Earnings Outlook takes center stage during the final week of January 2026, as global markets confront one of the most consequential convergence points of the year. From January 26 to January 30, central banks, macroeconomic data, and corporate earnings reports collide in a compressed period that will redefine expectations for growth, valuations, and risk assets well into the first quarter.

This is not simply another earnings week. It is a systemic stress test. Five major central banks will deliver policy decisions or critical signals. Key inflation and GDP figures will recalibrate growth assumptions. Simultaneously, some of the most influential companies on the planet—Apple, Microsoft, Meta, Tesla, and others—will report earnings that directly influence indices, capital flows, and investor confidence.

The earnings outlook emerging from this week will shape how markets price risk, growth, and liquidity in 2026.

Earnings Outlook: What Investors Are Watching

- Central banks reinforcing higher-for-longer policy

- Big Tech earnings setting valuation direction

- AI investment returns under scrutiny

- Global growth slowing but margins stabilizing

Part I: Central Banks and the Earnings Outlook Equation

Central banks are no longer reacting to inflation emergencies. Instead, they are managing credibility, timing, and financial stability. Their decisions directly affect borrowing costs, valuation multiples, and ultimately corporate earnings growth.

The Federal Reserve: Earnings Outlook Under “Higher for Longer”

The Federal Reserve enters its January meeting with markets reluctantly accepting reality: rate cuts are not imminent.

Strong labor markets, persistent services inflation, and resilient consumer demand continue to support a restrictive stance. For the earnings outlook, this environment creates a fundamental challenge—companies must deliver profit growth without monetary tailwinds.

Chair Jerome Powell’s expected messaging reinforces three themes critical to earnings:

- Discount rates remain elevated, pressuring long-duration earnings expectations

- Wage growth and input costs remain a margin risk

- Capital spending discipline becomes essential for earnings sustainability

For equity markets, this reinforces a bifurcated earnings outlook: companies with pricing power and balance-sheet strength outperform, while leveraged or cyclical firms struggle.

Bank of Canada: Earnings Outlook and Consumer Fragility

Canada’s earnings outlook hinges on household resilience. Elevated debt levels, soft housing activity, and slowing consumption challenge corporate revenue growth.

The Bank of Canada’s alignment with the Federal Reserve limits policy flexibility, reinforcing a subdued earnings outlook for consumer-facing sectors. However, stable core inflation offers a modest cushion for businesses managing cost structures effectively.

Riksbank: Currency Risk and Earnings Sensitivity

Sweden’s Riksbank faces a delicate balancing act. A weak Krona supports exporters’ earnings outlook but risks importing inflation that erodes domestic margins.

For European corporates, currency volatility adds complexity to earnings guidance, forcing executives to hedge aggressively while managing cost inflation.

Brazil’s Central Bank: A Turning Point for Earnings Growth

Brazil stands out as a rare bright spot in the global earnings outlook. Rapid disinflation, a strong currency, and the potential for future easing create conditions for margin expansion.

Emerging-market earnings outlooks often hinge on inflation control. Brazil’s progress positions it as a potential earnings leader among developing economies in 2026.

Bank of Japan: Inflation Signals and Global Earnings Impact

Tokyo CPI data serves as a proxy for global liquidity conditions. A stronger yen compresses exporter earnings but tightens global financial conditions. A weaker yen boosts Japanese earnings while exporting disinflation globally.

Either outcome influences multinational earnings outlooks through currency translation and trade competitiveness.

Part II: Macro Data and the Global Earnings Outlook

Economic data this week offers confirmation—or contradiction—of earnings expectations.

Eurozone GDP: Anemic Growth, Constrained Earnings

Weak growth across Europe caps revenue expansion for multinational firms. While recession fears ease slightly, the earnings outlook remains defensive, favoring cost control over growth initiatives.

Australia CPI: Inflation and Earnings Risk

Persistent services inflation threatens margins for Australian firms. Any upside inflation surprise would harden rate expectations and pressure earnings multiples.

China Industrial Profits: Structural Earnings Headwinds

China’s earnings outlook remains bifurcated. High-tech and advanced manufacturing show resilience, while traditional industries face profit compression and deflationary pressure.

This imbalance weighs on global earnings through supply chains, pricing power, and export competition.

