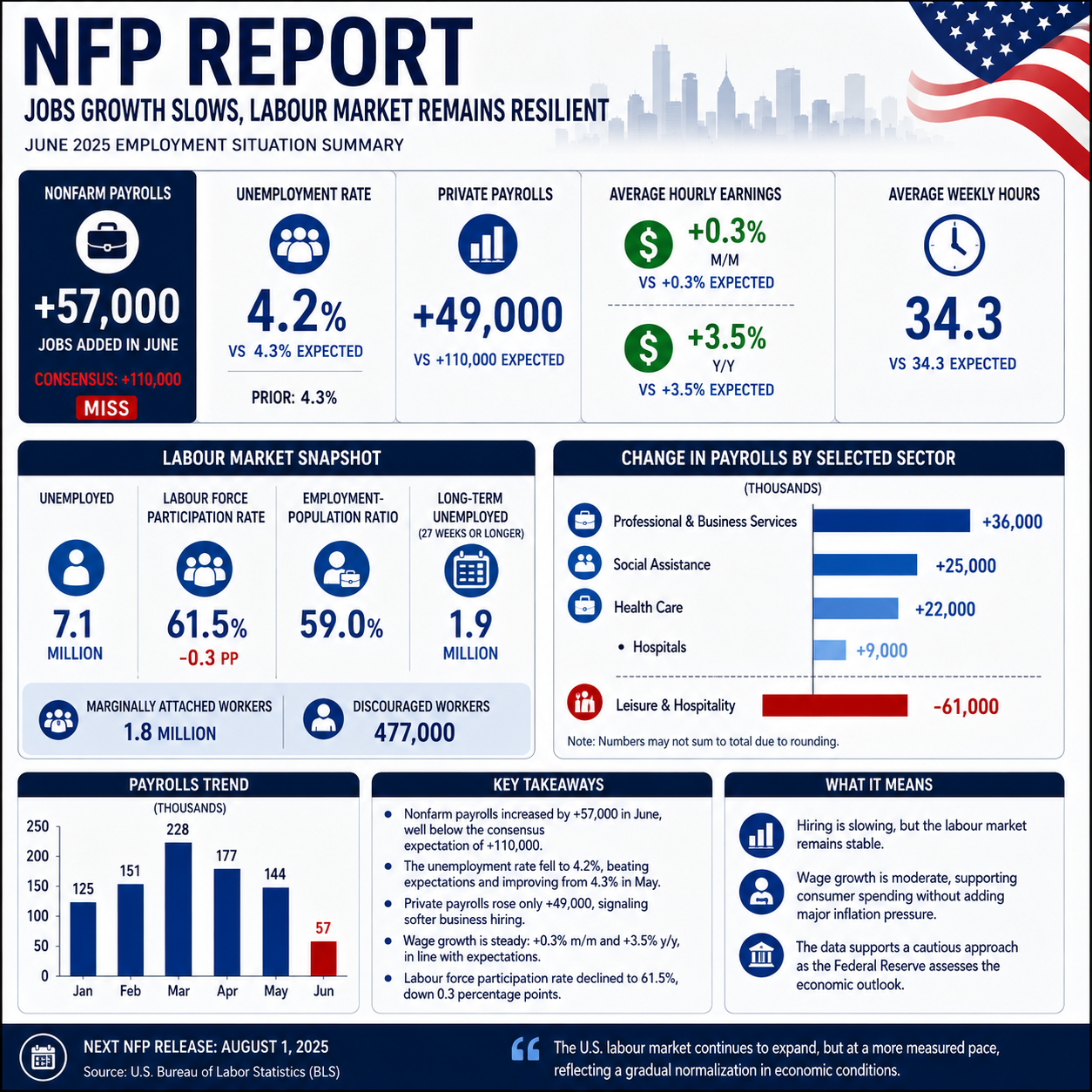

US Jobs Report data for January delivered one of the most complex and market-moving employment releases in recent years. What initially appeared to be a clean NFP beat quickly turned into a layered debate about Growth, policy direction, and credibility after a massive benchmark revision altered the broader labor market narrative.

At the surface level, payroll gains exceeded expectations, the Unemployment Rate declined, and wage Growth remained firm. However, beneath those headline numbers, the Bureau of Labor Statistics introduced a historic downward revision to prior employment estimates, raising serious questions about how strong the economy has truly been over the past year.

Markets reacted instantly. Treasury yields spiked. The dollar surged. Then both reversed. The resulting US Dollar Market Reaction revealed one clear truth: investors are no longer willing to accept headline strength without scrutiny.

This deep-dive analysis breaks down the NFP surprise, labor force dynamics, wage trends, sector-level Growth, Federal Reserve implications, bond repricing, and the broader currency impact shaping 2025 expectations.

January NFP: A Stronger-Than-Expected Payroll Print

The January employment figures showed:

- NFP: +130,000 vs +70,000 expected

- Private payrolls: +172,000

- Manufacturing: +5,000 vs -5,000 expected

- Unemployment Rate: 4.3% vs 4.4% prior

- Average Hourly Earnings (MoM): +0.4%

- Average Hourly Earnings (YoY): 3.7%

- Labor force participation: 62.5%

From a purely statistical standpoint, this was a broad-based beat. Economists had anticipated cooling Growth as higher interest rates filtered deeper into the economy. Instead, hiring proved resilient.

The NFP gain of 130,000 may not seem explosive relative to post-pandemic peaks, but in an environment of restrictive monetary policy, it signals meaningful underlying momentum.

