Economic Report Overview

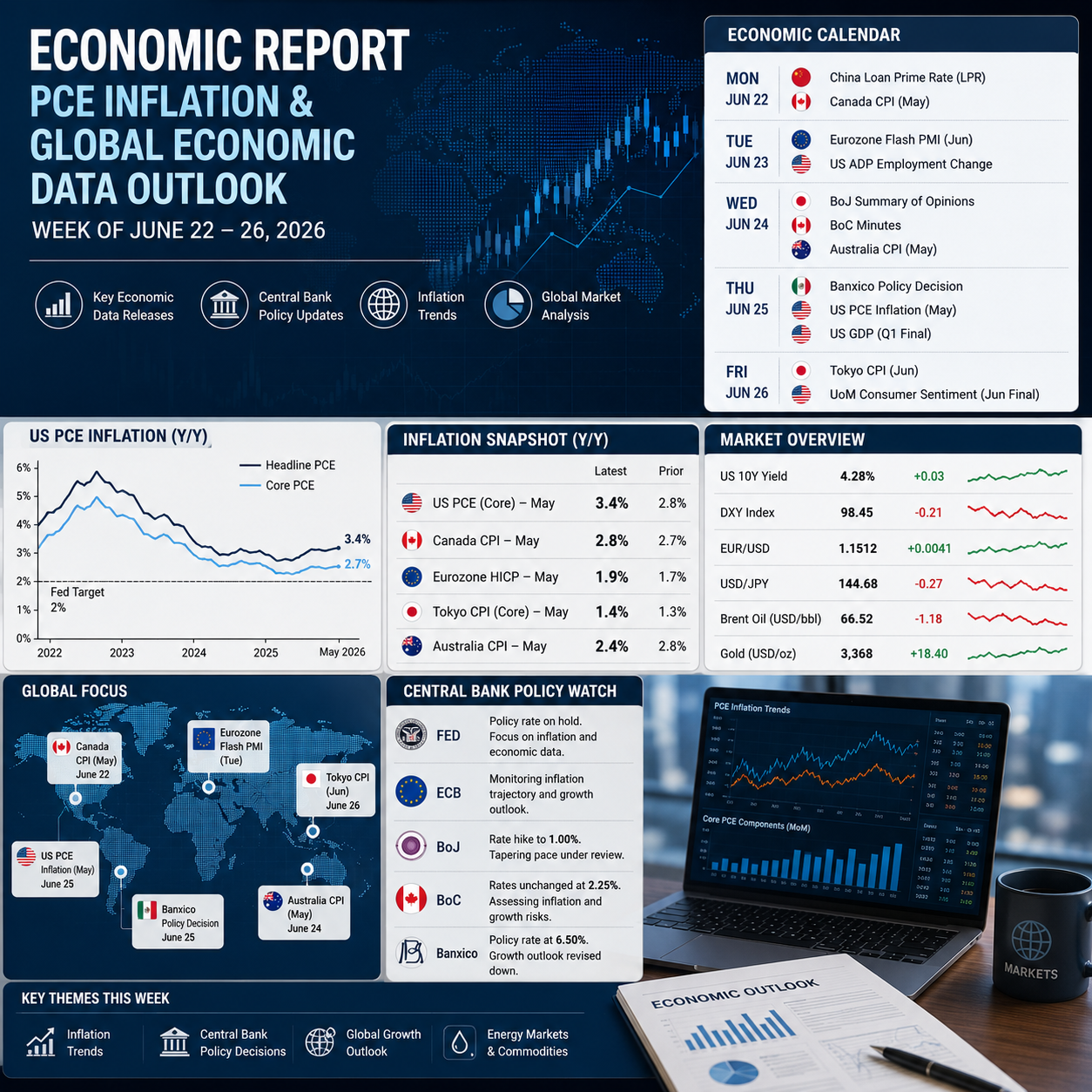

Economic Report: The week ahead presents one of the busiest economic calendars of the quarter, with investors closely monitoring a series of high-impact releases that are likely to influence expectations for interest rates, economic growth and financial markets. Attention will centre on the United States labour market, highlighted by the June US Non-Farm Payrolls (US NFP) report, alongside the ISM Manufacturing PMI, Eurozone inflation data and several important releases from Asia-Pacific economies.

