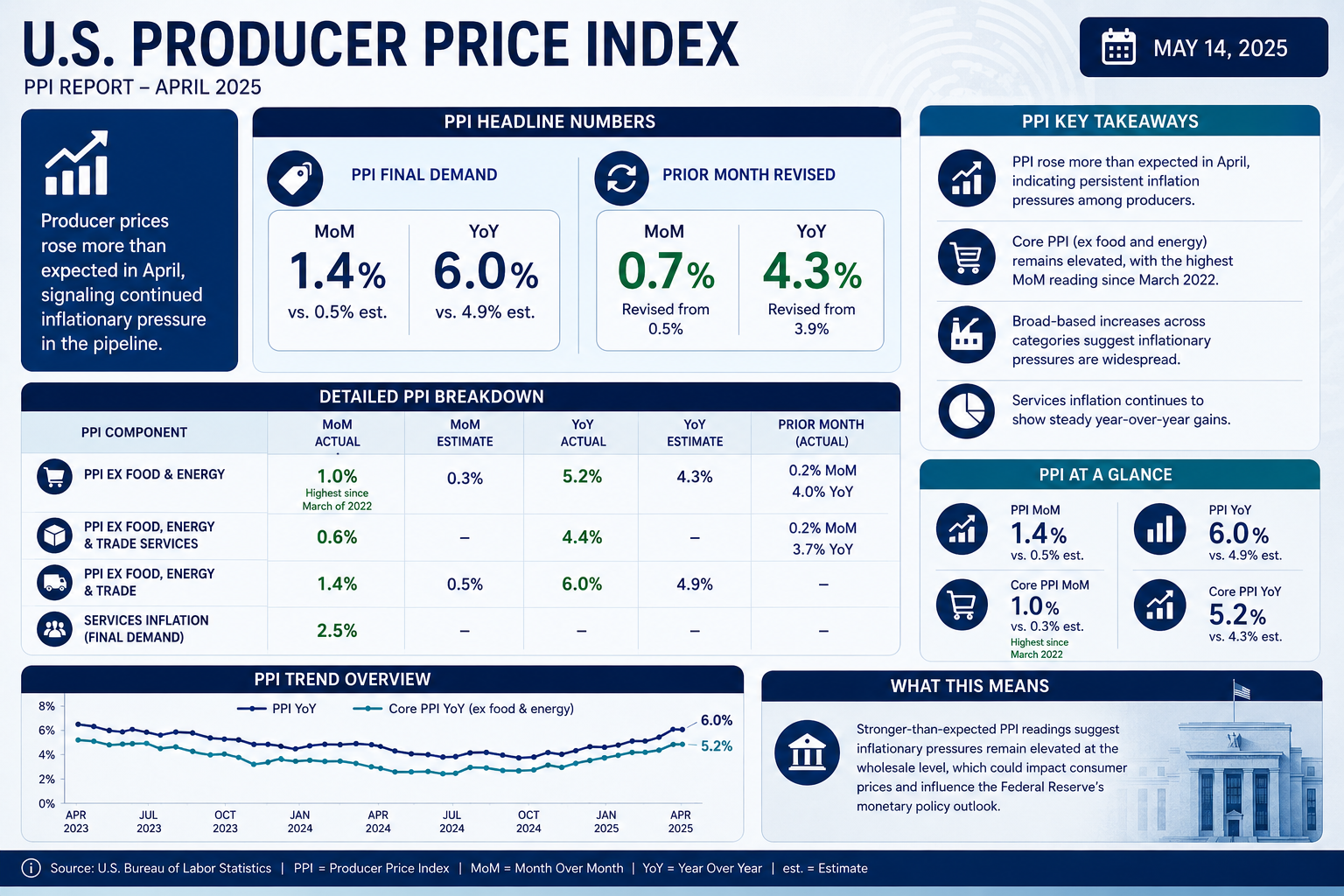

PPI Jumps Higher in April as Inflation Pressures Reaccelerate

PPI moved sharply higher in April 2026, signaling renewed inflation pressure across the United States economy. The latest Producer Price Index report showed that wholesale prices increased faster than economists expected, driven largely by rising energy costs, transportation expenses, and accelerating trade service margins. The report immediately raised concerns across financial markets regarding inflation persistence, future interest rates, and the outlook for the USD.

The April PPI report showed final demand prices increased 1.4% month over month, the largest monthly gain since March 2022. On an annual basis, PPI climbed 6.0%, representing the strongest yearly increase since late 2022. The data reinforced growing fears that inflation may remain elevated longer than previously anticipated.

