Earnings season has reached a pivotal moment for U.S. equities, delivering a powerful mix of headline strength and underlying economic divergence. As the most dramatic phase of the Q4 2025 reporting cycle draws to a close, aggregate numbers suggest corporate America remains in excellent health. Yet beneath those impressive totals, a more fragmented and uneven reality is taking shape—one that reflects a deeply K-shaped market economy.

According to aggregated earnings data, the S&P 500 is on track to record its fifth consecutive quarter of double-digit earnings growth, with blended growth approaching 13%. That figure stands well above expectations set at the start of the quarter and reinforces the perception of resilience across U.S. corporations. However, this earnings season is less about the averages and more about the extremes.

Mega-cap, globally exposed companies continue to dominate results, buoyed by artificial intelligence investment, pricing power, and currency tailwinds. Meanwhile, domestically focused, cyclical, and consumer-sensitive businesses are showing clear signs of stress. This widening performance gap has profound implications for stock market earnings analysis, investor positioning, and equity market valuation risks heading into 2026.

The Big Picture: Why This Earnings Season Matters

At first glance, the numbers from this earnings season are difficult to argue with. Roughly three-quarters of reporting companies have exceeded earnings expectations, while revenue growth is tracking near its strongest pace since 2022. Corporate margins, though under pressure in certain areas, have remained surprisingly resilient.

However, the market’s current valuation assumes that this strength is both sustainable and broad-based. With the forward price-to-earnings ratio hovering well above long-term averages, investors are effectively betting that earnings momentum will spread beyond a narrow group of winners. This earnings season is testing that assumption in real time.

International vs. Domestic: A Defining Split

One of the most striking themes emerging from this earnings season is the geographic divide in corporate performance. Companies generating a majority of their revenue internationally are reporting significantly faster earnings growth than those focused primarily on the U.S. market.

Several factors are driving this divergence:

- A weaker U.S. dollar has amplified overseas earnings

- Stronger demand in select international markets

- Heavy concentration in technology and industrial leaders

Yet this strength is not evenly distributed. A small number of global giants account for an outsized share of international earnings growth, underscoring the growing concentration risk within the index. Excluding a handful of mega-cap contributors, earnings growth among internationally exposed firms drops meaningfully.

This dynamic reinforces the idea that this earnings season is less about a rising tide and more about selective leadership.

Sector Performance Highlights a K-Shaped Market Economy

The sector-level data from this earnings season paints a textbook picture of a K-shaped market economy.

Clear Winners

- Technology companies tied to AI infrastructure and cloud demand

- Select industrial names benefiting from long-cycle investment trends

- Communication services leaders with dominant platforms

These sectors are driving the bulk of index-level growth and investor enthusiasm.

Clear Losers

- Consumer discretionary segments tied to big-ticket purchases

- Healthcare companies facing margin compression and policy uncertainty

- Energy firms impacted by lower year-over-year commodity prices

Within consumer discretionary alone, the divergence is stark. Premium leisure experiences and high-end brands continue to thrive, while autos and household durables face sharp earnings declines. This uneven consumer behavior is one of the clearest signals from this earnings season that economic pressure is rising beneath the surface.

