Introduction

Economic report analysis for the week ahead highlights a critical period for global markets as Central Banks, Chinese Retail Sales data, the BoC policy decision, and the FOMC meeting dominate the macroeconomic calendar. Investors are entering a pivotal week where monetary policy signals, geopolitical tensions, and global growth indicators will likely shape expectations for the remainder of 2026.

This Economic report outlines the key economic developments scheduled across major economies including the United States, China, Europe, Japan, Canada, and Australia. The focus will be on major policy announcements from several Central Banks, particularly the FOMC in the United States and the BoC in Canada, while fresh data on Chinese Retail Sales and industrial activity will provide a crucial read on the strength of China’s post-pandemic recovery.

At the same time, geopolitical tensions and energy market volatility continue to influence inflation expectations globally. Rising oil prices tied to Middle East conflict and shipping disruptions are complicating the outlook for monetary policy across multiple jurisdictions. This Economic report therefore examines not only the data releases themselves but also the broader implications for inflation, growth and financial markets.

The coming week is unusually dense with major policy decisions from global Central Banks, including the FOMC, BoC, BoJ, BoE, ECB, RBA, and SNB. The decisions and guidance from these institutions will provide investors with an updated roadmap for interest rate trajectories as policymakers balance inflation risks against weakening economic momentum.

In this comprehensive Economic report, we examine the major themes shaping global markets: the US-China economic relationship, technology sector developments, Chinese domestic demand trends, and the monetary policy outlook from key Central Banks.

Global Macro Overview

The central theme of this Economic report is the convergence of several major macroeconomic catalysts within the same week. Rarely do so many influential Central Banks deliver policy updates simultaneously, and the alignment of these events increases the probability of heightened market volatility.

The global economy in 2026 remains characterized by several overlapping forces:

- Elevated but moderating inflation

- Tight monetary conditions

- Slowing global growth

- Geopolitical instability

- Energy market volatility

- Structural changes in trade and supply chains

Against this backdrop, Central Banks must carefully balance their inflation mandates with the growing risk of economic slowdown.

The FOMC decision will likely attract the most attention given the influence of US monetary policy on global financial conditions. Meanwhile, the BoC meeting will provide insights into how North American policymakers are navigating labour market weakness and inflation pressures simultaneously.

The Economic report also highlights China’s economic trajectory through upcoming Chinese Retail Sales data, which serves as one of the most important indicators of consumer demand in the world’s second-largest economy.

US-China Meeting: Economic and Trade Implications

One of the most important geopolitical developments covered in this Economic report is the upcoming meeting between senior officials from the United States and China.

The meeting in Paris between representatives from both countries is designed to prepare for a planned state visit by the US President to Beijing later this month. This diplomatic engagement comes at a time when trade tensions remain elevated despite a temporary tariff truce.

Discussions are expected to focus on several key areas:

- The future of tariff arrangements

- Supply chain stability

- Technology trade restrictions

- Agricultural imports

- Rare earth mineral exports

From a global macro perspective, the outcome of these discussions could significantly influence trade flows and investor sentiment. The Economic report notes that both sides appear motivated to avoid renewed escalation, particularly given the fragile state of global growth.

Any progress toward trade stability would be welcomed by financial markets, particularly in sectors such as semiconductors, agriculture, and aerospace.

Nvidia GTC Conference and Technology Sector Outlook

Another major highlight discussed in this Economic report is Nvidia’s annual GTC conference, which continues to shape expectations for the global artificial intelligence industry.

Technology investors are watching closely for updates regarding:

- AI hardware supply chains

- Semiconductor production capacity

- Data-center expansion

- AI software ecosystems

The company’s roadmap for future chips and computing platforms may provide insight into the next stage of AI development and its economic impact.

In many ways, technological innovation has become a key driver of productivity growth globally. As such, developments in the semiconductor and AI industries increasingly influence macroeconomic expectations.

For global Central Banks, the productivity impact of artificial intelligence could play a role in shaping long-term inflation dynamics and economic growth projections.

Chinese Retail Sales and Economic Activity

The Economic report places significant emphasis on China’s upcoming economic data releases, particularly Chinese Retail Sales.

Chinese Retail Sales serve as one of the most important indicators of consumer spending within the Chinese economy. Consumer demand in China has been uneven in recent years as households remain cautious following the property market downturn and broader economic uncertainty.

Economists expect Chinese Retail Sales growth to rebound modestly in the upcoming report, supported by government stimulus measures including consumer trade-in subsidies and incentives designed to boost domestic consumption.