Following a week in which inflation data continued to shape central bank expectations, markets now face another critical test. Employment figures, manufacturing activity, inflation reports and central bank communications will provide valuable insight into whether global economic momentum remains resilient or whether signs of slowing growth are becoming more pronounced.

For traders and investors across equities, fixed income, foreign exchange and commodities, this week’s data has the potential to reshape expectations for monetary policy during the second half of the year.

Economic Calendar: Key Events This Week

| Day | Key Releases |

|---|---|

| Monday | Japanese Retail Sales, Spanish HICP Flash, Eurozone Consumer Confidence, US Dallas Fed Manufacturing Index |

| Tuesday | RBA Minutes, Chinese Manufacturing PMI, German Inflation, Canadian GDP, US JOLTS Job Openings |

| Wednesday | Japanese Tankan Survey, Eurozone Flash CPI, ADP Employment, ISM Manufacturing PMI |

| Thursday | Swiss CPI, Eurozone Unemployment, US NFP Report, Weekly Jobless Claims, Factory Orders |

| Friday | US Independence Day Holiday, Eurozone Services PMI Final, French Industrial Production, Italian Retail Sales |

Several releases stand out as potential market movers, particularly the US NFP report, ISM Manufacturing PMI and Eurozone inflation figures, all of which may influence expectations surrounding future policy decisions from the Federal Reserve and the European Central Bank.