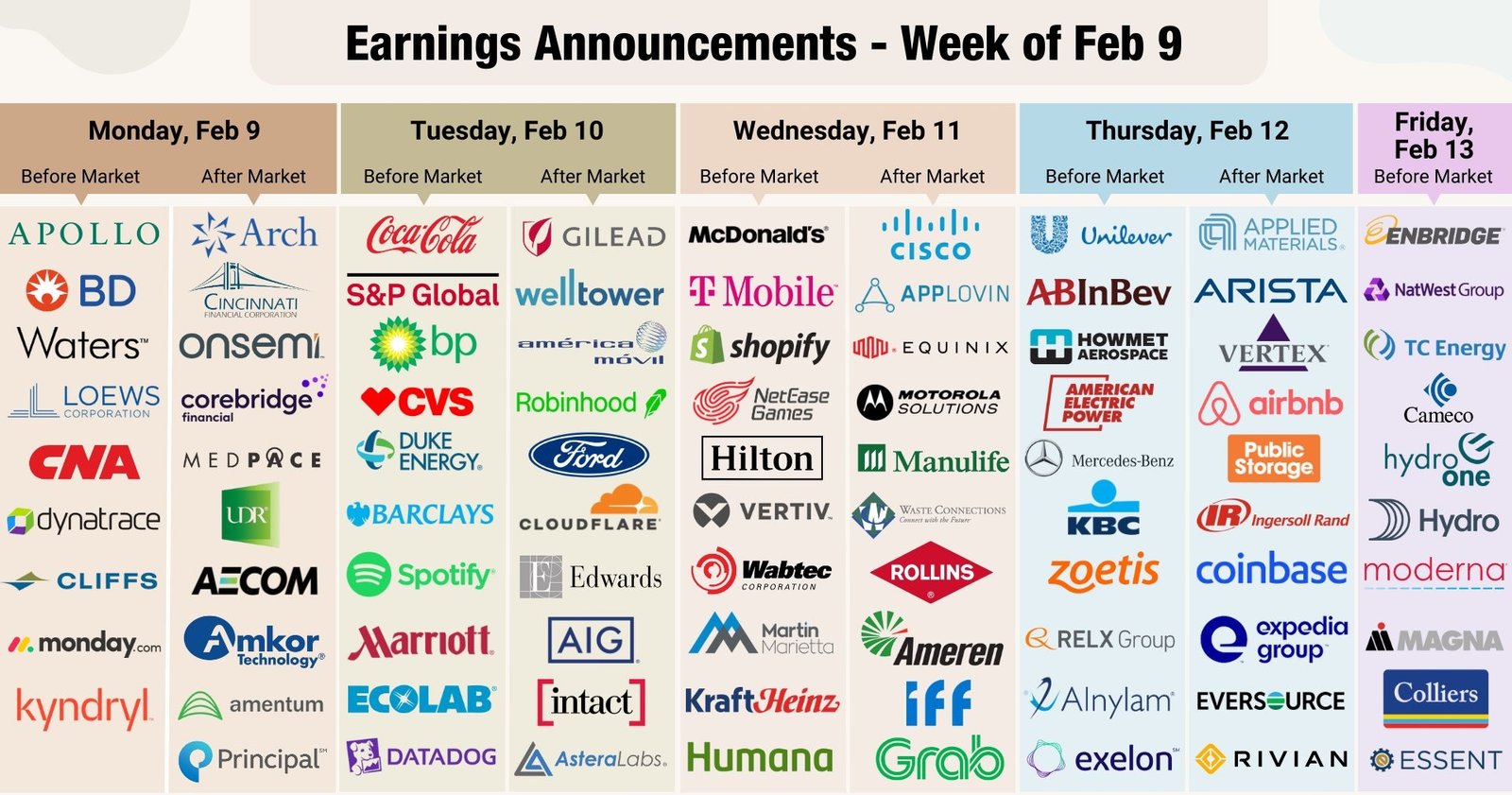

Coca-Cola: A Bellwether for the Real Economy

Few companies offer a clearer window into global consumer health than Coca-Cola, making its earnings particularly significant during this earnings season. As a company with unmatched global reach and pricing power, Coca-Cola sits at the intersection of inflation, consumer confidence, and disposable income trends.

Investors are closely monitoring several key metrics:

- Volume growth versus pricing increases

- Evidence of consumer trade-down behavior

- Regional demand trends across developed and emerging markets

Any sign that volume growth is weakening, even as prices remain elevated, would signal increasing strain on consumers worldwide. In a market priced for resilience, such signals carry outsized importance.

Market Reactions: Selective Optimism, Limited Punishment

One notable feature of this earnings season has been how markets are reacting to results. Companies that beat expectations are receiving modest rewards, while those that miss are not being punished as severely as historical norms would suggest.

This pattern reflects a market that is:

- Willing to forgive short-term weakness in favored sectors

- Less tolerant of disappointment in high-valuation names

- Increasingly focused on forward guidance rather than backward-looking results

This behavior also suggests growing complacency—a factor that adds to equity market valuation risks should macro conditions deteriorate.

Valuations: The Quiet Risk Building Beneath the Surface

Despite strong earnings growth, valuations remain elevated. The forward multiple on the S&P 500 sits well above its long-term average, reflecting optimism that earnings growth will continue uninterrupted.

Interestingly, valuation compression has come not from falling prices but from rising earnings estimates. While this dynamic appears healthy on the surface, it leaves little margin for error. Any broad-based guidance cuts or demand slowdowns could force a rapid reassessment.

This earnings season has not yet delivered such a shock—but it has made clear how concentrated the growth engine truly is.

Guidance Trends: Cautious Optimism or Delayed Reality?

Corporate guidance issued during this earnings season has been less negative than historical averages. Fewer companies than usual are guiding earnings lower for upcoming quarters, which analysts have interpreted as a sign of confidence.

However, guidance often lags reality. Management teams are balancing transparency with market expectations, and many are reluctant to signal weakness prematurely. As a result, the true test will come in subsequent quarters if demand softens or cost pressures persist.

The Real Economy Takes Center Stage

As mega-cap technology companies complete their reporting cycles, attention is shifting toward firms more directly tied to the real economy. This includes:

- Industrial suppliers

- Automotive manufacturers

- Consumer staples and services

- Enterprise technology providers

These companies offer clearer insight into everyday economic activity and spending behavior. Their results during this earnings season are crucial for validating—or challenging—the market’s optimistic assumptions.

AI vs. Everything Else

A defining tension of this earnings season is the contrast between AI-driven investment and broader corporate spending. While AI-related capital expenditure remains robust, there are growing questions about whether it is crowding out other forms of investment.

Enterprise networking, traditional IT infrastructure, and industrial automation are emerging as potential pressure points. Weakness in these areas would suggest that AI spending is not lifting the entire ecosystem as investors hope.

The Consumer Divide Becomes Impossible to Ignore

Consumer behavior remains one of the most important themes of this earnings season. Results from mass-market brands point to growing price sensitivity, while premium brands continue to report strength.

This divergence reflects:

- Persistent inflation pressure on lower- and middle-income households

- Strong balance sheets among higher-income consumers

- A gradual shift in spending priorities

If this pattern intensifies, it could weigh on aggregate growth and challenge the sustainability of current valuations.

Investment Implications: Navigating a Fragmented Market

This earnings season underscores several key realities for investors:

- Growth is real—but uneven

- Leadership is narrow and concentrated

- Valuations assume near-perfect execution

- The real economy is under increasing scrutiny

Opportunities remain, particularly in companies with durable pricing power, global exposure, and strong balance sheets. However, risk management is becoming more important as dispersion increases.

Conclusion: Earnings Season as a Stress Test

This earnings season is not simply another reporting cycle—it is a comprehensive stress test for the market’s dominant narrative. While headline growth remains impressive, the underlying data tells a more complicated story of divergence, concentration, and rising equity market valuation risks.

The K-shaped market economy is no longer a theoretical concept; it is visible across sectors, geographies, and consumer segments. Whether this divide narrows or deepens in the months ahead will determine whether current valuations are justified—or vulnerable.

For now, investors should resist complacency, focus on fundamentals, and recognize that beneath the surface of strong earnings lies a market demanding far greater selectivity and discipline.