However, underlying consumer sentiment remains fragile. Weak property prices and high youth unemployment continue to weigh on spending patterns across many sectors.

This Economic report highlights that policymakers in Beijing have prioritized consumption growth as a central pillar of their economic strategy. Strengthening domestic demand is seen as essential to offset slowing export growth and ongoing geopolitical tensions affecting trade.

The performance of Chinese Retail Sales will therefore provide a crucial signal regarding the sustainability of China’s economic recovery.

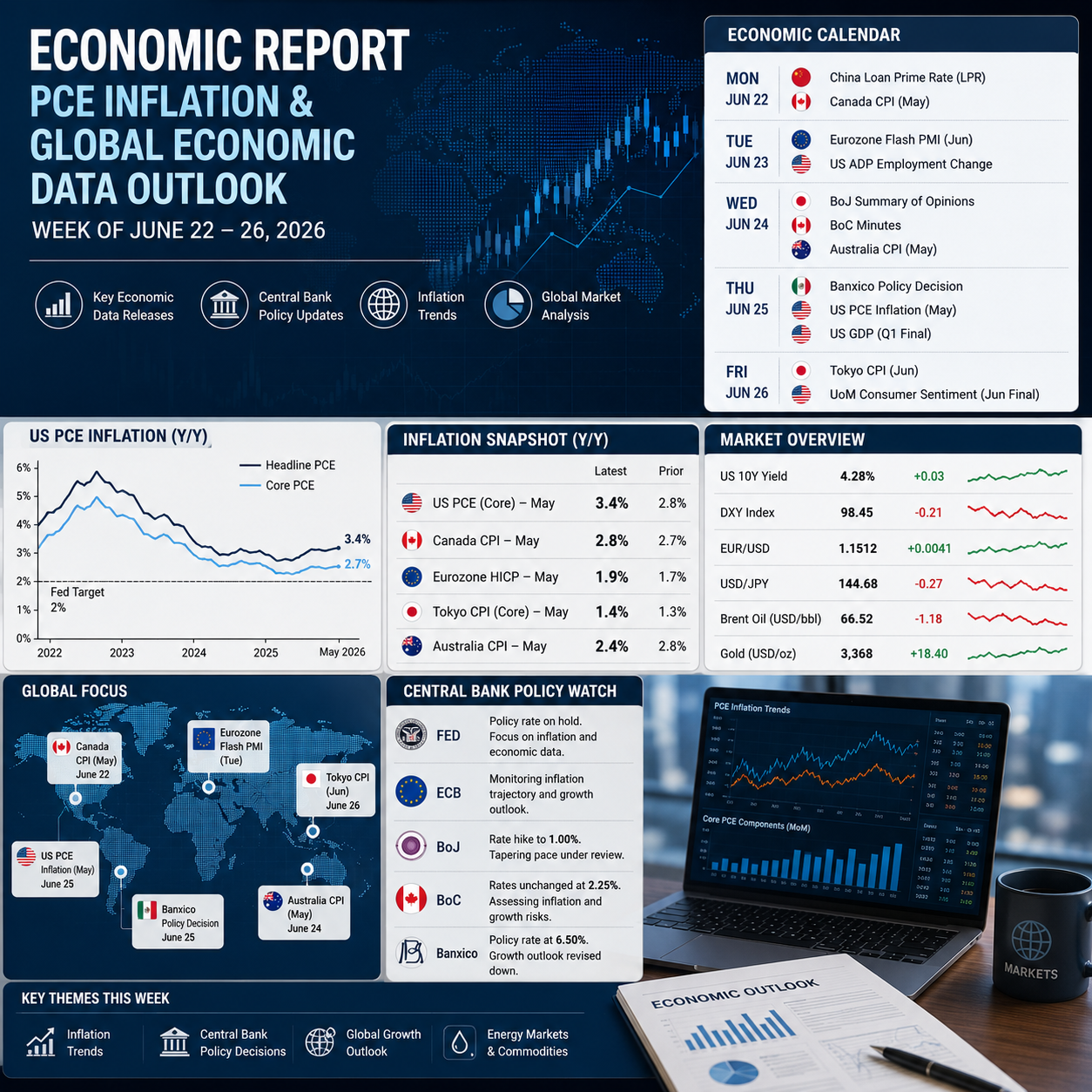

Canadian Inflation and the BoC Outlook

Turning to North America, the Economic report examines Canada’s upcoming inflation data and its implications for the BoC.

