Economic report week begins with heightened expectations as global markets approach a pivotal recalibration phase. This economic report cycle arrives at a critical moment when investors, policymakers, and corporations are reassessing inflation persistence, growth durability, and central bank policy trajectories. From OPEC+ production decisions to fresh PMIs data and the latest US Manufacturing signals, this economic report series could reshape risk sentiment heading into the second quarter.

The coming days deliver one of the most concentrated stretches of macroeconomic catalysts so far this year. Energy markets await direction from OPEC+, bond traders prepare for volatility around Nonfarm Payrolls, and equity markets monitor whether US Manufacturing can sustain its recent rebound. Together, these developments transform this economic report calendar into more than a routine update — it becomes a turning point for pricing growth, inflation, and monetary policy expectations.

The Structure of This Economic Report Week

This economic report cycle unfolds in layered fashion:

- OPEC+ ministerial meeting

- Global and US PMIs data

- US Manufacturing ISM survey

- Eurozone inflation readings

- ECB policy minutes

- UK fiscal update

- Australian GDP

- Chinese PMIs

- US Nonfarm Payrolls

- US Retail Sales

Each economic report carries standalone importance, but the collective narrative will determine whether the global economy continues its soft-landing trajectory or moves toward renewed tightening fears.

OPEC+ Decision: Energy Markets at a Crossroads

No economic report this week carries as much geopolitical sensitivity as the OPEC+ production decision.

OPEC+ has maintained voluntary supply cuts totaling 2.2 million barrels per day. Now, reports suggest a gradual easing of those cuts could begin. Markets anticipate a possible phased increase beginning next month.

This economic report event matters for three reasons:

1. Inflation Expectations

Oil prices directly influence headline inflation metrics. If OPEC+ increases production aggressively, crude could soften, easing inflation pressure. Conversely, restrained output could keep Brent elevated above $75, reinforcing sticky inflation fears.

2. Monetary Policy Implications

Central banks remain highly sensitive to energy-driven inflation spikes. A supply increase that lowers oil prices may provide breathing room for rate cuts. A tighter stance from OPEC+ could delay policy easing.

3. Market Volatility

Energy equities, emerging markets, and inflation-linked bonds will react quickly to this economic report outcome.

The geopolitical backdrop adds complexity. Tensions in the Middle East and risks to the Strait of Hormuz elevate supply uncertainty. Even a modest OPEC+ output increase could be overshadowed by disruption fears.

In summary, this economic report event has implications far beyond oil markets — it feeds directly into global inflation narratives.

PMIs: Forward-Looking Economic Signals

Purchasing Managers’ Index surveys (PMIs) provide early insight into business activity. This economic report batch includes global final readings alongside US ISM releases.

US Manufacturing PMI

Recent data showed US Manufacturing returning to expansion territory above 50. However, momentum remains fragile. New orders surged last month, but employment components softened.

This economic report reading must confirm whether:

- New orders remain strong

- Production expands further

- Employment stabilizes

- Input costs moderate

A second consecutive expansionary US Manufacturing reading would strengthen cyclical recovery narratives.

Services PMI

The services sector remains the backbone of the US economy. This economic report reading carries inflation sensitivity because services inflation tends to be stickier than goods inflation.

Markets will focus on:

- Business activity trends

- Price pressures

- Wage-related cost components

- Employment signals

If services PMIs show rising prices again, expectations for near-term rate cuts may fade.

US Manufacturing: The Industrial Pulse

US Manufacturing stands at the center of this economic report narrative.

After months of contraction, signs of stabilization emerged. Inventory adjustments, easing supply chains, and modest demand improvements have supported recovery.

However, several risks remain:

- High interest rates

- Slowing global demand

- Strong US dollar pressure

- Labor cost pressures

This economic report reading will either validate a cyclical rebound or expose fragility beneath the surface.

If US Manufacturing strengthens further, equity market leadership could broaden beyond mega-cap technology into industrial and materials sectors.

If it falters, defensive positioning may resume.

Nonfarm Payrolls: Labor Market Reality Check

The Nonfarm Payrolls economic report is the headline risk event.

Consensus expectations point to moderate job growth around 80,000 to 100,000.

Key components:

- Headline job creation

- Unemployment rate

- Labor force participation

- Average hourly earnings

Wage growth remains critical. The Federal Reserve’s inflation battle hinges on wage moderation.

A strong economic report showing accelerating wages could reignite tightening fears. A cooling print would reinforce soft landing optimism.

Bond markets are already pricing some labor moderation. Surprise strength could trigger yield spikes.

Retail Sales: The Consumer Engine

This economic report also delivers delayed Retail Sales data.

The American consumer has displayed resilience despite elevated rates. However, cracks are emerging:

- Rising credit card balances

- Slowing real income growth

- Increased reliance on savings

This economic report reading tests whether consumption momentum remains intact.

Strong retail activity would support GDP projections. Weakness could shift expectations toward slower growth in coming quarters.