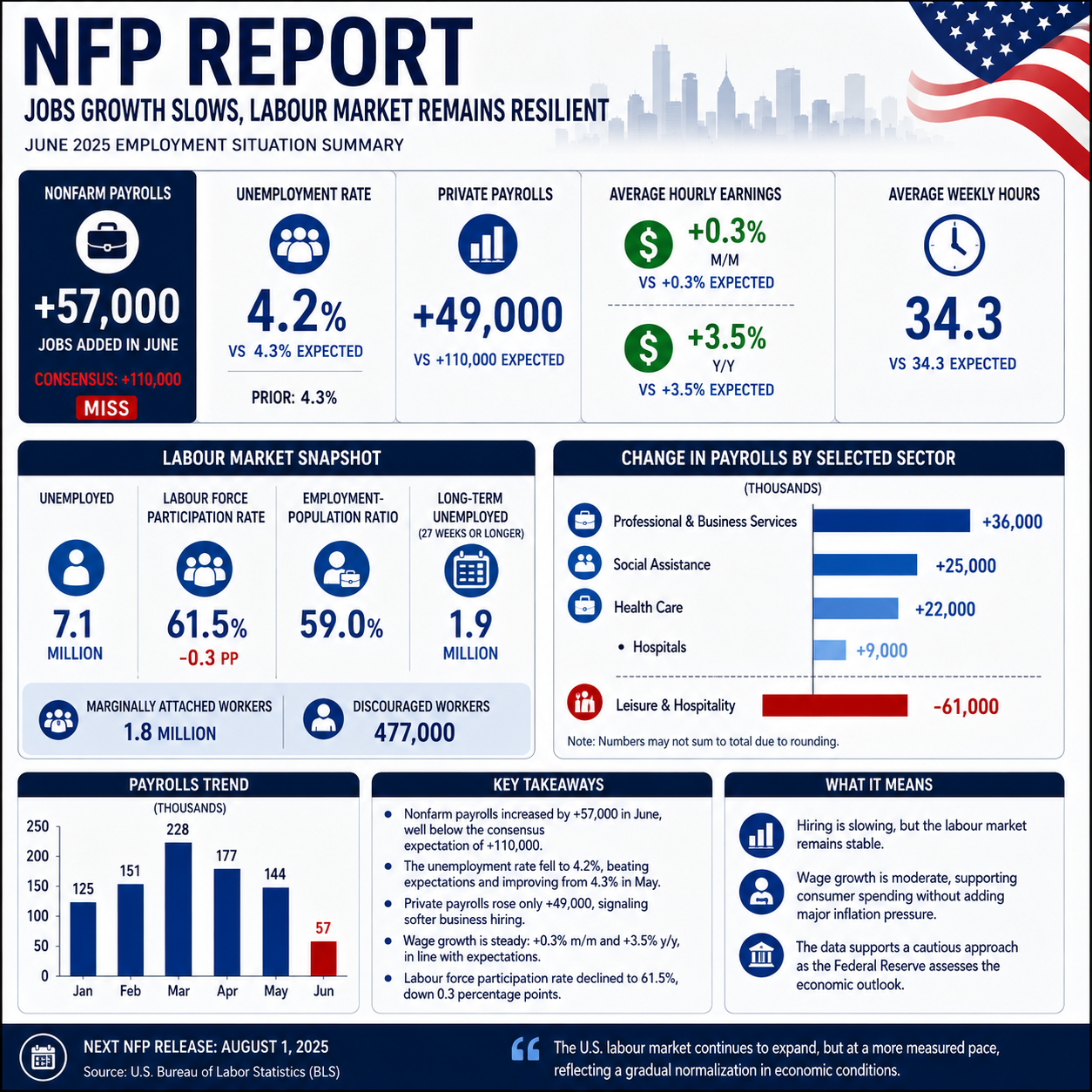

US NFP Preview: Labour Market Remains in Focus

The June US NFP report will be the headline release of the week and is expected to provide another important assessment of labour market conditions in the United States.

Consensus forecasts suggest payroll growth moderated during June after stronger hiring in the previous month. Economists generally expect approximately 115,000 new jobs to have been created, compared with 172,000 in May. While this would represent slower hiring, it would still indicate that the labour market remains relatively resilient despite tighter monetary policy and elevated borrowing costs.

The previous report benefited from unusually strong hiring within local government employment. Many analysts believe that temporary support is unlikely to be repeated, suggesting a more moderate headline figure this month.

The unemployment rate is expected to remain close to 4.3%, reflecting a labour market that continues to soften gradually rather than deteriorate sharply. Average hourly earnings are forecast to increase by approximately 0.3% month-on-month, keeping wage growth elevated enough to remain relevant for inflation expectations.

For Federal Reserve policymakers, the combination of employment growth, unemployment and wage inflation remains central to future policy decisions. A stronger-than-expected report would reinforce the argument that labour market conditions remain healthy, potentially delaying expectations for interest rate cuts. Conversely, weaker hiring combined with softer wage growth could strengthen expectations that inflation pressures will continue to ease over coming months.

Investors should also remain aware of temporary factors that may influence the June data. Some economists have noted that employment associated with preparations for the 2026 FIFA World Cup may provide a modest boost to payroll numbers before reversing later in the year.

Rather than focusing exclusively on the headline payroll figure, markets will likely assess the broader report, including revisions to previous months, labour force participation, unemployment and wage growth, to develop a more complete picture of underlying labour market conditions.

ISM Manufacturing PMI: Can Factory Activity Sustain Momentum?

Alongside the labour market, manufacturing activity remains another critical indicator of broader economic conditions.

Recent survey data have pointed towards improving factory activity. Preliminary purchasing managers’ surveys showed manufacturing output reaching multi-year highs, supported by stronger production and an increase in new orders.

However, the underlying picture remains more complex than headline figures suggest.

Part of the recent strength appears to reflect businesses accelerating orders ahead of potential supply chain disruptions and higher import costs rather than sustained improvements in final demand. Geopolitical tensions, shipping disruptions and tariffs have encouraged firms to rebuild inventories, temporarily boosting manufacturing activity.

Input costs also remain elevated, with businesses continuing to report rising prices for raw materials and longer supplier delivery times.

Export demand remains comparatively weak, suggesting external demand has yet to recover fully.

Employment within manufacturing has also softened despite stronger production, indicating that companies remain cautious regarding future economic conditions.

The ISM Manufacturing PMI will therefore receive close attention, not only for the headline reading but also for its individual components, including:

- New Orders

- Employment

- Prices Paid

- Production

- Supplier Deliveries

- Inventories

Together, these indicators provide valuable insight into inflationary pressures, business confidence and the health of the broader industrial sector.

Eurozone CPI: Inflation Remains Central to ECB Policy

Inflation remains the dominant consideration for the European Central Bank, making the June Flash Consumer Price Index one of the week’s most significant releases.