Energy prices played a central role in the latest PPI surge. Gasoline prices jumped more than 15%, while diesel fuel, jet fuel, and crude petroleum prices also rose sharply. These increases filtered throughout supply chains and intensified broader inflation concerns across transportation, manufacturing, logistics, and industrial production.

At the same time, stronger PPI data complicated the Federal Reserve’s interest rate outlook. Markets had expected gradual easing later in 2026, but persistent inflation pressure may force policymakers to maintain higher interest rates for longer. As a result, the USD strengthened as investors adjusted expectations for monetary policy.

The latest PPI report also highlighted a growing divergence between producer costs and consumer affordability. While producers continue facing rising input costs, businesses may increasingly pass these expenses onto consumers, potentially keeping CPI inflation elevated throughout the remainder of the year.

Financial markets responded quickly. Treasury yields moved higher, equity markets experienced volatility, and the USD gained strength against major currencies as investors reassessed inflation and interest rate expectations.

The April data suggests inflation pressures are no longer limited to isolated sectors. Instead, broad-based price increases are appearing across goods, services, transportation, warehousing, and intermediate demand stages throughout the economy.

What Is PPI and Why Markets Closely Watch It

PPI measures the average change in prices received by domestic producers for goods and services over time. Unlike CPI, which tracks prices paid by consumers, PPI reflects inflation from the producer perspective. Because businesses often pass higher costs onto consumers, PPI is widely viewed as a leading indicator of future inflation trends.

When PPI rises rapidly, markets typically expect higher consumer inflation in future months. This relationship makes PPI especially important for the Federal Reserve, bond markets, currency traders, and institutional investors.

The Bureau of Labor Statistics organizes PPI into several major categories:

- Final demand goods

- Final demand services

- Intermediate demand goods

- Intermediate demand services

- Energy products

- Transportation and warehousing

- Trade services

The latest report showed broad inflation pressure across nearly every major category. Final demand services rose 1.2%, while final demand goods climbed 2.0%. Intermediate demand categories also posted substantial gains, signaling continued pipeline inflation pressures.

The importance of PPI extends beyond inflation analysis. Markets use PPI to evaluate:

- Corporate profit margins

- Manufacturing costs

- Supply chain conditions

- Federal Reserve policy expectations

- Interest rate direction

- USD strength

- Commodity price trends

When PPI rises faster than expected, investors often anticipate tighter monetary policy and stronger USD performance. That relationship became increasingly visible after the April release.

Energy Prices Became the Main Driver Behind the PPI Surge

Energy inflation dominated the latest PPI report. The final demand energy index surged 7.8% in April following a 10.1% increase in March. Energy for export rose 15.8%, while government-purchased energy climbed 12.1%.

The largest contributor was gasoline, which jumped 15.6% during the month. Diesel fuel and jet fuel prices also increased sharply, reflecting stronger global demand, supply disruptions, and elevated geopolitical risks.

Energy inflation affects nearly every sector of the economy because fuel costs influence:

- Transportation

- Manufacturing

- Shipping

- Industrial production

- Agriculture

- Logistics

- Consumer goods pricing

As fuel prices rise, companies face higher operating costs. Businesses then either absorb lower profit margins or pass those costs onto consumers through higher prices.

The latest PPI report showed this transmission process clearly. Transportation and warehousing services surged 5.0%, while truck transportation of freight increased significantly. Freight forwarding and courier services also moved higher.

This matters because transportation inflation often spreads quickly through broader supply chains. Rising delivery costs increase prices for retailers, manufacturers, wholesalers, and eventually consumers.

Crude petroleum prices rose 11.3% during April, while processed energy goods climbed 7.8%. These gains suggest energy inflation may remain elevated in coming months, especially if oil markets remain tight.

Natural gas prices showed mixed performance, with some categories declining while others increased depending on market segment exposure.

The persistence of energy inflation creates a difficult challenge for policymakers because energy shocks can quickly reignite broader inflation expectations.

PPI Signals Inflation Pressures Are Expanding Across the Economy

The April PPI report showed inflation pressures are no longer isolated to a few sectors. Instead, price increases are spreading across goods, services, transportation, intermediate demand, and industrial supply chains.

Final demand services increased 1.2%, representing the largest monthly gain since March 2022. Trade service margins rose sharply, particularly in machinery, chemicals, fuels, and wholesale sectors.

Intermediate demand indexes also accelerated:

- Processed goods rose 2.7%

- Unprocessed goods climbed 4.1%

- Intermediate services increased 1.1%

These numbers matter because intermediate demand reflects costs businesses face before final production reaches consumers. When intermediate demand rises quickly, future consumer inflation risks often increase as well.