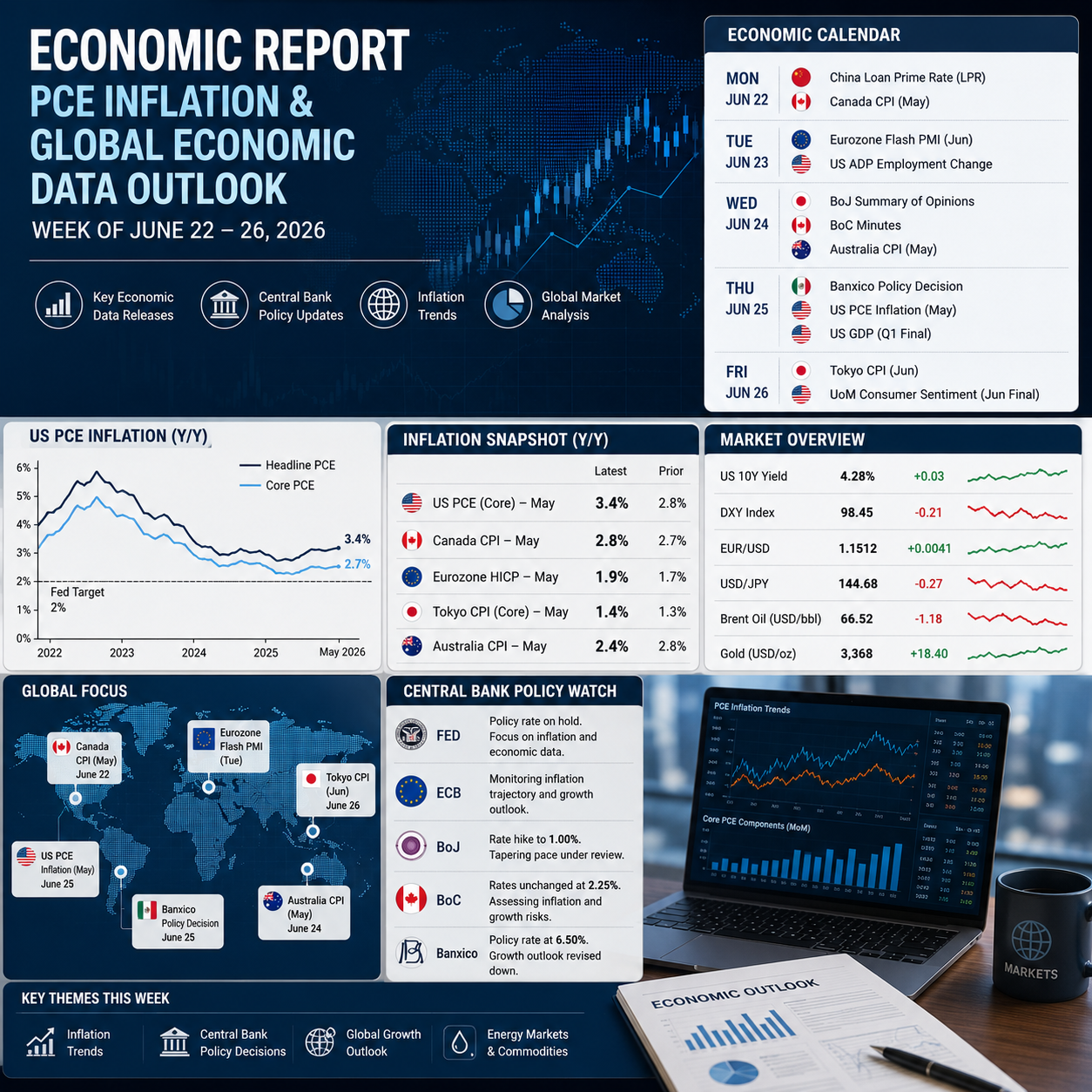

Eurozone Inflation and ECB Minutes

Europe’s contribution to this economic report week includes:

- Flash HICP inflation

- ECB policy minutes

Inflation has trended downward, nearing target. However, wage growth remains elevated.

Markets will assess whether the ECB signals patience or prepares for easing.

This economic report matters for global bond yields and currency markets, particularly EUR/USD volatility.

UK Spring Statement

The UK government’s fiscal update aims for stability rather than surprise.

Debt sustainability and gilt issuance levels are focal points.

Though unlikely to shock markets, this economic report shapes long-term fiscal credibility.

Australia GDP and China PMIs

Australian GDP is expected to show solid momentum. However, strong growth could delay rate cuts from the RBA.

Chinese PMIs remain fragile. Domestic demand weakness persists despite policy stimulus.

Together, these Asia-Pacific economic report releases provide insight into global trade demand and commodity trends.

Market Implications: What Could Shift?

This economic report sequence may influence:

1. Interest Rate Expectations

Bond yields react to inflation and labor data.

2. Equity Sector Rotation

Industrials and cyclicals benefit from strong US Manufacturing.

3. Energy Prices

OPEC+ drives crude volatility.

4. Currency Markets

USD strength hinges on labor resilience.

5. Risk Appetite

Soft landing narrative vs slowdown risk.

Federal Reserve Focus

The Fed’s messaging emphasizes inflation persistence over growth fears.

This economic report set must confirm:

- Labor moderation

- Services inflation cooling

- Manufacturing stabilization

Only then could policymakers feel confident easing later in the year.

Soft Landing vs Reacceleration

Two scenarios emerge from this economic report cycle:

Scenario 1: Soft Landing Reinforced

- Moderate payroll growth

- Cooling wages

- Stable US Manufacturing

- Oil prices contained

Scenario 2: Reacceleration Risk

- Strong payroll surprise

- Rising services prices

- OPEC+ keeps supply tight

- Oil spikes

Markets are finely balanced between these outcomes.

Investor Positioning Ahead of Data

Caution dominates positioning. Volatility hedges remain elevated. Bond traders prepare for yield swings.

This economic report concentration compresses multiple catalysts into one week, amplifying cross-asset reactions.

Final Outlook: A Defining Economic Report Week

This economic report preview highlights a synchronized moment of recalibration. OPEC+ decisions, PMIs momentum, US Manufacturing resilience, and Nonfarm Payrolls stability converge to test prevailing narratives.

The broader question is whether growth can remain resilient without reigniting inflation.

The answer begins with this economic report sequence.

Markets will respond not just to individual numbers, but to the cumulative signal.

If data align toward balance, confidence strengthens.

If cracks widen, volatility returns.

Either way, this economic report week represents a strategic inflection point for 2026’s macro outlook.