Headline inflation previously matched expectations, although underlying inflation measures surprised slightly to the upside, particularly within the services sector. Persistent service inflation continues to present challenges for policymakers seeking confidence that price pressures are easing sustainably.

Recent business surveys suggest price pressures may be stabilising. Lower energy prices have begun filtering through supply chains, while softer economic activity has reduced some pricing power across several industries.

Even so, inflation dynamics remain uneven across the Eurozone.

Countries continue to experience differing rates of price growth depending on domestic demand, wage developments and energy exposure. Consequently, investors will monitor not only the aggregate Eurozone figure but also inflation readings from Germany, France, Spain and Italy.

For the European Central Bank, incoming inflation data will influence expectations regarding future policy meetings. While officials have emphasised a data-dependent approach, evidence of moderating inflation could strengthen confidence that restrictive monetary policy is gradually achieving its objective.

Conversely, another upside surprise—particularly within core inflation—would likely reinforce expectations that interest rates may need to remain elevated for longer.

Swiss CPI: Stable Inflation Supports a Patient Approach

Switzerland’s inflation outlook remains comparatively subdued relative to many advanced economies.

Recent inflation readings have eased, helped by lower energy prices and stable domestic demand. Analysts generally expect June inflation to remain contained, supporting the Swiss National Bank’s current policy stance.

Although policymakers recently revised medium-term inflation projections slightly higher, inflation continues to remain well below levels experienced elsewhere.

Unless inflation unexpectedly accelerates, markets broadly anticipate that Swiss monetary policy will remain relatively stable over coming months, providing investors with another useful comparison against larger central banks currently managing more persistent inflation challenges.

RBA Minutes: Policy Still Data Dependent but Vigilant

The latest Economic Report attention turns to Australia, where the Reserve Bank of Australia (RBA) Minutes will provide important context around the central bank’s current policy stance and risk assessment.

At its most recent meeting, the RBA held the cash rate steady at 4.35%, maintaining a cautious approach after a series of tightening decisions earlier in the cycle. The decision was unanimous, reinforcing the sense of internal agreement around the current policy path. However, the tone of communication remained firm, with policymakers continuing to stress that inflation remains too high and that monetary policy must remain restrictive for a longer period if necessary.

The RBA Minutes are expected to shed light on how policymakers are interpreting recent inflation data, which has shown signs of persistence in underlying measures despite some moderation in headline figures. Of particular importance will be any discussion around services inflation and wage growth, both of which remain central to the inflation outlook in Australia.

The Australian economy continues to display a mixed profile. While labour market conditions have softened modestly, they remain relatively tight by historical standards. Consumer demand has slowed under the pressure of higher interest rates, yet housing-related inflation remains sticky, limiting the scope for rapid policy easing.

Global factors are also playing an important role. Energy price volatility and geopolitical developments have contributed to uncertainty in imported inflation dynamics, which the RBA continues to monitor closely.

Market participants will be looking for any signal that the central bank is shifting either toward a more neutral stance or maintaining a firmly restrictive bias. At present, expectations remain anchored around a prolonged pause rather than imminent easing, with policy decisions likely to remain highly data dependent through the remainder of the year.

Japan Tankan Survey: Business Sentiment Under Scrutiny

The Japanese Tankan Survey will be another key focus in this week’s Economic Report, offering a timely snapshot of business sentiment across the world’s third-largest economy.

The previous survey showed improving sentiment among large manufacturers, with confidence rising for several consecutive quarters. However, expectations for the upcoming release are more cautious, as analysts anticipate a modest weakening in sentiment.

A number of factors are contributing to this outlook. Rising energy prices, persistent global uncertainty and supply chain disruptions have all placed pressure on corporate margins. Additionally, recent geopolitical developments have raised concerns about potential trade and shipping disruptions, which could weigh on export-oriented sectors of the Japanese economy.

Manufacturing firms are particularly sensitive to fluctuations in global demand. While domestic conditions have shown gradual improvement, external demand remains uneven, especially from key trading partners in Europe and parts of Asia.

The Tankan index will be closely watched for signs of whether business confidence is holding up or beginning to soften. Even small changes in sentiment can influence expectations for future investment and hiring decisions, making this survey a key forward-looking indicator for Japanese economic momentum.