Several important categories posted significant gains:

| Sector | Monthly Increase |

|---|---|

| Gasoline | 15.6% |

| Crude Petroleum | 11.3% |

| Diesel Fuel | 12.6% |

| Transportation Services | 5.0% |

| Freight Transportation | 8.1% |

| Energy for Export | 15.8% |

The broad-based nature of the increases suggests inflation remains deeply embedded within the economy.

Markets are especially focused on “core” measures that exclude food, energy, and trade services. Even these categories moved higher, indicating underlying inflation remains firm despite previous Federal Reserve tightening efforts.

Final demand less foods, energy, and trade services increased 0.6%, marking the largest rise since October 2025.

This suggests inflation is not solely dependent on volatile energy prices. Core pricing pressures remain persistent across broader economic activity.

Interest Rates May Stay Higher for Longer After the PPI Report

The stronger-than-expected PPI report significantly impacted interest rate expectations. Investors now believe the Federal Reserve may delay future rate cuts if inflation continues accelerating.

Higher PPI data creates several challenges for policymakers:

- Inflation remains above target

- Energy costs are rising again

- Supply chain inflation is returning

- Services inflation remains sticky

- Producer costs continue climbing

The Federal Reserve closely watches inflation indicators like PPI when determining interest rate policy. If wholesale inflation continues rising, policymakers may keep rates elevated longer than markets previously expected.

Higher interest rates influence the economy in multiple ways:

- Borrowing costs increase

- Mortgage rates remain elevated

- Business investment slows

- Consumer spending weakens

- Credit conditions tighten

- USD strength improves

Following the report, Treasury yields moved higher as investors adjusted policy expectations.

The possibility of prolonged high interest rates creates additional pressure on financial markets because equities typically perform worse when borrowing costs remain elevated.

Growth-oriented sectors such as technology often face the greatest sensitivity to changing interest rate expectations.

At the same time, higher rates can strengthen the USD by attracting foreign capital seeking higher returns on U.S. assets.

USD Strengthened as Markets Reacted to Higher PPI

The USD strengthened following the release of the April PPI data. Currency traders interpreted the report as a sign that the Federal Reserve may maintain restrictive monetary policy for longer.

Higher interest rate expectations generally support the USD because investors seek stronger returns from U.S. Treasury assets and dollar-denominated investments.

Several factors supported USD strength after the report:

- Higher Treasury yields

- Delayed rate cut expectations

- Rising inflation concerns

- Stronger economic resilience

- Persistent energy inflation

The relationship between PPI and USD performance remains important because inflation directly impacts central bank policy.

If inflation remains elevated:

- Interest rates stay higher

- Treasury yields increase

- USD demand strengthens

- Capital flows toward dollar assets

However, sustained USD strength also creates challenges for multinational corporations and emerging markets. A stronger dollar can reduce export competitiveness while increasing debt servicing costs globally.

Currency markets now expect inflation data to remain one of the primary drivers of USD volatility throughout 2026.

Transportation and Supply Chain Inflation Returned Strongly

One of the most important developments within the PPI report was the sharp rise in transportation and logistics costs.

Transportation and warehousing services increased 5.0% during April, reflecting higher freight expenses, fuel costs, and shipping demand.

Truck transportation of freight rose 8.1%, while freight forwarding and courier services also moved sharply higher.

This trend matters because transportation inflation often spreads quickly across the economy. Rising shipping costs affect:

- Retail pricing

- Manufacturing expenses

- Food distribution

- Consumer products

- Industrial supply chains

- International trade

During previous inflation cycles, transportation inflation became a major contributor to persistent price increases throughout the broader economy.

The return of higher logistics costs raises concerns that supply chain inflation may be reaccelerating after moderating during 2024 and 2025.

If energy prices remain elevated, transportation inflation could continue rising throughout the second half of 2026.

Why Markets Care About Intermediate Demand Data

Intermediate demand data often receives less public attention than headline PPI numbers, but institutional investors closely monitor these categories because they provide insight into future inflation trends.

The April report showed strong increases across all four production stages:

| Production Stage | Monthly Increase |

|---|---|

| Stage 1 | 2.1% |

| Stage 2 | 2.8% |

| Stage 3 | 2.3% |

| Stage 4 | 0.9% |

These increases indicate inflation pressure is building throughout multiple levels of production.

When early-stage costs rise:

- Manufacturers pay more

- Producers raise prices

- Retailers face margin pressure

- Consumers eventually absorb higher costs

The strong gains in processed and unprocessed goods suggest pipeline inflation remains active.

Crude petroleum, industrial chemicals, electronic components, and plastic materials all experienced notable increases.

This broad industrial inflation supports the view that inflation may remain persistent despite slower economic growth.

