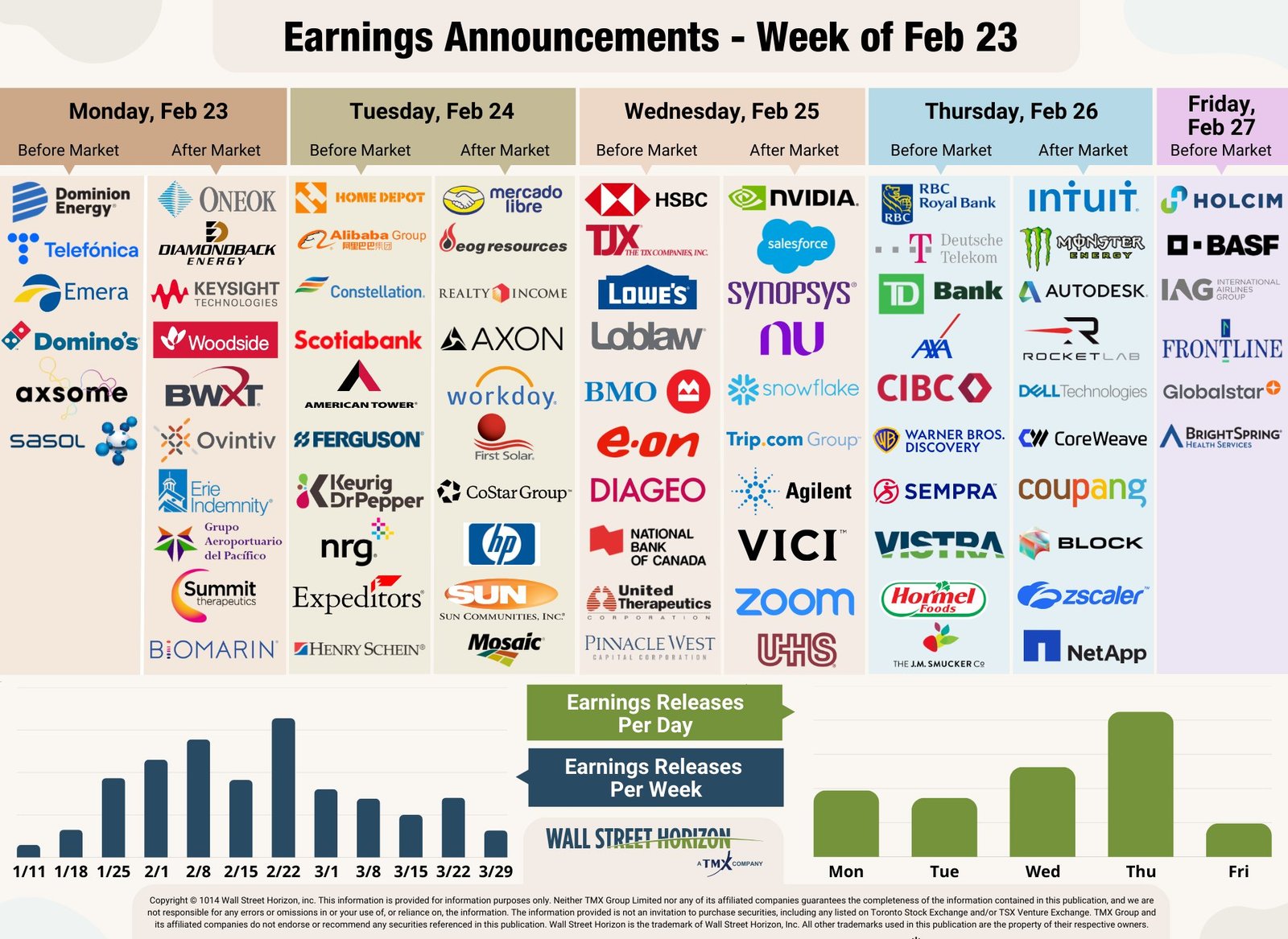

The macro outlook demands attention—but this one demands preparation.

Grab a coffee. Clear your schedule. Forget whatever else you had penciled in for the first full week of February. What lies ahead is not a routine cadence of economic releases or predictable policy commentary. It is a compressed, high-stakes convergence of monetary decisions, global data, and geopolitical undercurrents—a seven-day stretch capable of reshaping portfolios, redefining risk appetite, and exposing whether market expectations are aligned with economic reality.

This is the Macro Gauntlet.

Over the course of a single week, markets will be forced to absorb a dense barrage of signals: central bank decisions across multiple continents, critical economic data from the United States, and policy guidance that will influence interest rates, currencies, and capital flows well beyond the near term. While asset prices often react to headlines, this week is about conditions—the underlying economic and policy framework that determines what markets can sustain.