The Bank of Japan continues to face a delicate balancing act between supporting economic recovery and gradually normalising monetary policy. As a result, the Tankan data will be important in shaping expectations around the timing and pace of any future policy adjustments.

Week in Review: Inflation and Policy Signals Dominate

Before turning to the week ahead in full detail, it is important to reflect on recent developments that continue to shape the broader macroeconomic backdrop.

In China, the decision to hold benchmark lending rates steady was widely expected, reflecting a continued preference for targeted liquidity management rather than broad rate cuts. Policymakers have increasingly relied on short-term liquidity tools to guide financial conditions, while maintaining a cautious stance on formal rate adjustments.

In Canada, inflation data showed a mixed picture. Headline inflation accelerated due largely to energy prices, while core measures remained more stable. The data suggests that inflationary pressures remain uneven, with shelter inflation easing but other components proving more resilient.

Australia’s inflation report delivered a similar theme. While headline CPI came in softer than expected, underlying measures remained slightly elevated. This reinforces the view that disinflation is progressing, but not uniformly across all categories.

In Europe, flash PMI data indicated that economic activity remains resilient, particularly in services. However, manufacturing continues to lag, reflecting ongoing weakness in global industrial demand. Price pressures appear to be stabilising, though not yet fully subdued.

Japan’s monetary policy communication also remained notably hawkish in tone, with several policymakers signalling openness to further tightening if inflation and wage dynamics continue to evolve in line with forecasts.

Together, these developments reinforce a global economic environment characterised by slow but uneven disinflation, modest growth and continued reliance on central bank guidance.

Global Market Outlook: What This Economic Report Means for Investors

This Economic Report highlights a week where macroeconomic data could significantly influence expectations for monetary policy across multiple major economies.

In the United States, attention will remain firmly anchored on the labour market. The US NFP report is likely to be the single most influential release, not only for assessing economic momentum but also for shaping expectations around the Federal Reserve’s next policy steps. A stronger labour market would reinforce the narrative of resilience, while softer data could strengthen the case for a more dovish outlook later in the year.

Manufacturing data, particularly the ISM PMI, will provide additional insight into the balance between demand and supply conditions in the US economy. Investors will be watching closely for signs of whether recent strength in production is sustainable or driven primarily by temporary factors.

In the Eurozone, inflation data will remain central to European Central Bank policy expectations. The balance between easing price pressures and persistent services inflation will be critical in determining whether current policy settings remain appropriate.

Elsewhere, central bank communications from Australia and Japan will continue to shape expectations around global interest rate differentials. While neither central bank is expected to make immediate policy changes, their forward guidance will be important in shaping medium-term market pricing.

Overall, the Weekly Market Outlook suggests a data-dependent environment where macroeconomic surprises have the potential to drive volatility across currencies, bond yields and equity markets.

Investors should therefore approach the coming week with a focus on key data releases rather than broad macro narratives, as the next set of figures may provide clearer direction on the global economic cycle.

Frequently Asked Questions (FAQs)

1. What is the Economic Report?

The Economic Report is a weekly macroeconomic summary highlighting key global data releases, central bank decisions and market-moving economic indicators.

2. Why is US NFP important?

US NFP is a key measure of employment in the United States and plays a major role in shaping Federal Reserve interest rate expectations.

3. What does ISM Manufacturing PMI measure?

ISM Manufacturing PMI tracks activity in the US manufacturing sector, including production, employment and new orders.

4. How does Eurozone CPI affect markets?

Eurozone CPI measures inflation across the region and influences European Central Bank monetary policy decisions.

5. What is the Weekly Market Outlook?

The Weekly Market Outlook summarises expected macroeconomic events and their potential impact on global financial markets.

6. How do central bank minutes impact markets?

Central bank minutes provide insight into policy discussions and can shift expectations around future interest rate decisions.

Conclusion

This Economic Report underscores a pivotal week for global financial markets, with key data releases including US NFP, manufacturing activity indicators and inflation figures across major economies.

As central banks continue to navigate uneven disinflation and moderating growth, incoming data will play a decisive role in shaping policy expectations.

The overall Weekly Market Outlook remains highly data-sensitive, with the potential for volatility across asset classes depending on how closely economic outcomes align with forecasts.

")