26

| Day | Event |

|---|---|

| Monday | Chinese Loan Prime Rate, Canadian CPI |

| Tuesday | Global Flash PMIs, Richmond Fed Index |

| Wednesday | Australian Inflation, German Ifo, BoC Minutes |

| Thursday | Banxico Decision, Australian Jobs, US PCE |

| Friday | Tokyo CPI, Canadian Wholesale Sales, US Trade Data |

The schedule includes a combination of inflation indicators, activity surveys and central bank communications that will help shape expectations for future interest rate decisions.

Chinese Loan Prime Rate Expected to Remain Unchanged

The People’s Bank of China is expected to maintain both the one-year and five-year Loan Prime Rates at current levels.

The one-year Loan Prime Rate currently stands at 3.00%, while the five-year rate remains at 3.50%. These benchmarks continue to serve as reference rates for corporate lending and mortgage financing across China.

Recent policy actions suggest Chinese authorities remain focused on liquidity management rather than benchmark rate adjustments. The central bank has increased liquidity support through open market operations and has signalled a willingness to use shorter-term instruments to influence financial conditions.

Recent Chinese economic data presents a mixed picture. Export growth has remained relatively firm, while retail sales have weakened. Industrial production has exceeded expectations, but consumer demand remains uneven.

For investors, the significance of the Chinese Loan Prime Rate announcement may lie less in the actual decision and more in any accompanying signals regarding future liquidity operations or broader economic support measures.

Canadian Inflation Data and Bank of Canada Expectations

Canadian inflation figures for May will be released at the beginning of the week and will provide updated information regarding price developments within the Canadian economy.

The Bank of Canada has indicated that inflation could remain around 3% in the near term before gradually moving closer to its 2% objective. Policymakers have also stated that they are monitoring whether energy-related price increases become embedded in broader inflation measures.

Energy markets have changed considerably since the previous inflation release. Crude oil prices declined substantially during May and have remained under pressure following improvements in geopolitical conditions.

This development may reduce the influence of energy costs on future inflation readings and could support expectations that inflation pressures will moderate over time.

Several components of the Canadian inflation report deserve attention:

- Headline CPI

- Core CPI

- Services inflation

- Shelter costs

- Food prices

- Energy-related components

If inflation remains broadly contained, policymakers may feel comfortable maintaining a patient approach. However, evidence of persistent price pressures within core inflation categories could influence future policy discussions.

The Bank of Canada minutes scheduled later in the week may provide additional insight into how policymakers are assessing inflation risks and economic growth prospects.

Global Flash PMIs Provide Insight into Economic Activity

Purchasing Managers’ Index surveys from major economies will offer one of the earliest indications of economic activity during June.

The Flash PMI reports cover both manufacturing and services sectors and are closely monitored because they provide timely information about business conditions.

Recent PMI surveys have highlighted several recurring themes:

- Slower manufacturing activity

- Resilient service sector demand

- Elevated input costs

- Ongoing pricing pressures

- Mixed business confidence

For the Eurozone, market participants will be particularly interested in whether lower energy prices improve business sentiment and reduce inflation concerns.

The relationship between PMI surveys and inflation remains important. If companies continue reporting higher input costs and stronger pricing power, central banks may view inflation risks as remaining elevated.

Conversely, evidence of softer demand and easing price pressures could support expectations for a more balanced inflation outlook.

As a result, PMI data often influences both growth expectations and monetary policy forecasts.

Australian Inflation Report

Australia’s monthly inflation release will be one of the week’s most important indicators for the Reserve Bank of Australia.

Current forecasts suggest inflation may moderate during May, supported by lower fuel prices and softer cost pressures in several sectors.

The Reserve Bank of Australia has maintained a cautious stance regarding inflation and has repeatedly emphasised that inflation remains above its preferred range.

Several factors will influence the inflation outcome:

Energy Prices

Lower fuel prices have provided some relief to households and businesses. This may contribute to softer headline inflation readings.

Consumer Demand

Survey evidence suggests many businesses continue absorbing cost increases rather than passing them directly to consumers.

Underlying Inflation

The trimmed mean measure remains the preferred indicator for policymakers because it excludes temporary price fluctuations.

If underlying inflation remains elevated, the Reserve Bank may maintain a restrictive policy stance for longer.

If inflation slows more quickly than expected, discussions regarding future policy adjustments could become more balanced.

Bank of Canada Minutes

The release of Bank of Canada meeting minutes will provide additional detail regarding the June policy decision.

At the previous meeting, policymakers left interest rates unchanged while reiterating their commitment to controlling inflation.

The minutes may reveal several important themes:

- Assessment of inflation risks

- Views regarding labour market conditions

- Concerns surrounding economic growth

- Impact of energy prices

- Trade-related uncertainties

Recent employment data showed stronger labour market performance than expected, while inflation data has generally remained moderate.

This combination creates a policy environment in which officials may prefer to wait for additional evidence before considering further action.

Investors will review the minutes carefully for any indication regarding future policy direction and the balance of risks facing the Canadian economy.