Importantly, the Unemployment Rate fell even as labor force participation rose — a rare combination that strengthens the case for authentic labor market resilience.

The Unemployment Rate: A Key Policy Signal

The decline in the Unemployment Rate from 4.4% to 4.3% carries more weight than the headline suggests.

When participation rises and unemployment falls simultaneously, it indicates that new entrants are being absorbed without displacing existing workers. This dynamic is critical for evaluating sustainable Growth.

For the Federal Reserve, labor slack remains a central variable in inflation control. A falling Unemployment Rate suggests:

- Demand for labor remains elevated

- Wage pressures may persist

- Rate cuts may not be imminent

Even more telling was the unrounded unemployment reading, which fell decisively rather than narrowly. That precision matters in policy discussions.

The Benchmark Revision: -858,000 Jobs Erased

While the January payroll data surprised to the upside, the benchmark revision stunned analysts.

The BLS revised employment levels down by 858,000 jobs over the previous year. This adjustment aligns survey data with tax records from the Quarterly Census of Employment and Wages.

Such a significant downward revision implies that job creation was overstated for months.

This creates two competing interpretations:

1. The Present Is Strong

January Growth reflects renewed acceleration.

2. The Past Was Weaker

The labor market had already been slowing, and monetary tightening was more effective than realized.

This tension between current strength and historical weakness drove volatility in equities, bonds, and foreign exchange markets.

Why the US Dollar Market Reaction Was So Volatile

The immediate US Dollar Market Reaction followed textbook logic:

Strong payrolls → Higher yields → Delayed rate cuts → Stronger dollar

However, within 30 minutes, the rally faded.

Why?

- Traders reassessed the revision magnitude.

- Models adjusted for potential overstatement risk.

- Profit-taking emerged after a pre-report dollar run.

- Contradictory data from ISM and ADP tempered conviction.

The dollar’s inability to hold highs signaled uncertainty rather than confidence.

Sector Breakdown: Where Growth Is Concentrated

The composition of hiring tells a deeper story about structural versus cyclical momentum.

Healthcare (+82,000)

Healthcare remains the most consistent engine of payroll Growth, driven by demographics and policy spending.

Construction (+33,000)

Despite elevated mortgage rates, non-residential projects continue benefiting from federal investment programs.

Social Assistance (+42,000)

Childcare and eldercare hiring reflects normalization after pandemic distortions.

Financial Activities (-22,000)

A rate-sensitive sector showing strain under high borrowing costs.

Transportation & Warehousing (-11,000)

E-commerce normalization and inventory recalibration weigh on hiring.

Government (-42,000)

A surprising contraction after steady public hiring in prior months.

The distribution suggests that structural sectors are offsetting cyclical weakness — a hallmark of late-cycle Growth stabilization.

Wage Growth: The Inflation Transmission Channel

Average Hourly Earnings rose 0.4% month-over-month.

At 3.7% year-over-year, wage Growth remains above the level consistent with the Fed’s 2% inflation target when adjusted for productivity.

Persistent wage momentum implies:

- Services inflation may remain sticky

- Consumer spending power remains intact

- Core inflation risks are not fully extinguished

The bond market focused heavily on this element.

Labor Force Participation: The Underappreciated Story

The participation rate climbed to 62.5%.

After years of concerns about labor shortages, rising participation signals:

- Improved labor supply

- Immigration inflows

- Re-entry of sidelined workers

- Structural adjustment in demographics

If this trend continues, it could offset inflationary pressure even amid solid hiring.

Federal Reserve Implications

Prior to the employment release, markets were pricing a high probability of a June rate cut.

Afterward:

- June cut odds dropped sharply

- Treasury yields climbed

- Rate expectations shifted deeper into 2025

However, the revision kept policymakers cautious.

Chair Jerome Powell has emphasized “data dependency.” This employment mix reinforces that stance.

The Fed now faces:

- Strong current hiring

- Revised weaker prior baseline

- Sticky wages

- Moderating but resilient inflation

This complicates forward guidance.

Bond Market Repricing

10-year Treasury yields briefly tested key technical levels.

Higher yields suggest:

- Delayed easing cycle

- Higher neutral rate assumptions

- Stronger Growth expectations

However, yield pullbacks mirrored the fading US Dollar Market Reaction.

Markets remain cautious rather than fully hawkish.

Comparing to ADP and ISM Data

Private payroll processor ADP reported softer hiring prior to the official figures.

The ISM Services employment index showed contraction.

When official data diverges from private indicators, markets become skeptical.

Future revisions may reconcile these discrepancies.

What Happens Next?

All eyes now shift to:

- CPI inflation data

- PCE readings

- Next NFP release

- Wage trend persistence

- Continued Unemployment Rate stability

If inflation remains firm alongside strong US Jobs Report readings, rate cuts may be postponed deep into 2025.

If inflation cools, January may be viewed as statistical noise.

Conclusion: A Data Fog Moment

The January US Jobs Report delivered:

- Strong NFP Growth

- Falling Unemployment Rate

- Sticky wages

- Rising participation

- Historic downward revision

- Volatile US Dollar Market Reaction

It is both a bullish and cautionary report simultaneously.

For now, markets are treating the data as inconclusive.

The Fed remains on pause. The dollar remains reactive. The bond market remains sensitive.

One thing is clear: the path toward rate cuts is no longer certain.

The US Jobs Report has reset expectations — but not clarified direction.