PPI and CPI Could Diverge in the Months Ahead

Although PPI often influences CPI, the two indexes do not always move together immediately.

Several factors can create temporary divergence:

- Corporate margin compression

- Consumer resistance to higher prices

- Government subsidies

- Inventory adjustments

- Import pricing dynamics

- Currency fluctuations

However, sustained PPI increases usually place upward pressure on future CPI readings over time.

Businesses facing higher producer costs eventually attempt to protect profitability by raising consumer prices.

The latest report suggests this risk is growing again, particularly in:

- Energy

- Transportation

- Industrial goods

- Wholesale trade

- Manufacturing inputs

If CPI follows PPI higher during coming months, expectations for Federal Reserve easing could weaken further.

That scenario would likely support higher Treasury yields and additional USD strength.

Financial Markets Face Renewed Inflation Uncertainty

The April PPI report increased uncertainty across financial markets.

Investors now face several major questions:

- Will inflation remain elevated longer?

- Can the Federal Reserve still cut rates in 2026?

- Will energy prices continue rising?

- Can corporate margins withstand higher costs?

- Will USD strength continue?

These questions matter because inflation directly affects:

- Equity valuations

- Bond prices

- Currency markets

- Commodity prices

- Corporate earnings

- Consumer confidence

Higher inflation generally creates a more difficult environment for risk assets.

Bond markets become especially sensitive because rising inflation reduces the purchasing power of future fixed-income payments.

At the same time, commodity markets often benefit from sustained inflation pressures, particularly energy-related sectors.

Corporate Margins May Come Under Pressure

The latest PPI report also raises concerns about corporate profitability.

Businesses now face:

- Higher energy costs

- Rising transportation expenses

- Increasing input prices

- Elevated wage pressure

- Tight financing conditions

Companies unable to pass higher costs onto consumers may experience shrinking profit margins.

Industries with heavy energy exposure appear particularly vulnerable, including:

- Airlines

- Transportation firms

- Manufacturing companies

- Chemical producers

- Industrial suppliers

Retailers may also face pressure if consumers resist additional price increases after several years of elevated inflation.

Margin compression could become a major theme during upcoming earnings seasons if producer costs continue rising.

Federal Reserve Policy Outlook After the PPI Report

The Federal Reserve now faces a more complicated policy environment.

Before the latest PPI release, markets expected several possible interest rate cuts during late 2026. However, persistent inflation pressures may force policymakers to delay easing plans.

The Fed’s primary concerns now include:

- Persistent core inflation

- Energy price volatility

- Services inflation strength

- Wage growth

- Inflation expectations

If inflation remains elevated:

- Interest rates may stay restrictive

- Financial conditions remain tight

- Economic growth could slow

- USD strength may continue

At the same time, policymakers must avoid overtightening the economy into recession.

This balancing act will likely define monetary policy discussions throughout the remainder of 2026.

Conclusion

The April 2026 PPI report delivered a strong warning that inflation pressures remain deeply embedded within the U.S. economy. Rising energy prices, accelerating transportation costs, and broad-based producer inflation are creating renewed concerns about interest rates, Federal Reserve policy, and USD strength.

PPI increased at the fastest monthly pace since 2022, reinforcing fears that inflation may stay elevated longer than markets previously expected.

Energy remains the primary driver behind the latest inflation surge, but the broader expansion across goods, services, transportation, and intermediate demand categories suggests inflation risks are becoming increasingly widespread.

The report significantly impacted financial market expectations. Treasury yields rose, the USD strengthened, and investors reassessed the likelihood of future interest rate cuts.

Moving forward, markets will closely monitor whether rising PPI eventually feeds into higher CPI inflation. If producer costs continue accelerating, the Federal Reserve may face growing pressure to maintain higher interest rates for longer.

The April data confirms that inflation remains one of the defining macroeconomic themes of 2026, with important implications for markets, businesses, consumers, and policymakers alike.

FAQ

What is PPI?

PPI stands for Producer Price Index. It measures changes in prices received by producers for goods and services over time.

Why is PPI important?

PPI helps investors and policymakers track inflation trends before they reach consumers through CPI inflation.

Why did PPI rise in April 2026?

The biggest drivers were rising energy prices, gasoline costs, transportation expenses, and broader supply chain inflation.

How does PPI affect interest rates?

Higher PPI can lead the Federal Reserve to keep interest rates elevated to control inflation pressures.

Why did the USD strengthen after the PPI report?

Markets expect higher interest rates to support the USD because investors seek stronger returns from dollar-denominated assets.

Does higher PPI mean inflation will continue rising?

Not always, but sustained increases in PPI often place upward pressure on future consumer inflation over time.