The BoC has maintained its policy rate at 2.25% as it attempts to balance inflation control with the need to support economic growth. Canada’s labour market recently showed signs of weakness, with a sharp decline in employment and a rising unemployment rate.

Despite the softer labour market, inflation remains slightly above the central bank’s target. Food and housing costs continue to exert pressure on household budgets.

The Economic report suggests that the BoC will likely adopt a cautious stance in its upcoming meeting. Policymakers are expected to monitor economic conditions closely before making any further policy adjustments.

Financial markets currently anticipate the first potential rate hike from the BoC later in the year if inflation pressures persist.

FOMC Policy Decision and US Monetary Outlook

No Economic report covering global markets would be complete without a detailed analysis of the upcoming FOMC meeting.

The FOMC is widely expected to leave interest rates unchanged at its upcoming meeting. However, investors will focus intensely on the central bank’s economic projections and policy guidance.

The Federal Reserve continues to face a delicate balancing act. Inflation remains above the official 2% target, while the labour market shows signs of cooling.

Recent inflation data has indicated that price pressures remain sticky, particularly within services sectors. At the same time, rising energy prices linked to geopolitical tensions may complicate the inflation outlook further.

The Economic report highlights that the FOMC will likely emphasize patience and data dependency in its policy communication.

Markets are currently pricing in limited rate cuts this year, reflecting concerns that inflation could remain elevated for longer than previously expected.

Central Banks Across the Globe

Beyond the FOMC and BoC, several other Central Banks are scheduled to announce policy decisions during the same week.

These include:

- Bank of Japan

- Bank of England

- European Central Bank

- Swiss National Bank

- Reserve Bank of Australia

- Riksbank

The clustering of policy decisions from so many Central Banks makes this one of the most important weeks of the year for macroeconomic analysis.

Each institution faces its own unique set of economic conditions. Some economies are grappling with inflation pressures, while others face stagnating growth or currency volatility.

The Economic report underscores that policy divergence among Central Banks could become a defining feature of the global economy over the next several years.

Japan’s Shunto Wage Negotiations

Another important development covered in this Economic report is Japan’s annual Shunto wage negotiations.

These negotiations play a crucial role in determining wage growth across the Japanese economy. Strong wage increases could reinforce the Bank of Japan’s efforts to achieve sustained inflation near its target.

Japanese unions are seeking significant pay increases this year as workers attempt to keep pace with rising living costs.

The outcome of the Shunto negotiations will therefore influence the future path of Japanese monetary policy.

Europe’s Monetary Policy Landscape

European Central Banks also face a challenging policy environment.

Energy prices have surged due to geopolitical tensions, increasing inflation risks across the region. At the same time, economic growth in several European countries remains weak.

The European Central Bank is expected to keep interest rates unchanged for now. However, policymakers have emphasized their readiness to respond if inflation expectations rise.

This Economic report highlights that Europe’s policy outlook remains highly dependent on energy markets and geopolitical developments.

Geopolitical Risks and Energy Markets

Geopolitical developments remain a central theme in this Economic report.

The conflict in the Middle East has significantly disrupted global energy markets, pushing oil prices above key thresholds.

Higher energy costs have several macroeconomic consequences:

- Increased inflation pressures

- Higher transportation costs

- Slower economic growth

- Tighter financial conditions

Central Banks must consider these factors when setting interest rate policy.

Energy-driven inflation shocks are particularly challenging because monetary policy has limited ability to address supply-side price increases.

Global Market Implications

The developments outlined in this Economic report will likely influence multiple asset classes.

Equity markets will respond to technology sector developments and central bank guidance.

Bond markets will focus on inflation expectations and interest rate projections from the FOMC and other Central Banks.

Currency markets will react to policy divergence among major economies.

Commodity markets will remain sensitive to geopolitical risks and supply disruptions.

Investors therefore face a complex environment where macroeconomic data, geopolitical developments, and central bank policy all interact simultaneously.

Conclusion

This Economic report highlights one of the most important weeks of the year for global macroeconomic developments.

Key themes include:

- Policy decisions from multiple Central Banks

- The highly anticipated FOMC meeting

- Canada’s BoC policy outlook

- Critical Chinese Retail Sales data

- Geopolitical risks affecting energy markets

Together, these developments will shape expectations for inflation, interest rates, and economic growth for the remainder of 2026.

For investors and policymakers alike, the coming week represents a critical moment for assessing the direction of the global economy.