Australian Employment Data

Employment data scheduled for Thursday will provide another important input for Reserve Bank of Australia policy assessments.

Labour market conditions remain relatively firm despite slower economic growth.

Economists expect a recovery in employment growth following the previous month’s decline.

Key metrics include:

- Employment change

- Unemployment rate

- Participation rate

- Full-time employment

- Part-time employment

The Reserve Bank has consistently highlighted inflation rather than employment as its primary concern. Nevertheless, labour market strength remains relevant because it can influence wage growth and consumer spending.

A stronger-than-expected report could reinforce expectations that economic activity remains sufficiently resilient to support current policy settings.

A weaker outcome may contribute to expectations that inflation pressures will continue to moderate.

Banxico Policy Decision

Mexico’s central bank is expected to leave interest rates unchanged at 6.50%.

Recent policy communications suggest officials believe current policy settings are broadly appropriate given the inflation outlook and economic growth conditions.

Although inflation has moved lower compared with previous years, policymakers remain attentive to potential risks.

At the same time, economic growth has slowed, creating a policy environment that requires careful balancing between inflation management and economic activity.

Market participants will focus on:

- Rate decision

- Policy statement

- Inflation forecasts

- Growth projections

- Forward guidance

Any changes in language regarding inflation or economic growth may influence expectations for future policy adjustments.

US PCE Inflation Remains the Primary Focus

The US PCE inflation report scheduled for Thursday is expected to be the most closely analysed release in this Economic Report. Personal Consumption Expenditures inflation is the Federal Reserve’s preferred measure of inflation because it captures a broader range of consumer spending behaviour and adjusts for substitution effects that may not be fully reflected in the Consumer Price Index.

Recent inflation reports have indicated that price pressures remain above the Federal Reserve’s long-term objective. While some components of inflation have moderated, policymakers continue to monitor whether inflation is returning sustainably toward the 2% target.

Current estimates suggest that core PCE inflation could increase by approximately 0.3% to 0.4% on a monthly basis. On an annual basis, the measure is expected to remain above the Federal Reserve’s preferred range.

Several components are likely to influence the report:

Housing and Shelter Costs

Housing-related inflation continues to represent an important component of overall price growth. Although some measures of rent inflation have moderated, shelter costs remain elevated relative to historical averages.

Services Inflation

Services inflation remains one of the most persistent areas of inflation across the US economy. Labour-intensive sectors continue to experience wage-related cost pressures.

Goods Prices

Goods inflation has generally eased compared with previous years, although supply chain disruptions and trade-related developments remain potential sources of volatility.

Energy Prices

Energy prices increased during parts of May but subsequently declined. This may result in some divergence between headline and core inflation measures.

The Federal Reserve has repeatedly stated that inflation remains a primary consideration when evaluating monetary policy decisions. As a result, the US PCE report will likely play an important role in shaping expectations regarding future interest rate decisions.

Federal Reserve Policy Outlook Following PCE Inflation

The latest Federal Reserve meeting reinforced the institution’s commitment to price stability.

Policymakers maintained interest rates while emphasising that inflation remains above target and requires continued monitoring. Updated projections also suggested a more cautious approach toward future policy adjustments.

Several themes emerged from recent Federal Reserve communications:

- Inflation remains above target.

- Economic growth continues.

- Labour market conditions remain relatively stable.

- Policymakers remain data dependent.

- Price stability remains a priority.

This Economic Report highlights that future policy decisions will depend heavily on incoming inflation data.

Should US PCE inflation exceed expectations, markets may reassess the likelihood of policy easing. Conversely, evidence of sustained disinflation could support a more balanced policy outlook.

The Federal Reserve has consistently communicated that decisions will be guided by economic data rather than predetermined policy paths.

For this reason, inflation releases remain among the most influential indicators for financial markets.

Japanese Tokyo CPI and Bank of Japan Policy Considerations

Tokyo Consumer Price Index data scheduled for Friday provides an early indication of inflation trends across Japan.

The Bank of Japan recently increased its policy rate to 1.00%, marking its highest level in several decades. Despite this adjustment, Japanese monetary policy remains accommodative relative to many other developed economies.

Consensus expectations suggest that Tokyo CPI may increase modestly due to:

- Higher energy costs

- Exchange rate effects

- Consumer price adjustments

- Gradual demand recovery

Government support measures have helped moderate some energy-related inflation pressures, contributing to relatively stable headline inflation readings.

The Bank of Japan continues to signal that future policy decisions will depend on developments in:

- Inflation

- Economic activity

- Financial conditions

- Wage growth

Should inflation continue moving higher, expectations regarding additional policy tightening may increase.

However, policymakers have emphasised that any future adjustments will be gradual and data dependent.

Eurozone Economic Outlook

The Eurozone enters the week with investors focusing on Flash PMI surveys and broader inflation trends.

Recent economic data has reflected uneven growth across the region. Manufacturing activity has remained subdued while service-sector activity has demonstrated greater resilience.