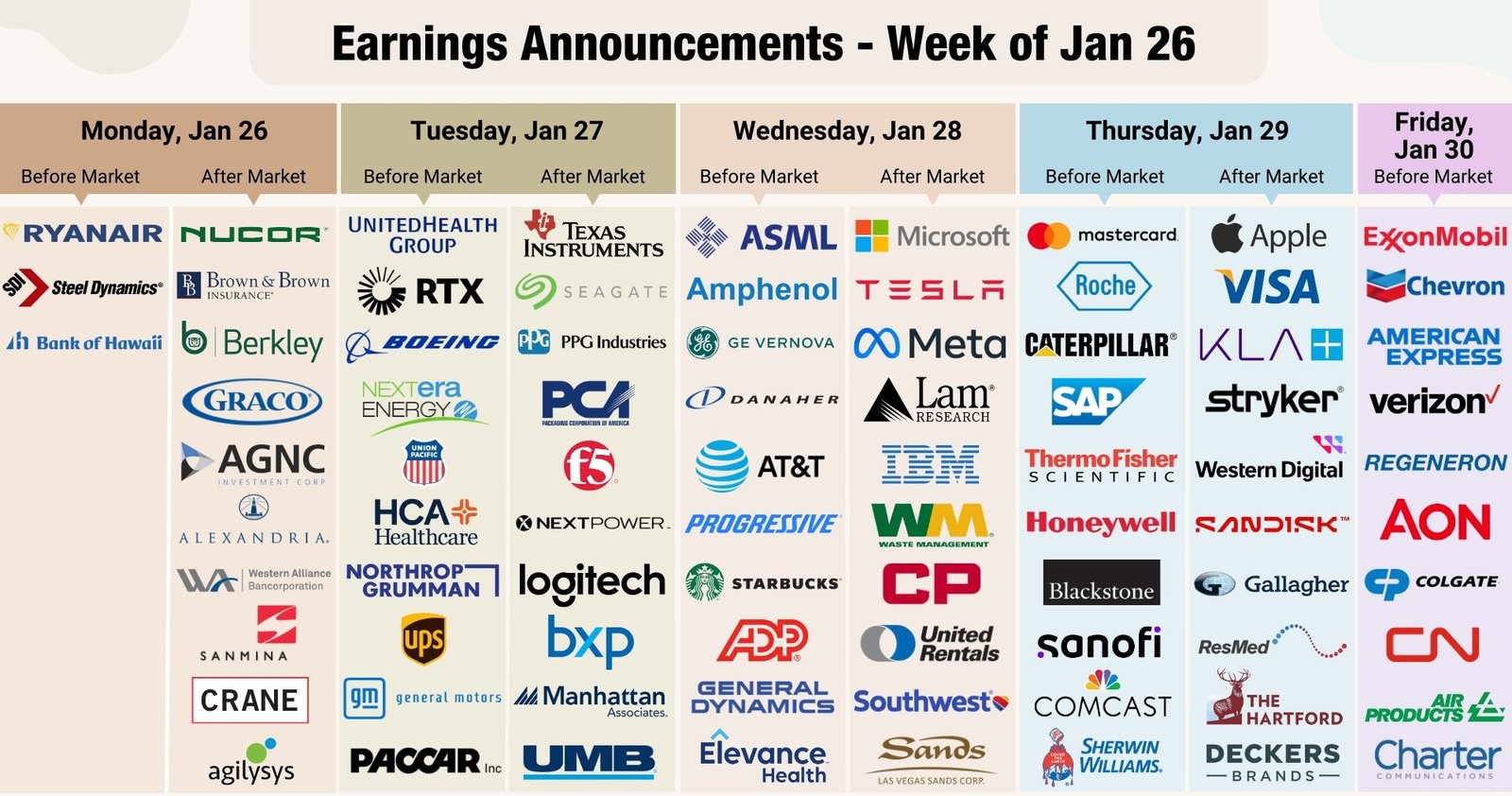

Part III: Big Tech Earnings and the Market’s Verdict

Big Tech earnings dominate the earnings outlook narrative. These companies represent a disproportionate share of index earnings growth and valuation support.

Microsoft: The Enterprise Earnings Bellwether

Microsoft’s earnings outlook hinges on:

- Cloud growth sustainability

- AI monetization progress

- Corporate IT spending discipline

Azure growth rates will directly influence confidence in enterprise earnings resilience.

Meta Platforms: Advertising and Earnings Momentum

Meta reflects the health of digital advertising and discretionary corporate spending. Strong earnings reinforce risk appetite, while guidance caution reverberates across growth stocks.

Apple: Consumer Earnings Under Scrutiny

Apple’s earnings outlook tests premium consumer demand, especially in China. Services revenue remains the stabilizing force as hardware cycles mature.

Tesla: Earnings Volatility and Narrative Risk

Tesla’s earnings outlook remains the most volatile. Margins, demand elasticity, and forward-looking commentary drive sharp market reactions.

Semiconductors, Industrials, and Financials

- Lam Research gauges AI-driven capital expenditure

- Boeing reflects industrial recovery and execution risk

- UnitedHealth signals healthcare cost inflation

- SoFi highlights consumer credit and fintech earnings risk

Part IV: The Earnings Outlook Synthesis

This week crystallizes three intersecting forces shaping the earnings outlook:

1. Elevated Rates vs Earnings Multiples

Higher discount rates challenge valuation assumptions, demanding real earnings growth—not narratives.

2. Guidance Credibility

Forward guidance matters more than backward-looking results. Markets reward clarity and punish uncertainty.

3. Global Disinflation vs Demand Weakness

Lower inflation supports margins but signals soft demand, complicating earnings visibility.

Conclusion: Earnings Outlook at a Crossroads

The final week of January 2026 defines the earnings outlook for the quarter ahead. Central banks reinforce patience. Macro data confirms slow growth. Corporate earnings reveal which businesses can thrive without monetary support.

This is a week where earnings quality, not speculation, determines market leadership.

The earnings outlook will not emerge unchallenged—but it will emerge clarified.