This macro moment is not about isolated data points. It is about confirmation. Confirmation that inflation pressures are easing—or persisting. Confirmation that labor markets are cooling without breaking. Confirmation that policymakers can maintain control without tightening financial conditions too far.

By the end of the week, markets will have far greater clarity on where economic momentum is building, where it is stalling, and where risks are quietly accumulating.

The Macro Backdrop — Setting the Conditions for Global Markets

Before investors react, policymakers act.

In the days ahead, the world’s most influential financial institutions will shape the environment in which global markets must operate. Monetary policy decisions, energy supply signals, and high-impact economic data releases will quietly—but decisively—define expectations for growth, inflation, and risk.

These forces do not move markets in isolation. They interact, compound, and sometimes collide. Understanding this backdrop is essential, because it determines how every subsequent data point is interpreted.

OPEC+ and Energy Stability (Sunday)

The week begins with energy markets, where expectations are deliberately restrained. OPEC+ is widely expected to maintain current production levels, choosing stability over stimulus. Brent crude’s recent recovery above the $70 level reflects supply-side disruptions and geopolitical uncertainty more than a resurgence in global demand.

This matters more than it first appears.

Stable energy prices imply:

- Contained input costs across transportation, manufacturing, and consumer sectors

- Limited near-term upside for energy producers

- Reduced inflationary pressure feeding into central bank decision-making

What markets will watch closely is not action, but language. Any indication that OPEC+ views geopolitical supply risks as persistent rather than temporary could reintroduce volatility into inflation expectations, complicating the macro narrative just as policymakers attempt to maintain balance.

Central Banks Take the Stage

Reserve Bank of Australia (Tuesday)

Among all macro events this week, the Reserve Bank of Australia represents the highest probability of meaningful action. With labor markets tightening again and core inflation proving stubborn, the RBA stands on the brink of its first rate hike in over two years.

A move toward 3.85% would reinforce a critical message: the global policy cycle is not synchronized.

While markets have grown comfortable with the idea that tightening is largely finished, Australia’s situation serves as a reminder that inflation dynamics remain uneven. For earnings season, this underscores a broader truth—companies operating across regions face divergent monetary realities, complicating forecasting and capital allocation.

Bank of England (Thursday)

The Bank of England remains trapped in one of the most uncomfortable macro positions among developed economies. Inflation remains the highest in the G7, while economic momentum continues to erode.

A policy hold is fully priced in, but investors will focus on:

- The vote split within the Monetary Policy Committee

- Changes in inflation forecasts

- Any acknowledgment that inflation expectations risk becoming entrenched

For earnings season, this has direct implications for UK-exposed consumer, retail, and financial companies. A hawkish tone would further pressure margins and spending power, while a more cautious stance could provide temporary relief—though not clarity.

European Central Bank (Thursday)

The ECB enters the week projecting calm. Policy, according to President Lagarde, is “in a good place.” Yet beneath that calm lies a significant challenge: currency strength.

The euro’s appreciation acts as a form of de facto tightening, compressing export competitiveness and earnings translation for multinational firms. During earnings season, even subtle commentary on currency dynamics can influence how investors interpret guidance from European-exposed companies.

Banxico and the RBI (Thursday/Friday)

Mexico and India offer a counterpoint. Both central banks remain in holding patterns, albeit for different reasons. Banxico faces fiscal uncertainty, while the RBI enjoys a rare alignment of growth and controlled inflation.

Their relative stability highlights the fragmentation of global monetary policy—another layer of complexity for multinational earnings season analysis.

The Economic Data Deluge

US ISM Manufacturing and Services (Monday/Wednesday)

Purchasing managers’ data often acts as an early warning system. Recent flash PMIs suggested expansion, but with troubling softness in new orders, particularly exports.

The official ISM reports will either confirm or challenge that signal. A weak services print would be especially concerning, as it would suggest the consumer-driven engine of the US economy is losing momentum—an ominous backdrop for earnings season.

US Treasury Quarterly Refunding (Wednesday)

Rarely a headline event, the Treasury’s refunding announcement carries outsized importance in this environment. Expectations are for unchanged coupon sizes, funded primarily through Treasury bills.

Any surprise increase in long-duration supply would:

- Push yields higher

- Reprice equity discount rates

- Pressure high-valuation growth stocks reporting this earnings season

US and Canada Jobs Reports (Friday)

Labor data closes the week. Markets are looking for continued moderation—steady job growth without wage acceleration.

A benign report would support the soft-landing narrative. A surprise in either direction would force a rapid reassessment of rate expectations, directly influencing how investors digest earnings guidance.