Several factors continue to influence the Eurozone outlook:

Energy Costs

Energy markets remain an important variable for inflation and business activity throughout Europe.

Consumer Spending

Consumer demand has shown gradual improvement as inflation has moderated from previous peaks.

Industrial Activity

Manufacturing activity remains under pressure in some sectors, particularly export-oriented industries.

Monetary Policy

The European Central Bank continues to evaluate incoming inflation and growth data when determining policy settings.

The Flash PMI surveys will provide additional information regarding business confidence and economic momentum heading into the second half of the year.

Economic Report Assessment of Global Inflation Trends

A common theme throughout this Economic Report is the continued importance of inflation across major economies.

While inflation rates have generally moved lower from their peak levels, progress toward central bank targets remains uneven.

Several observations can be made:

Inflation Has Moderated

Most major economies have experienced lower inflation rates compared with previous years.

Services Inflation Remains Persistent

Services inflation continues to represent a challenge for many central banks.

Energy Prices Remain Influential

Energy markets continue to affect both headline inflation and inflation expectations.

Labour Markets Remain Important

Employment conditions influence wage growth and consumer spending patterns.

Monetary Policy Remains Restrictive

Many central banks continue to maintain relatively restrictive policy settings.

These factors suggest inflation will remain an important consideration for policymakers throughout the remainder of the year.

Central Bank Policy Developments

Several central banks are represented in this Economic Report.

Each institution faces unique economic circumstances, but several common themes are evident.

Federal Reserve

Focused on returning inflation to target while maintaining economic stability.

Bank of Canada

Monitoring inflation developments while evaluating economic growth conditions.

Bank of Japan

Continuing a gradual normalisation process following years of accommodative policy.

Reserve Bank of Australia

Maintaining a strong focus on inflation and underlying price pressures.

Banxico

Balancing inflation objectives against slower economic growth.

Collectively, these institutions continue to emphasise data dependency and flexibility when evaluating future policy decisions.

Implications for Financial Markets

Economic data releases influence expectations across multiple asset classes.

Foreign Exchange Markets

Currency markets often react to inflation surprises and changes in interest rate expectations.

Fixed Income Markets

Bond yields frequently adjust in response to inflation data and central bank communications.

Equity Markets

Stock market performance may be influenced by growth expectations and policy outlooks.

Commodity Markets

Energy and commodity prices remain closely linked to inflation developments and global growth conditions.

This Economic Report suggests that inflation-related releases are likely to remain among the most influential drivers of market sentiment.

Key Themes to Monitor During the Week

Several themes warrant attention throughout the week.

Inflation Persistence

The extent to which inflation remains elevated will continue influencing policy expectations.

Economic Growth

PMI surveys and activity indicators will provide insight into global growth conditions.

Labour Markets

Employment reports remain important for assessing economic resilience.

Central Bank Communication

Minutes, policy statements and official comments may influence market expectations.

Consumer Demand

Retail activity and inflation data provide valuable information regarding household spending patterns.

These themes collectively shape the broader macroeconomic outlook.

Frequently Asked Questions

What is the most important release in this Economic Report?

The US PCE inflation report is likely to receive the greatest attention because it is the Federal Reserve’s preferred inflation measure.

Why is PCE inflation important?

PCE inflation provides a broad measure of consumer price changes and plays an important role in Federal Reserve policy decisions.

What are Flash PMIs?

Flash Purchasing Managers’ Index surveys provide early estimates of business activity in manufacturing and services sectors.

Why is Canadian CPI important?

Canadian CPI helps assess inflation trends and may influence future Bank of Canada policy decisions.

What is the significance of Tokyo CPI?

Tokyo CPI is often viewed as an early indicator of inflation developments across Japan.

What is expected from Banxico?

Banxico is widely expected to maintain its policy rate while providing updated guidance regarding inflation and economic growth.

How do inflation reports affect markets?

Inflation data influences interest rate expectations, bond yields, currency valuations and broader financial market sentiment.

Why do central banks focus on inflation?

Central banks seek price stability because stable inflation supports sustainable economic growth and financial stability.

Conclusion

Economic Report analysis for June 22-26 highlights a week filled with important inflation indicators, economic activity surveys and central bank developments across major economies.

The primary focus remains US PCE inflation, which will provide updated information regarding underlying price pressures and may influence expectations for future Federal Reserve policy decisions. Alongside PCE inflation, investors will review Canadian CPI, Eurozone Flash PMIs, Australian inflation, Tokyo CPI and the latest Banxico policy announcement.

Recent central bank communications have demonstrated that inflation remains a key policy consideration despite progress made in reducing price pressures from previous highs. Policymakers continue to evaluate incoming data while balancing inflation objectives against economic growth considerations.

This Economic Report suggests that inflation trends, business activity indicators and central bank communications will remain central themes for market participants throughout the week. As additional data becomes available, attention will remain focused on whether inflation continues moving toward target levels and how central banks adjust their policy outlooks in response to evolving economic conditions.